The final trading day of 2025 delivered a golden surprise for Goldgroup Mining Inc. (TSXV: GGA) investors. While many were closing their books, GGA shares surged ~4% on December 31, 2025, closing at CAD 1.56—a staggering 817% YTD return from its January lows.

This wasn't just a "Santa Claus rally." It was the culmination of a massive structural pivot that has transformed Goldgroup from a struggling junior into a concentrated production powerhouse.

The Dec 31 Catalyst: Trimming the Fat

Source: Kalkine Group

The primary driver for the year-end bump was the official announcement on December 31 that Goldgroup entered into an agreement to sell its subsidiary Minera Apolo, effectively disposing of the Pinos Project.

Why the market loved it:

- Balance Sheet Optimization: The sale simplifies the corporate structure and provides a non-dilutive capital infusion.

- Strategic Focus: Investors are cheering the shift away from "project juggling" to focus entirely on their high-margin Sonora assets.

- Safe-Haven Tailwinds: With spot gold hitting $4,500/oz in late 2025 due to geopolitical tensions, any company streamlining for pure-play production saw aggressive year-end bidding.

Latest Business Model & Operational Updates

Goldgroup’s 2025 "Rebirth Model" focuses on low-capex, high-recovery heap leaching.

- The San Francisco Mine Acquisition

On December 24, 2025, Goldgroup finalized 100% ownership of the San Francisco Gold Mine through the bankruptcy restructuring of Molimentales. This adds a formerly producing asset with massive infrastructure already in place.

- Cerro Prieto Optimization

The flagship Cerro Prieto project is undergoing a massive facelift:

- Target: 30,000 oz of gold annually.

- The Secret Sauce: A re-leaching program of existing pads is expected to add 9,000 oz/year for the next six years at near-zero extraction cost.

- Tech Integration: Adoption of AI-powered ore sorting and real-time monitoring to mitigate the 15% rise in energy costs seen across the sector this year.

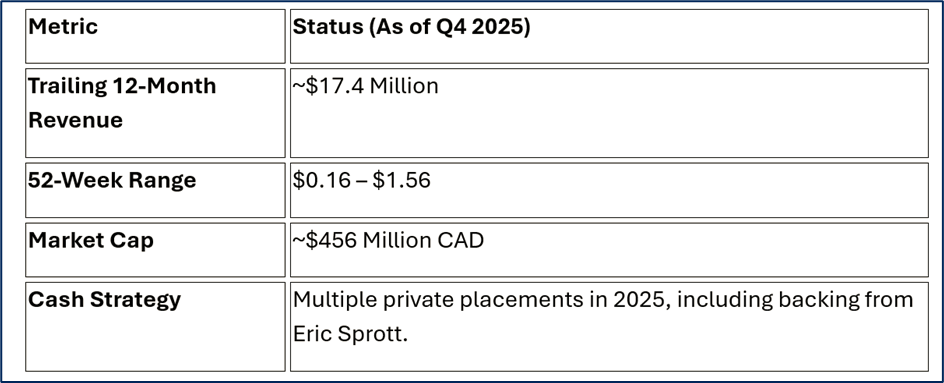

2025 Financial Snapshot

Source: Company Data

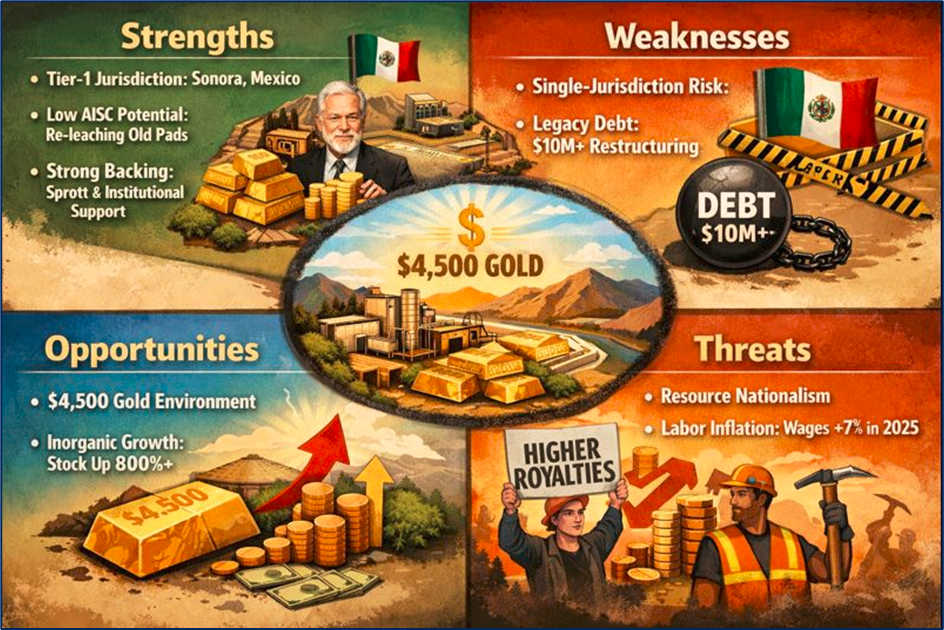

SWOT Analysis

Source: Kalkine Group

Strengths

- Tier-1 Jurisdiction: Sonora, Mexico remains a premier mining hub.

- Low AISC potential: Re-leaching old pads provides ultra-high-margin ounces.

- Strong Backing: Major institutional and billionaire (Sprott) interest.

Weaknesses

- Single-Jurisdiction Risk: Exposure to Mexican regulatory changes.

- Legacy Debt: Managing the US$10M+ restructuring debt from the Molimentales deal.

Opportunities

- $4,500 Gold Environment: Record metal prices provide a massive safety net for operational errors.

- Inorganic Growth: Ability to use its now-valuable stock (up 800%+) as currency for further acquisitions.

Threats

- Resource Nationalism: Increasing government pressure in Latin America for higher royalties.

- Labor Inflation: Mining wages rose ~7% in 2025, eating into margins.

Key Risks to Watch

- Approval Contingencies: The Pinos sale and San Francisco acquisition still face final TSXV approval.

- Geopolitical Volatility: While high gold prices help, trade disruptions can spike the cost of cyanide and machinery parts.

- Dilution: Frequent private placements to fund "aggressive drilling" could cap per-share gains.

The Verdict

Goldgroup Mining’s 4% jump on New Year's Eve marks the transition from a "story stock" to a "production stock." By shedding the Pinos Project and consolidating the San Francisco mine, management has signaled they are betting everything on their core Sonora footprint. In a world where gold is the ultimate insurance policy, GGA has positioned itself as a high-leverage play on the metal’s historic 2025 bull run.

Please wait processing your request...

Please wait processing your request...