Catalysts Behind the January 9th Surge

The approximately 8% spike in Cameco Corporation’s share price on January 9, 2026, is the culmination of a "perfect storm" in the nuclear energy sector. The primary driver is the accelerating "Nuclear Renaissance," where global governments are aggressively pivoting toward nuclear power to meet net-zero carbon targets and secure energy independence.

Source: Kalkine Group

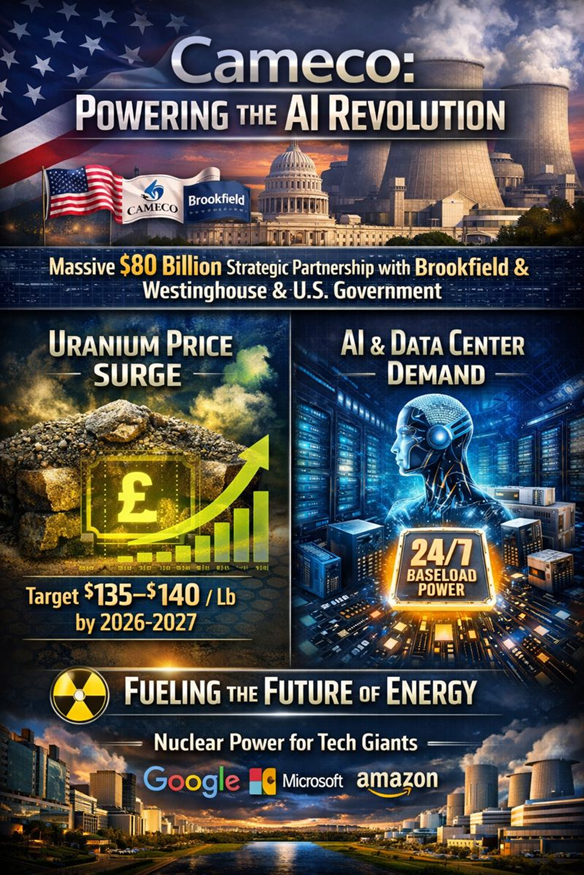

- The US Strategic Partnership Effect: Investor sentiment remains highly elevated following the massive strategic partnership between Cameco, Brookfield, and the U.S. government. This collaboration, centered on the deployment of Westinghouse nuclear reactor technology, signals a decades-long commitment to rebuilding Western nuclear infrastructure.

- Spot Price Momentum: Uranium spot prices have broken key psychological barriers, with forecasts now eyeing $135–$140 per pound for the 2026 period. As a primary producer, Cameco’s margins expand exponentially with every dollar increase in the underlying commodity.

- AI and Data Centre Demand: The relentless expansion of AI and massive data centers has created a desperate need for 24/7 "baseload" power. Tech giants are increasingly signing direct power purchase agreements with nuclear providers, positioning Cameco as the "fuel provider to the AI revolution."

Technical Analysis: Breaking the C$145 Barrier

Source: Trading View

From a technical perspective, Cameco (CCO on TSX) is displaying a textbook bullish breakout. The stock has been trading within a well-defined rising trend channel for much of late 2025 and has accelerated into 2026.

- Resistance and Support: The stock recently tested and successfully breached the C$145 resistance level, hitting an intraday high of C$147.24. This upward breakthrough typically signals a "buy" for momentum traders, with the next major psychological resistance sitting at the C$155 mark (near its 52-week high of C$153.59).

- Moving Averages: CCO is currently trading well above its 50-day (C$111.95) and 200-day Simple Moving Averages. The widening gap between the current price and these averages indicates a strong, sustained uptrend.

- Technical Indicators: The RSI (14) is currently reading approximately 78, which suggests the stock is in overbought territory. While this confirms strong buying pressure, it also flags the potential for a short-term consolidation or "cooling off" period. The MACD remains in a clear "Buy" position, reflecting positive trend momentum.

Analyst Consensus: Upgrades and Target Prices

Wall Street and Bay Street remain overwhelmingly bullish on Cameco’s trajectory for 2026. Recent updates suggest a significant shift in valuation models as the market transitions from viewing Cameco as a "miner" to a "vertically integrated energy giant."

- Scotiabank Target Boost: On January 8, 2026, Scotiabank raised its price target for CCO from C$150.00 to C$155.00, maintaining an "Outperform" rating.

- Broad Consensus: The consensus among 15 analysts is a "Buy," with 14 analysts issuing Buy or Strong Buy ratings and only one holding a "Hold" position. High-end price targets have reached as high as C$175.00.

- Valuation Concerns: Some analysts at Simply Wall St and Zacks have noted that the current P/E ratio (exceeding 118x) is significantly higher than the energy sector average, suggesting that much of the future growth may already be priced in.

Evolving Business Model: Beyond Just Mining

Cameco’s business model has undergone a "transformational shift." While they remain a titan in uranium extraction, they are now a fully integrated player in the nuclear value chain.

- The Westinghouse Powerhouse: Through its 49% stake in Westinghouse, Cameco now earns significant revenue from reactor design, nuclear services, and fuel fabrication. This provides a steady, "utility-like" cash flow that balances the cyclical nature of uranium mining.

- Fuel Services Dominance: Cameco is one of the few Western companies capable of converting and enriching uranium, a critical bottleneck in the global supply chain as utilities move away from Russian-sourced fuel.

- Long-Term Contracting: Unlike speculative juniors, Cameco operates on a disciplined contracting strategy. They have layered in long-term contracts that protect them from downward price swings while retaining exposure to rising market prices through "market-related" pricing tiers.

Financial and Operational Updates

The latest updates highlight a company operating at peak efficiency despite the inherent challenges of high-grade uranium mining.

- Production Outlook: For 2026, Cameco is targeting an attributable production share of approximately 24 million pounds of uranium, up from the 2025 estimate of 22 million pounds.

- Financial Health: As of the latest reports, Cameco maintains a strong liquidity position with C$779 million in cash and a C$1 billion undrawn credit facility. Their debt-to-equity ratio remains healthy at approximately 14.7%.

- Upcoming Earnings: The market is eagerly awaiting the Q4 2025 results, scheduled for release on February 13, 2026, which will provide a clearer picture of year-end performance and 2026 guidance.

Critical Risks to Consider

Despite the bullish sentiment, investors must weigh several high-impact risks:

- Operational Disruptions: Mining in the Athabasca Basin is technically challenging. Issues such as production setbacks at McArthur River/Key Lake or development delays can impact quarterly results.

- Geopolitical Volatility: While energy security is a tailwind, changes in international trade policies or uranium export regulations from Kazakhstan (Kazatomprom) can disrupt global price dynamics.

- The "Safety" Sentiment: Any significant nuclear incident anywhere in the world would likely trigger an immediate, sharp de-rating of the entire sector.

- Stretched Valuation: With a Forward P/E ratio far above industry peers, the stock is sensitive to any news that suggests a slowing of the "nuclear momentum."

Conclusion

Cameco Corporation has successfully positioned itself at the epicenter of the global energy transition. Today’s surge reflects a growing market consensus that the "uranium supercycle" is supported by long-term structural demand. By combining world-class tier-one assets like Cigar Lake with the technological expertise of Westinghouse, Cameco has evolved into a strategic energy asset that transcends simple commodity mining.

Please wait processing your request...

Please wait processing your request...