The first trading day of 2026 has sent shockwaves through the mining sector as Barrick Gold (TSX: ABX) jumped roughly 4.3% on January 5, 2026. While the broader market navigates a landscape of "Green Transition" volatility and shifting trade policies, Barrick has emerged as a clear beneficiary of a "Perfect Storm" in the commodities market.

This analysis breaks down the catalysts driving the rally, the company’s evolved business model, and the critical SWOT factors every retail and institutional observer is watching.

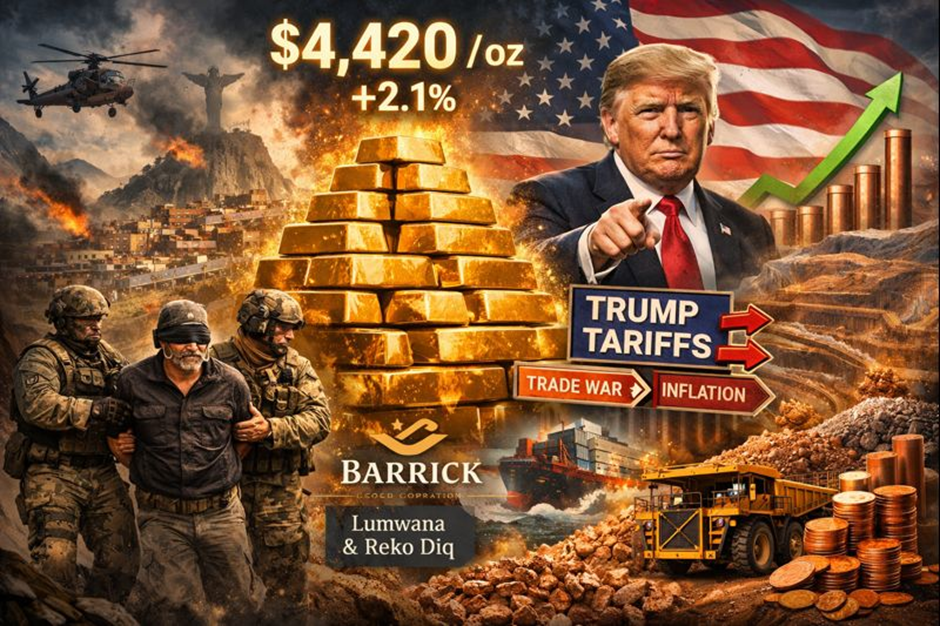

The Big Spark: Why the 4.3% Jump Today?

Source: Kalkine Group

The rally on January 5 was primarily fueled by a 2.1% surge in spot gold prices, which climbed toward $4,420/oz. This move was triggered by:

- Safe-Haven Demand: Renewed geopolitical tensions in South America (specifically the U.S. capture of a regional leader) sparked an immediate flight to safety.

- The "Trump Tariff" Effect: Ongoing global trade friction has solidified gold as the premier hedge against currency devaluation and inflation.

- Copper Correlation: With copper prices rising nearly 3%, Barrick’s significant copper portfolio (Lumwana and Reko Diq) provided an additional "growth metal" kicker that pure-play gold miners lacked.

Business Model 2026: More Than Just Gold

Barrick has pivoted from a traditional gold miner to a diversified Tier One copper-gold producer. By 2026, the company’s strategy is built on three pillars:

- Tier One Asset Focus: Barrick only targets "Tier One" mines—assets capable of producing over 500,000 ounces of gold annually with a life of at least 10 years and costs in the lower half of the industry curve.

- The Copper Bridge: Recognizing the global shift toward electrification, Barrick has aggressively expanded its copper footprint. It now views copper as a strategic partner to gold, diversifying revenue and tapping into the EV and AI infrastructure boom.

- Owner-Operator Excellence: Unlike peers who rely heavily on contractors, Barrick’s 2026 model emphasizes "hands-on" management, utilizing an agile, decentralized regional structure.

Financial & Operational Update: The Pulse of ABX

Latest Financials (Q4 2025/Q1 2026 Snapshot)

- Free Cash Flow (FCF): Projected to reach a record yield of approximately 12% for 2026, outperforming most large-cap peers.

- Shareholder Returns: In late 2025, Barrick hiked its base dividend by 25% and maintained a robust $1 billion share buyback program.

- Debt Profile: The company remains in a net-cash or low-debt position, providing the "war chest" needed for massive capital projects.

Operational Highlights

- Reko Diq (Pakistan): The massive copper-gold project is on track, with recent JV approvals securing its path to production by 2028.

- Fourmile (Nevada): Exploration results in late 2025 confirmed this as one of the highest-grade gold discoveries of the century.

- The "Mali Resolution": In November 2025, Barrick resolved its disputes with the Mali government, stabilizing the Loulo-Gounkoto complex—a major relief for the stock’s risk premium.

SWOT Analysis: The 2026 Reality Check

Source: Kalkine Group

Strengths

- Unrivaled Reserve Replacement: Consistently replaces over 100% of mined reserves through organic exploration rather than expensive M&A.

- Geographic Diversification: Operating across five continents hedges against localized political disruptions.

- High-Grade Pipeline: Assets like Fourmile offer grades significantly higher than the industry average.

Weaknesses

- High Capex Demands: Massive projects like Lumwana and Reko Diq require billions in upfront spending, which may limit FCF growth in the immediate short term.

- Production Plateaus: Annual gold production has been hovering in the 3.1M–3.5M oz range, leading some to call for more aggressive growth.

Opportunities

- North American Asset IPO: Management has discussed spinning off North American assets to unlock value and achieve a "re-rating" to higher multiples.

- Critical Minerals Demand: Rising copper prices due to the AI data center boom provide a secular tailwind.

Threats

- Resource Nationalism: Increasing taxes and royalty demands in emerging markets (Africa/Central Asia) remain a persistent threat to margins.

- Cost Inflation: Despite falling energy costs, specialized labor and mining equipment inflation remains sticky at 3–5%.

Key Risks to Watch

While the stock is currently riding high, several "tripwires" remain:

- Geopolitical Instability: Operations in Mali and Pakistan carry inherent jurisdictional risks.

- Execution Risk: Any delays in the multi-billion dollar "Super Pit" expansion at Lumwana could sour investor sentiment.

- Gold Price Correction: If central banks slow their bullion purchases, a sharp pullback in gold would directly hit ABX’s bottom line.

Conclusion

Barrick Gold’s 4.3% jump on January 5 is more than a daily blip; it is a reflection of a company that has successfully positioned itself at the intersection of monetary safety (gold) and industrial growth (copper). With a 2026 outlook defined by record cash flows and a resolution of key political hurdles, Barrick is operating at a level of financial health rarely seen in its history. However, the path forward requires flawless execution of its massive capital projects and navigating a world where "mining" is as much about diplomacy as it is about geology.

Please wait processing your request...

Please wait processing your request...