On December 24, 2025, while most of the market was winding down for the holidays, Mullen Group Ltd. (TSX: MTL) managed to squeeze out a 0.8% gain, closing at approximately CAD 16.21. While 0.8% might seem modest, it represents a continuation of a powerful year-end rally that has seen the stock surge over 13% in the last month alone, consistently hitting new 52-week highs.

Why the Green Close? Key Drivers on Dec 24

The Christmas Eve bump was less about a single "smoking gun" and more about investor positioning for 2026.

Source: Kalkine Group

- The Yield Hunt: Mullen recently affirmed its monthly dividend of $0.07 per share ($0.84 annualized). With the ex-dividend date looming on December 31, retail and institutional "dividend captures" likely provided buying support.

- Balance Sheet Cleanup: Earlier in December, Mullen completed the redemption of its 5.75% convertible debentures. This move reduced potential share dilution and signaled to the market that the company is entering 2026 with a leaner, more efficient capital structure.

- Analyst Upgrades: Following the Q3 results, heavyweight firms like BMO Capital Markets and Desjardins hiked their price targets to the $18.00–$19.00 range, suggesting that despite being at 52-week highs, the stock still has "legs."

The Latest Business Model: "The Decentralized Aggregator"

Mullen’s 2025 evolution has shifted from simple trucking to a sophisticated non-asset-based logistics powerhouse.

- Strategic Segments

The business now operates through four distinct pillars:

- Less-Than-Truckload (LTL): The steady "bread and butter" income.

- Logistics & Warehousing (L&W): The current growth engine, up over 23% in recent quarters.

- Specialized & Industrial Services: Serving the Western Canadian energy and mining sectors.

- U.S. & International Logistics: The new frontier, bolstered by the 2025 acquisition of Cole Group.

- The Acquisition Machine

Mullen operates a "decentralized" model. They acquire well-run regional players, keep the local management in place, and provide them with corporate "muscle" (capital and technology). In 2025, they allocated $150 million specifically for these "tuck-in" acquisitions.

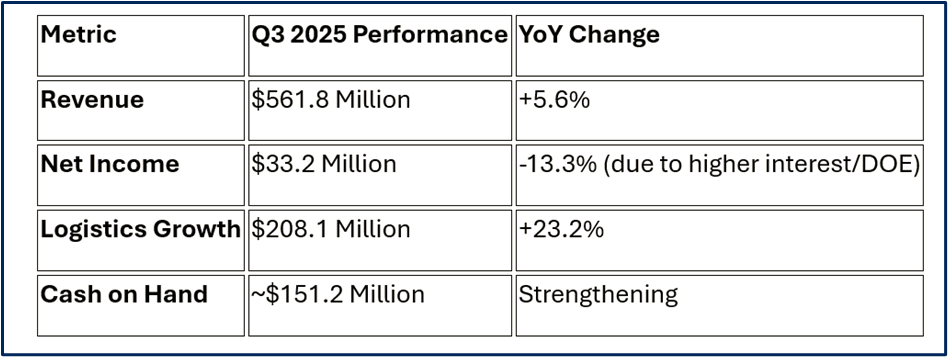

Latest Financial & Operational Updates (Q3/Q4 2025)

Mullen’s performance in the latter half of 2025 has been a story of resilience in a soft economy.

Source: Company Data

Operational Milestone: The acquisition of Cole Group (finalized mid-2025) added approximately $300 million in annualized revenue potential, specifically expanding their footprint in customs brokerage and freight forwarding—high-margin services that don't require owning thousands of expensive trucks.

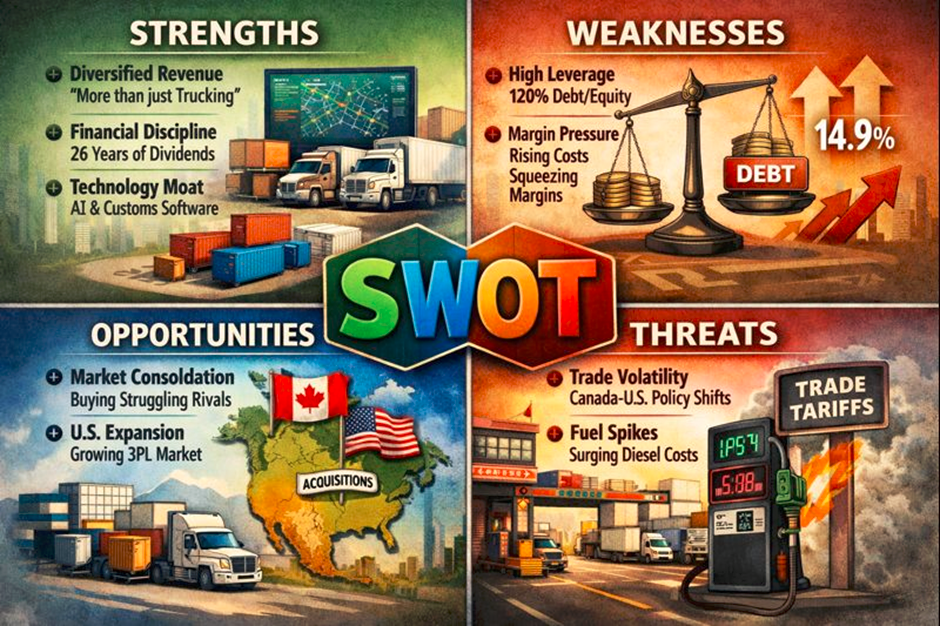

SWOT Analysis

Source: Kalkine Group

Strengths

- Diversified Revenue: They aren't just a "trucking company"; they are a logistics platform.

- Financial Discipline: High free cash flow yield and a 26-year history of dividend payments.

- Technology Moat: Heavy investment in AI-driven routing and proprietary customs software.

Weaknesses

- Leverage: A debt-to-equity ratio of ~120% makes them sensitive to prolonged high interest rates.

- Margin Pressure: Rising direct operating expenses (DOE) have slightly compressed operating margins to around 14.9%.

Opportunities

- Market Consolidation: In a "soft" Canadian economy, smaller competitors are struggling, allowing Mullen to acquire them at attractive valuations.

- U.S. Expansion: The U.S. 3PL market remains a massive growth target for their non-asset-based business.

Threats

- Trade Volatility: Potential shifts in Canada-U.S. trade policy and tariffs could impact cross-border volumes.

- Fuel Volatility: While surcharges help, sudden spikes in diesel prices can lag in recovery.

Critical Risks to Watch

Investors shouldn't ignore the "Specialized & Industrial" segment, which saw a 20% revenue drop recently due to a lack of large-scale capital projects in Western Canada. If the energy sector remains stagnant, this segment will continue to drag on the high-flying Logistics division. Furthermore, the high Short Interest (reaching ~8% in late 2025) suggests that some big players are betting on a correction after this massive run.

Conclusion

Mullen Group’s 0.8% rise on December 24 is a microcosm of its 2025 strategy: steady, incremental, and focused on shareholder returns. By pivoting toward "asset-light" logistics and brokerage, Murray Mullen has shielded the company from the worst of the trucking downturn. As we head into 2026, the stock is a "show-me" story: can they integrate their 2025 acquisitions fast enough to offset the slowing industrial sector?

Please wait processing your request...

Please wait processing your request...