_12_17_2025_16_42_13_496875.jpg)

Investors are buzzing after Accord Financial Corp. (TSX: ACD) saw a sudden ~18% surge on December 17, 2025. While the stock has faced a gruelling year of debt restructuring and bottom-line losses, a series of high-stakes "survival" updates in mid-December has finally given the market something to chew on.

Is this the beginning of a massive recovery, or a final "relief rally" before more turbulence? Let’s dive into the analytical breakdown of what is driving this micro-cap finance player right now.

The 18% Catalyst: Why the Spike Today?

The recent volatility and the 18% jump are driven by a shift from "uncertainty" to "action." After months of silence, Accord has released a comprehensive refinancing roadmap that signals a clear path away from potential default.

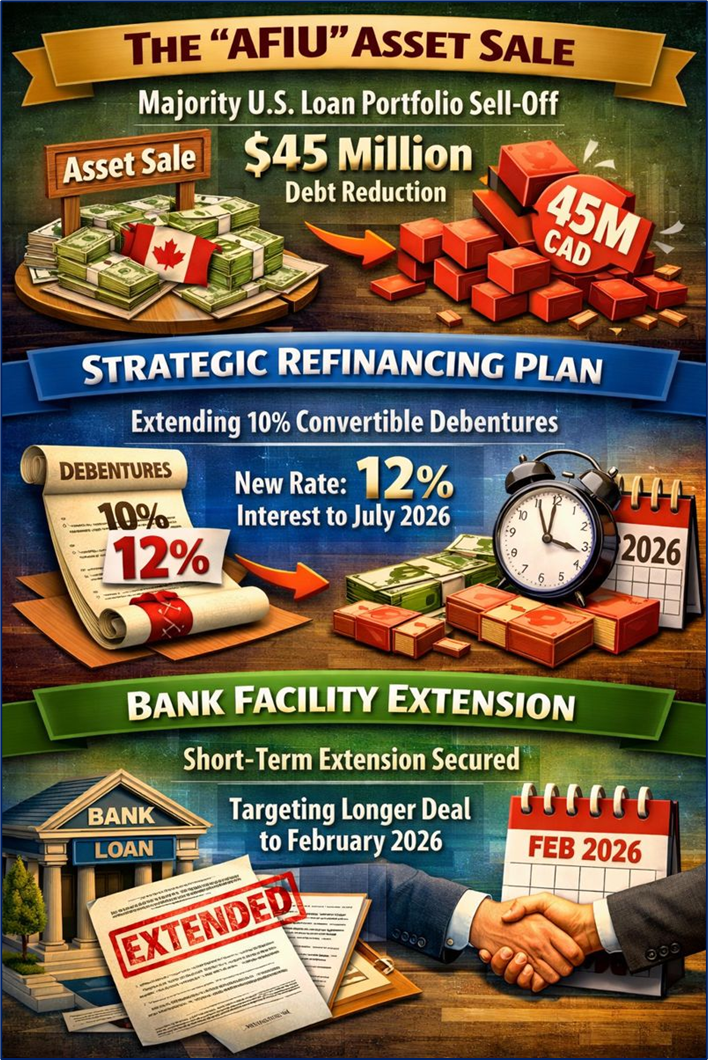

- The "AFIU" Asset Sale

On December 11, Accord signed a non-binding Letter of Intent (LOI) to sell a majority of its U.S. loan portfolio (Accord Financial, Inc. or AFIU). This deal is expected to slash debt by approximately $45 million CAD. For a company with a market cap under $15 million, a $45 million debt reduction is a massive de-leveraging event.

The market is reacting to a massive restructuring of its debt. Accord is moving to extend the maturity of its 10% convertible debentures to July 2026 and raise the interest rate to 12% to appease lenders. This buys the company six critical months to stabilize.

On December 15, the company secured a short-term extension of its main credit facility. While only for a few days (initially to December 23), it signals that the lending syndicate is staying at the table to finalize a longer extension into February 2026, rather than forcing a liquidation.

Source: Kalkine Group

Business Model 2.0: The "Leaner Canada" Pivot

Accord has historically operated as a North American "lender of choice" for small and medium-sized enterprises (SMEs). However, the business model is currently undergoing a radical transformation:

- The Core: Asset-Based Lending (ABL), factoring, and equipment financing.

- The Shift: Moving away from a broad North American footprint to a Canada-first strategy. By divesting US assets, they are trading scale for stability.

- Revenue Drivers: Profit is generated via interest income and factoring commissions. However, the current focus isn't growth—it's liquidity. The company is essentially liquidating non-core assets to pay down a massive debt mountain that has "hampered" profitability all year.

Source: Kalkine Group

Latest Business Updates (Q3 2025 Recap)

The numbers behind the stock tell a story of a company under intense pressure, now trying to surface for air:

- Revenue: Declined to $15.8 million in Q3 2025 (down from $21.2 million YoY).

- Net Loss: Reported a loss of $2.4 million ($0.28 per share).

- Book Value: Currently sits at $8.92, significantly higher than the trading price (approx. $1.70–$2.10 range), suggesting a deep "value" play if the company avoids insolvency.

- Efficiency: Management has successfully cut general and administrative (G&A) expenses to $7.0 million to offset falling revenues, despite $1.1 million in professional fees spent solely on debt management.

The High-Stakes Risks: Why Caution is Key

While an 18% jump looks exciting, the technical and fundamental risks remain extreme:

- Refinancing Cliff: If debenture holders do not approve the amendments on January 27, 2026, the company may face a default scenario.

- Interest Deferral: Accord has officially deferred the December 31, 2025, interest payment. While planned as part of the restructuring, "deferred interest" is a classic distress signal.

- The "Non-Binding" Trap: The sale of the AFIU portfolio is currently under a non-binding LOI. If the buyer walks away, the $45 million debt-reduction plan vanishes.

- Low Liquidity: ACD is a micro-cap stock with thin volume. Small buy orders can cause massive percentage swings, making it easy to enter but difficult to exit without crashing the price.

Conclusion: Turnaround or Trap?

Accord Financial is currently a "Special Situations" play. The 18% spike reflects investor optimism that the sale of the U.S. portfolio and the debt extension will prevent a total collapse. With a book value of $8.92 against a stock price near $2.00, the math suggests a massive "margin of safety"—but only if the company can successfully navigate its January debt meeting.

The stock is no longer a traditional "growth" story; it is a survival story. For retail investors, the next 45 days will determine if ACD returns to its historical valuation or becomes a cautionary tale of over-leverage.

Source: Trading View, 17 December 2025, 11:05 AM, ON, Canada

Please wait processing your request...

Please wait processing your request...