WTI is surging and Baytex Energy is printing cash. Explore BTE’s 2026 outlook, price targets, dividends, buybacks & oil risks.

Latest Key Takeaways (January 2026)

- Production Surge: Baytex Energy is targeting 3% to 5% annual production growth, aiming for 75,000 boe/d by 2028, with a 2026 capital budget of up to $625 million (Baytex Newsfile, Dec 2025).

- Financial Discipline: The company recently achieved a sustaining breakeven price of US$52/bbl WTI, a 13% improvement over last year, enhancing resilience against volatile oil prices.

- Shareholder Returns: Following the Eagle Ford asset optimization, Baytex is prioritizing buybacks (NCIB) and maintaining steady dividends to return excess free cash flow.

- TSX Momentum: The S&P/TSX Composite hit record highs of 33,350 in late January 2026, driven by a 10% monthly rally in WTI crude and geopolitical tensions in the Middle East.

- Analyst Consensus: Wall Street and Bay Street maintain a "Moderate Buy" rating with a consensus price target of C$4.79, suggesting steady value despite global supply headwinds.

Can Baytex Energy (BTE) Dominate the TSX Energy Sector in 2026?

As we navigate through January 2026, the global energy landscape is witnessing a massive shift. Investors searching for the best energy stocks to buy on the TSX are laser-focused on Baytex Energy Corp (TSX: BTE). With the TSX Composite Index reaching all-time highs and the Canadian Dollar (CAD) showing resilience against the USD, the macro environment for Canadian oil producers is electrifying. Geopolitical risks, particularly reports of potential strikes on Iran, have sent WTI crude prices on a 10% monthly tear, directly benefiting heavy-weight Canadian energy players.

In this Baytex Energy stock analysis, we break down why retail investors are flocking to this name. Unlike the speculative bubbles of the past, the 2026 energy trade is built on disciplined capital allocation, record-breaking free cash flow (FCF), and strategic asset consolidation. Baytex is no longer just a "leveraged play" on oil; it has evolved into a lean, mean, cash-generating machine with a diversified portfolio spanning the Pembina Duvernay and the heavy oil corridors of Peace River.

The Canadian economy in early 2026 is at a crossroads. While the Bank of Canada has held interest rates steady at 2.25%, the threat of U.S. tariffs looms over the manufacturing sector. However, energy remains the crown jewel. With Baytex Energy's latest 2026 budget forecasting significant production growth and a streamlined debt profile, is this the moment to go long on BTE stock? Our deep-dive analysis provides the unbiased analytical reasoning you need to stay ahead of the curve in this high-volatility market.

Is the Global Oil Market Bullish for Canadian Producers?

The global market dynamics of 2026 are defined by a tug-of-war between immediate supply shocks and a looming medium-term surplus.

- Geopolitical Premium: Fears of supply disruptions in the Middle East have injected a "war premium" into crude, pushing prices toward the mid-$70s despite bearish forecasts from agencies like the EIA.

- India-Canada Energy Trade: A new ministerial energy partnership signed in January 2026 at India Energy Week is opening massive doors for Canadian heavy crude, reducing dependency on U.S. refining capacity and potentially improving netback prices for companies like Baytex (Discovery Alert, Jan 2026).

- The "Trump Put": While the U.S. administration favors lower oil prices to curb inflation, experts believe intervention is unlikely unless WTI falls below US$50, providing a psychological floor for the industry.

How Does the Canadian Economy Impact Your BTE Portfolio?

The Canada economy in January 2026 is showing a "quality divide." High-income consumption is keeping the TSX afloat, while the S&P/TSX Composite has outperformed the S&P 500 in relative terms.

- Currency Advantage: The CAD analysis shows a 1.8% increase against the USD this month, which helps Canadian producers manage USD-denominated debt, though it can slightly compress CAD-realized oil prices.

- Interest Rate Stability: The Bank of Canada’s decision to hold at 2.25% suggests that the "easy money" era is over, forcing energy companies to rely on internal cash flow rather than cheap debt for expansion.

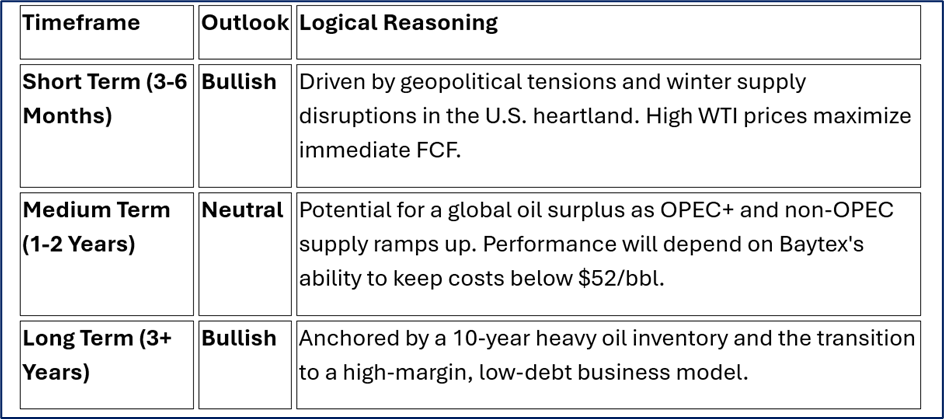

- Sector Outlook: In the short term, energy is a momentum play. In the medium term, analysts expect a market reset as non-OPEC+ supply (Brazil, Guyana) hits the market. Long term, disciplined players with low breakeven points will be the last ones standing.

What Are the Latest Financial and Operational Updates from Baytex?

Baytex Energy’s recent Form 6-K and SEDAR filings (Dec 2025/Jan 2026) reveal a company hitting its stride:

- 2026 Capital Budget: Set at $550 million to $625 million, focusing 55% on light oil and 45% on heavy oil (Baytex Newsfile).

- Production Targets: Aiming for 68,000 to 70,000 boe/d by the end of 2026, representing a solid 3-5% growth rate.

- Pembina Duvernay Success: This asset has become the company's growth engine, with recent wells delivering peak rates of 1,300 boe/d (Baytex Q3 2025 Transcript).

- Debt & Liquidity: Baytex reduced net debt to $2.2 billion and extended its $750 million credit facility to 2030, providing a massive runway for the next three years.

Investor Strategy: Should You Buy, Sell, or Hold BTE in 2026?

Source: Market Data

What Do the Top Analysts Predict for Baytex Share Price?

Latest ratings from January 2026 show a cautious but optimistic professional community:

- Scotiabank: Outperform rating; Price Target C$5.50 (Jan 20, 2026).

- TD Securities: Hold rating; Price Target C$5.00 (Jan 16, 2026).

- Canaccord Genuity: Hold rating; Price Target C$4.75 (Jan 27, 2026).

- BMO Capital Markets: Outperform rating; Price Target C$6.00 (Nov 13, 2025).

- Royal Bank of Canada: Sector Perform rating (Jan 13, 2026).

Latest FAQ for Investors

Q: Is Baytex Energy paying a dividend in 2026? A: Yes, Baytex currently pays a quarterly dividend of $0.0225 per share (approx. 2% yield) and is prioritizing further shareholder returns via share buybacks in 2026 (Baytex Newsfile).

Q: What is the biggest risk to Baytex Energy stock? A: The primary risk is a global oil surplus in late 2026, which could pull WTI prices toward the $50-$60 range, testing the company's new breakeven levels.

Q: Why did some analysts downgrade BTE in January 2026? A: Firms like Canaccord and TD Securities moved to "Hold" as the stock reached their price targets, citing a balanced risk-reward profile after the recent 25% year-over-year gain.

Investment Conclusion: Buy, Sell, or Hold?

Verdict: HOLD for Income, BUY for Momentum. If you are looking for short-term tactical gains, the current geopolitical environment and TSX record highs provide a strong tailwind for BTE stock. However, for long-term retail investors, the story is about discipline. Baytex has successfully navigated the "leverage trap" and is now a robust producer with an attractive US$52/bbl breakeven. While a massive breakout beyond C$6.00 requires a sustained $80+ WTI environment, the company’s focus on shareholder returns makes it a "High-Quality Hold" in any diversified Canadian portfolio.

Please wait processing your request...

Please wait processing your request...