Dorel Industries Inc. (TSX: DII.A) Performance Analysis

Dorel Industries Inc. (DII.A) electrified the Toronto Stock Exchange on January 27, 2026, with a commanding 14.5% surge in its Class A share price. This double-digit rally marks a significant inflection point for the global consumer products giant, which has spent much of the past year navigating a high-stakes balance sheet recapitalization and a fundamental resizing of its home furnishings division.

As the market digests the company's progress toward its goal of returning to full profitability by 2026, today’s price action suggests a growing investor appetite for Dorel’s leaner, juvenile-centric business model.

Latest Drivers of the Surge

Source: Kalkine Group

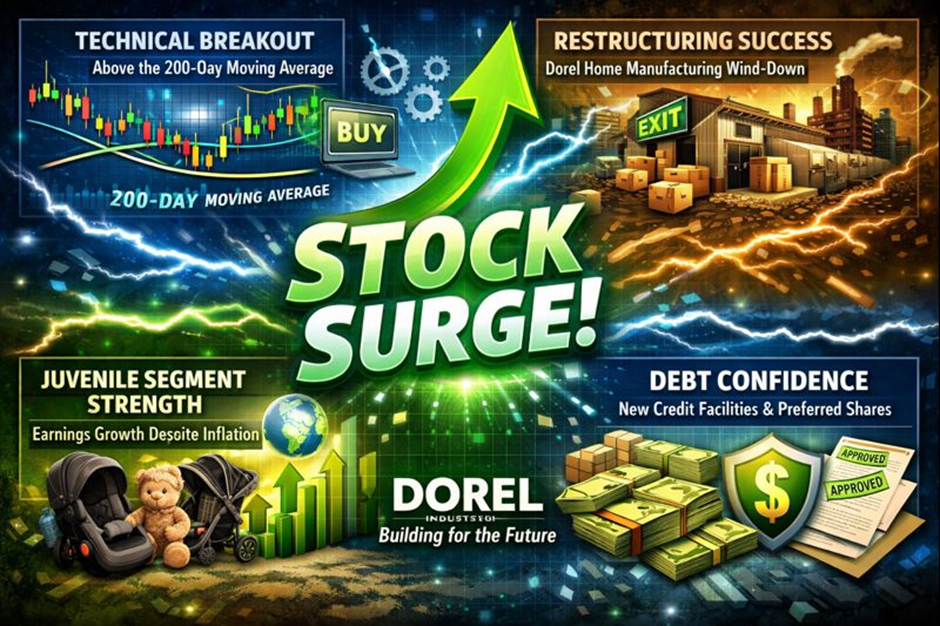

The primary catalyst for today's price action appears to be a combination of technical momentum and renewed confidence in the company’s internal restructuring.

- Technical Breakout: The stock recently crossed above its 200-day moving average, a key indicator that often triggers algorithmic and institutional buying (MarketBeat).

- Restructuring Execution: Investors are reacting to the successful wind-down of Dorel Home’s domestic manufacturing, a move designed to eliminate heavy losses and "substantially reduce" the segment's footprint (Dorel News).

- Juvenile Segment Strength: Continued resilient performance in the Dorel Juvenile segment, which has seen year-over-year earnings improvement despite global inflationary pressures.

- Debt Confidence: Clarity surrounding the company’s new credit facilities and preferred share issuance has mitigated immediate liquidity concerns that plagued the stock in 2025.

Current Business Model

Dorel operates as a global consumer products powerhouse divided into two primary reporting segments:

- Dorel Juvenile: This remains the company’s flagship and growth engine. It designs, manufactures, and distributes high-end children’s accessories, including strollers, car seats, and health aids under premier brands like Maxi-Cosi, Safety 1st, and Tiny Love (Dorel Company Profile).

- Dorel Home: Transitioning from a broad manufacturer to a leaner, more agile importer and distributor. This segment focuses on ready-to-assemble (RTA) furniture, metal folding furniture, and futons, primarily through e-commerce and major retail channels.

Financial, Operational, and Dividend Updates

Based on the most recent company filings and management statements:

- Financial Performance: In its latest quarterly filing (Q3 2025), Dorel reported revenues of approximately $415.73 million. While net margins remained negative due to restructuring costs, the company projected a return to segment-wide profitability in 2026 (Dorel Q3 Report / GlobeNewswire).

- Operational Shifts: Dorel has completed the closure of its North American manufacturing operations for the Home segment, shifting toward a sourcing-based model to lower fixed costs and improve cash flow (Dorel Business Update).

- Capital Structure: The company successfully closed new credit facilities and issued preferred shares in late 2025 to recapitalize the balance sheet and provide the runway needed for the Juvenile segment's expansion (Dorel Financing Announcement).

- Dividend Status: Dorel’s Board has historically paid dividends when declared; however, under the current recapitalization and debt covenants, there is no immediate regular dividend payout, with the company prioritizing debt reduction and operational stability (Dorel Dividends / Sedar).

SWOT Analysis

Source: Kalkine Group

- Strengths: Global brand recognition with Maxi-Cosi; strong e-commerce presence in the Home segment; diversified geographic revenue streams across the U.S. and Europe.

- Weaknesses: High debt-to-equity ratio; historical losses in domestic furniture manufacturing; vulnerability to consumer discretionary spending shifts.

- Opportunities: Expansion of the Juvenile segment in emerging markets; increased margins following the exit from North American manufacturing; potential for market share gains in the premium baby gear sector.

- Threats: Persistent inflationary pressures on raw materials; potential for new tariffs on imported goods; intense competition from low-cost furniture importers.

Outlook and Risks

The outlook for Dorel hinges on the 2026 "Return to Profitability" roadmap. Management has signaled that the fourth quarter of 2025 and the first half of 2026 will be the "bridge" period where the savings from the Home segment restructuring begin to manifest in the bottom line. Analysts expect the Juvenile segment to continue its upward trajectory as product innovation in the car seat and stroller categories drives premium sales.

However, significant risks remain. The company’s high leverage and high beta (1.40) mean the stock is susceptible to broader market volatility and interest rate fluctuations. Furthermore, any disruption in global shipping or a resurgence in trade tariffs could impact the newly streamlined, import-heavy Home segment.

Conclusion

Dorel Industries’ 14.5% jump is a clear signal that the market is beginning to price in the potential of a leaner, more focused organization. By aggressively cutting the "dead weight" of underperforming domestic manufacturing and doubling down on its world-class Juvenile brands, Dorel is attempting a classic corporate turnaround. While the road to 2026 profitability still carries the burden of a heavy debt load, the operational milestones reached in the last two quarters have provided the necessary oxygen for this significant rally.

Please wait processing your request...

Please wait processing your request...