Eldorado Gold Corporation (TSX: ELD) experienced a decisive breakout during the January 21, 2026, trading session, with shares surging 4.9% to reach 62.24 CAD. This bullish momentum was ignited by the company’s dual announcement of hitting the upper end of its 2025 production guidance and providing a highly anticipated "transformational" update on its Greek development projects.

Investors responded enthusiastically to preliminary full-year gold production reaching 488,268 ounces, bolstered by a significant fourth-quarter recovery at the Olympias mine and continued operational excellence at the Lamaque Complex in Quebec. As the company prepares for the imminent first production at its world-class Skouries project in early 2026, the market is aggressively pricing in Eldorado's transition from a mid-tier producer to a diversified high-margin growth story.

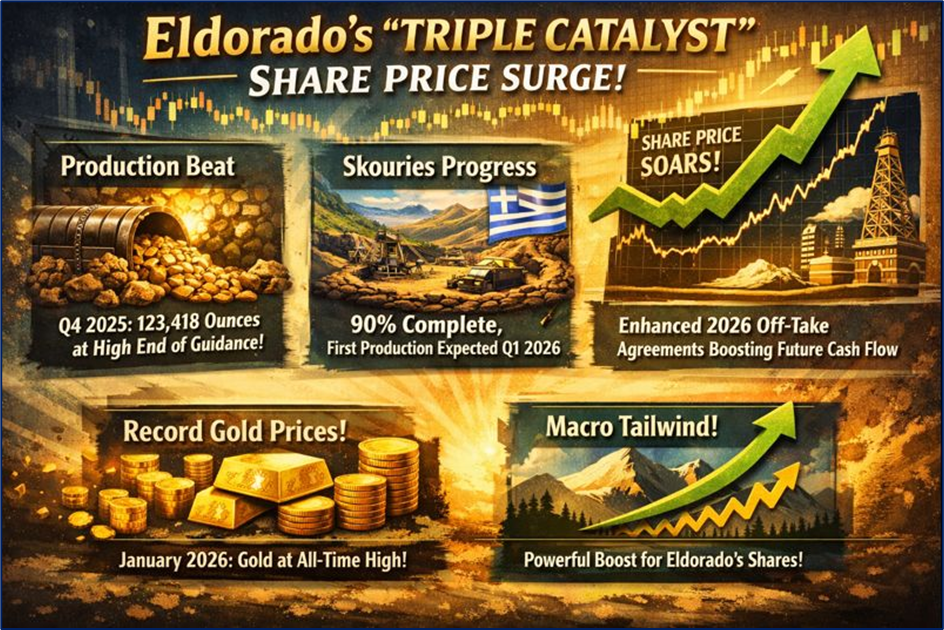

Latest Key Reasons for the Surge

Source: Kalkine Group

The recent jump in share price is primarily attributed to a rare "triple-catalyst" event: operational outperformance, de-risking of key growth projects, and a favorable macroeconomic tailwind.

- Production Beat: Preliminary Q4 2025 results showed production of 123,418 ounces, allowing the company to meet the high end of its annual guidance.

- Skouries Progress: The company confirmed that the Skouries project in Greece has reached 90% overall progress, with first concentrate production firmly on track for the end of Q1 2026.

- Improved Contract Terms: Eldorado revealed it has executed new concentrate off-take agreements for 2026 with "substantially improved payability" compared to 2025, directly enhancing future cash flow projections.

- Macro Environment: Gold prices hitting record levels in January 2026 have acted as a force multiplier for mining equities with high operational leverage like Eldorado.

Latest Drivers

Several internal and external drivers are currently dictating the stock's trajectory:

- Operational Stability in Greece: After facing processing challenges earlier in 2025, the Olympias mine saw a 36% quarter-over-quarter production increase in Q4, signaling that technical fixes are now yielding consistent results.

- Asset Diversification: The shift toward becoming a significant copper producer via Skouries is attracting a broader base of investors looking for exposure to the green energy transition alongside traditional gold hedging.

- Cost Management: While inflationary pressures persist, the company’s focus on "disciplined execution" at Kisladag and Efemcukuru in Turkey has helped stabilize all-in sustaining costs (AISC).

Latest Analyst Coverages

Major financial institutions have revised their outlooks following the January 2026 updates:

- BMO Capital Markets: Boosted the price target from $50.00 to $53.00, citing increased confidence in the 2026 production ramp-up (Source: BMO Capital Markets).

- Canaccord Genuity: Recently upgraded the stock from Hold to Buy with a price target of $54.00, noting the successful de-risking of the Greek portfolio (Source: Canaccord Genuity).

- National Bankshares: Restated an "Outperform" rating, increasing the target from $38.00 to $41.00 as technical milestones at Skouries were achieved (Source: National Bank Financial).

- CIBC World Markets: Maintains an "Outperformer" rating, highlighting the company’s ability to offset depletion at key operations (Source: CIBC World Markets).

Current Business Model

Eldorado Gold operates as an intermediate gold and base metals producer with a geographically diversified portfolio.

- Core Mining: The company manages four producing mines: Lamaque (Canada), Kisladag and Efemcukuru (Turkey), and Olympias (Greece).

- Growth Integration: The model is currently transitioning to include high-grade copper-gold concentrate production through the Skouries project.

- Vertical Strategy: Eldorado focuses on long-life, low-cost assets with significant exploration potential near existing infrastructure to maximize return on invested capital.

Financial and Operational Updates

Based on the January 2026 news releases and preliminary filings:

- Preliminary Production: Full-year 2025 production of 488,268 ounces of gold (Eldorado Gold Corp Source).

- Lamaque Complex: Produced 187,208 ounces in 2025, benefiting from the high-grade Ormaque bulk sample (Eldorado Gold Corp Source).

- Mineral Reserves: Released an updated statement showing successful offsetting of depletion and an increase in mineral reserves at key operations (Eldorado Gold Corp Source).

- Dividends: The dividend remains suspended as the company prioritizes capital allocation toward the completion of the Skouries project (Eldorado Gold Corp Source).

Outlook

The remainder of 2026 is viewed as a "transformational" year for Eldorado.

- Q1 2026: Expected first concentrate production at Skouries, marking the start of its copper-gold revenue stream.

- Q3/Q4 2026: Completion of the Olympias mill expansion to 650,000 tonnes per annum.

- Long-term: The company is advancing the Perama Hill project in Greece, with an updated feasibility study underway to support its next leg of growth.

Risks

- Geopolitical Exposure: Significant operations in Turkey and Greece expose the company to regional regulatory shifts and local community relations.

- Currency Fluctuation: The strength of the Euro against the US Dollar remains a risk for capital expenditure budgets in Greece.

- Technical Execution: Any delays in the final commissioning stages of the Skouries filtered tailings plant could impact the mid-2026 commercial production target.

Conclusion

Eldorado Gold’s surge to $62.24 CAD on January 21 reflects a market that is finally rewarding the company for consistent operational delivery and the tangible nearing of its growth goals. By meeting its 2025 guidance and clearing the path for Skouries, Eldorado has positioned itself as one of the most dynamic intermediate producers on the TSX heading into the 2026 fiscal year.

Please wait processing your request...

Please wait processing your request...