-Copy_01_29_2026_20_11_40_296448.jpg)

The Canadian retail landscape is undergoing a massive shift in January 2026 as Empire Company Limited (TSX: EMP.A) pivots its strategy to combat inflationary pressures and a cooling economy. With the S&P/TSX Composite Index navigating a high-interest-rate plateau and the CAD (Loonie) finding support amidst global trade volatility, investors are aggressively hunting for defensive moats.

Empire Company, the titan behind Sobeys, Safeway, and FreshCo, recently sent shockwaves through the market with a strategic e-commerce overhaul and a 10% dividend hike, marking its 30th consecutive year of increases (Empire Co. Source). As grocery inflation stabilizes and consumer behavior shifts toward discount banners, the question remains: is EMP.A the safest bet for your portfolio this quarter?

Latest Market Pulse: January 2026 Key Metrics

- Current Price: Approximately $45.46 - $46.25 (TSX: EMP.A)

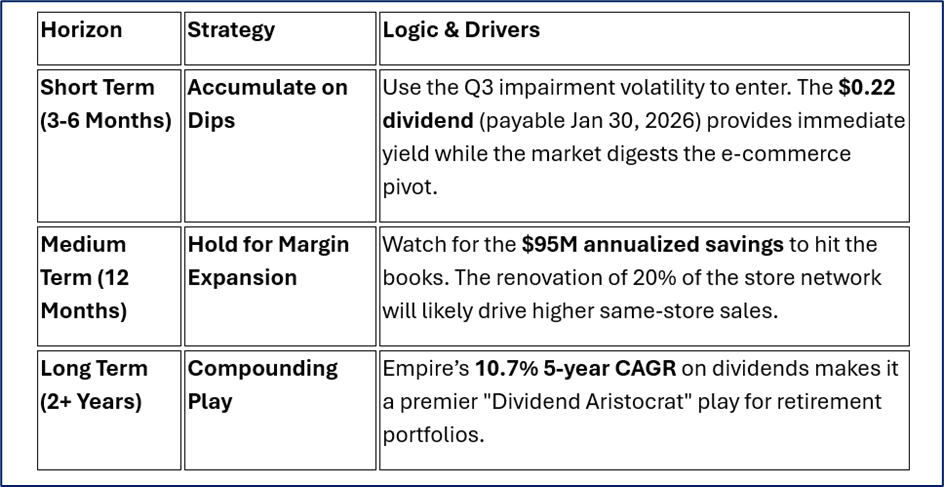

- Dividend Yield: 1.9% – 2.0% (Quarterly payout of $0.22/share)

- Recent Momentum: 10% dividend increase; $400 million share repurchase program renewed for fiscal 2026.

- Strategic Pivot: $750 million non-cash charge in Q3 2026 to rationalize e-commerce, shifting focus to high-margin delivery via DoorDash (Empire Co. Release).

Why is the Canada Economy Driving Empire’s 2026 Strategy?

The Canadian economy in early 2026 is a tale of two consumers. While the Bank of Canada holds the overnight rate near 2.25%, core inflation remains sticky at roughly 2.4%, forcing households to hunt for value (S&P Global). This "value-seeking" trend has been a massive tailwind for Empire’s Discount banners, which are currently outperforming full-service formats. As the TSX Composite trades at a P/E of 15.9x, Empire’s valuation at 15.0x offers a rare "quality-at-a-discount" opportunity. The CAD/USD exchange rate continues to impact import costs, but Empire’s focus on "Own Brands" expansion is shielding margins from global supply chain shocks.

Is Empire Company’s Business Model Future-Proof?

Empire is no longer just a traditional grocer; it is a data-driven retail powerhouse. By migrating to the SAP S/4HANA ERP platform and leveraging the Scene+ loyalty program, the company is capturing granular consumer data to optimize promotions. Their latest operational update reveals a bold move: winding down underperforming e-commerce fulfillment centers in Alberta to save $95 million annually by fiscal 2027 (Company Source). This pivot from high-cost infrastructure to lean, third-party delivery partnerships signal a management team focused on Free Cash Flow and bottom-line protection.

Should You Be Bullish or Bearish on EMP.A Today?

- Short-Term Outlook (Bearish/Neutral): The stock faces immediate pressure from a $750 million impairment charge related to e-commerce restructuring in Q3 2026. Technical indicators show the stock trading below its 200-day moving average, suggesting a period of consolidation.

- Long-Term Outlook (Bullish): The fundamentals are rock-solid. A 30-year dividend growth streak and a massive share buyback program provide a floor for the stock. As the e-commerce "rationalization" completes, the lean-and-mean Empire is positioned for significant EPS expansion. Analytical retail sentiment suggests that while the "sticker shock" of the impairment might hurt now, the resulting $95M in annual savings is a gift for long-term holders.

Forward-Looking Investor Strategies

Source: Kalkine Group Analysis

Top Analyst Ratings & Share Price Forecasts

The consensus among top-tier Canadian institutions remains cautiously optimistic, with an average price target of $52.00.

- RBC Capital: Reiterated Sector Perform with a target of $61.00 (September 2025).

- CIBC World Markets: Outperformer rating with a target of $53.00 (December 2025).

- BMO Capital: Market Perform (Hold) with a target of $51.00 (December 2025).

- Desjardins: Buy rating maintained with a target of $53.00 (December 2025).

Investor FAQ: Everything You Need to Know

When is the next Empire Company earnings date?

Empire is scheduled to release its Q3 2026 results on March 12, 2026, before the market opens.

Is the Empire Company dividend safe?

Yes. With a payout ratio of approximately 28% and 30 years of consecutive increases, the dividend is among the safest on the TSX.

What are the biggest risks for EMP.A?

Key risks include intensified competition from Walmart and Loblaws, potential labor disruptions, and the successful execution of the new DoorDash delivery strategy.

Conclusion: Buy, Sell, or Hold?

Analytical Verdict: ACCUMULATE/HOLD. Empire Company is currently a "coiled spring." The short-term pain of restructuring its e-commerce wing is hiding the long-term gain of a much more profitable, leaner business model. For income-seeking investors, the 10% dividend hike is a massive signal of management confidence. While the stock may remain range-bound until the March 2026 earnings, the valuation gap compared to peers like Metro (MRU) makes EMP.A a prime candidate for a valuation re-rating.

Please wait processing your request...

Please wait processing your request...