On January 20, 2026, G Mining Ventures Corp. (TSX: GMIN) surged 5% following the release of its comprehensive 2026-2027 operational guidance. The stock is currently trading at approximately CA$46.02 (implied from the 6.6% gain on previous close), reflecting massive investor confidence in the company’s transition from a single-asset developer to a multi-asset mid-tier producer.

Latest Key Drivers and Reasons for Today’s +6% Jump

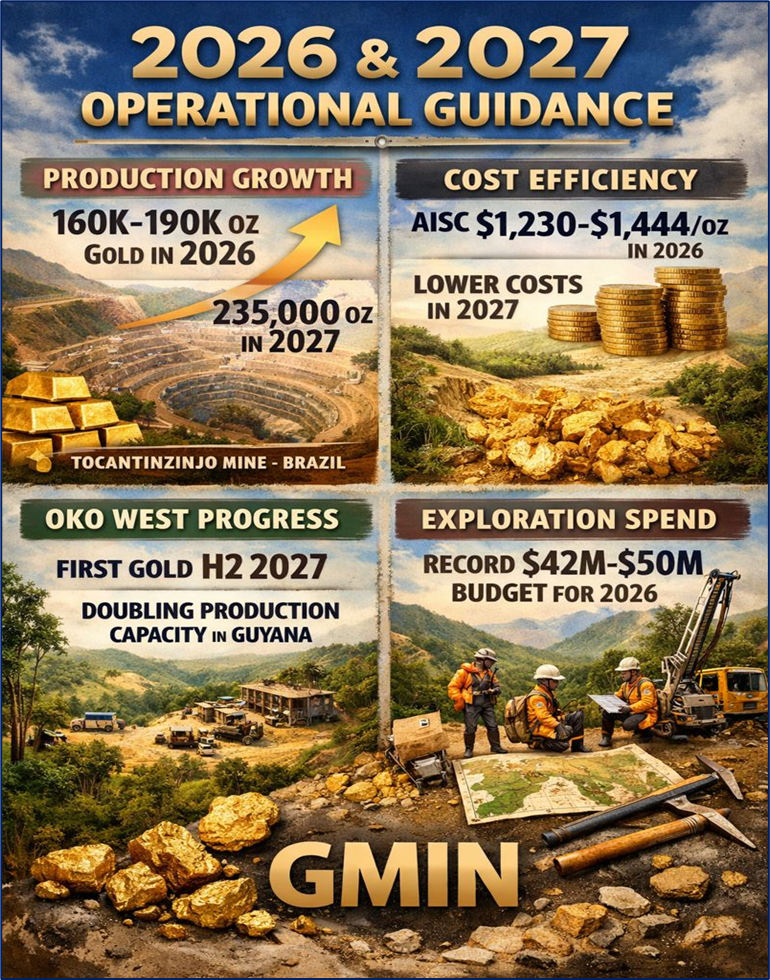

Source: Kalkine Group

The primary catalyst for today’s upward price action is the 2026 and 2027 Operational Guidance released this morning. Investors are reacting to:

- Production Growth: 2026 gold production is guided at 160,000 to 190,000 oz, with a massive 25% jump expected in 2027 (up to 235,000 oz) as higher-grade Phase 2 ore at the Tocantinzinho (TZ) mine in Brazil becomes available.

- Cost Efficiency: Despite global inflation, GMIN maintains a competitive AISC (All-In Sustaining Cost) guided between $1,230 and $1,444/oz for 2026, with costs expected to drop significantly in 2027.

- Oko West Progress: The company confirmed that its Oko West project in Guyana is on track for first gold in H2 2027, which is expected to double the company's total production capacity.

- Exploration Spend: A record $42M–$50M exploration budget for 2026 signals aggressive resource expansion, particularly at the Gurupi and Oko West sites.

Current Technical Analysis Paragraph

Technically, GMIN is exhibiting a strong bullish breakout from a consolidation pattern. As of today, January 20, the stock has cleared its immediate resistance at CA$41.50 on high relative volume. The Relative Strength Index (RSI) is trending toward 68, suggesting strong momentum without yet entering "overbought" territory (above 70). The stock is trading well above its 50-day and 200-day Moving Averages, which have formed a wide "Golden Cross" gap, typical of a sustained long-term uptrend. Today's 5% candle confirms a "base-on-base" breakout, with technical targets now shifting toward the CA$46.00 psychological level.

Latest Analyst Upgrades & Valuation

Wall Street and Bay Street remain overwhelmingly bullish.

- Price Targets: Average 12-month target has been revised upward today to CA$44.59, with some aggressive street targets reaching CA$51.00.

- Valuation: GMIN currently trades at a Forward P/E of approximately 26.6x. While higher than some legacy producers, this "growth premium" is justified by a forecast EPS growth of 22.6% per annum.

- Smart Money Sentiment: Institutional ownership has increased by 12% over the last quarter, with "Smart Money" funds like VanEck and Sprott increasing positions as the company de-risks its Guyana assets.

Business Model & Dividend Analysis

- Business Model: G Mining operates as a "Build-and-Operate" precious metals specialist. Unlike junior miners that sell projects, GMIN leverages its in-house "G Mining Services" expertise to build mines on time and on budget—a rare feat in the industry. They focus on low-cost, high-margin gold assets in mining-friendly jurisdictions (Brazil and Guyana).

- Dividend Analysis: As of January 20, 2026, G Mining does not pay a dividend. The company is in a "Hyper-Growth" phase, reinvesting 100% of free cash flow into the construction of Oko West and its record-breaking 2026 exploration program. Analysts do not expect a dividend initiation until Oko West reaches commercial production in 2028.

Financial and Operational Updates (Today)

- Cash Position: The company maintains a robust balance sheet with approximately $95M in cash and significant undrawn credit facilities, deemed sufficient to fund the $514M–$568M in growth CAPEX required for Oko West in 2026.

- Production Weights: Operational updates note that 2026 production will be weighted 62% toward the second half (H2), meaning the market is already pricing in a softer Q1 and Q2 in exchange for a massive year-end finish.

- Safety & ESG: Management highlighted a Lost Time Injury Frequency Rate (LTIFR) of 0.15, keeping them in the top decile of ESG performers among mid-tier miners.

Risks & Outlook

- Outlook: The outlook is exceptionally bright. By 2028, GMIN is projected to be a 500,000 oz/year producer. The immediate 2026 focus is the assembly of the initial mining fleet at Oko West and pre-production stripping in Brazil.

- Risks: Commodity Volatility: The 2026 guidance assumes a realized gold price of $4,000/oz. A significant drop in bullion prices would impact margins.

- Jurisdictional Risk: While Guyana is mining-friendly, geopolitical tensions in the region or changes in tax codes remain a background risk.

- Execution Risk: Any delay in the H2 2027 first gold target at Oko West would likely lead to a valuation re-rating.

Conclusion

G Mining Ventures represents a rare "growth-at-a-reasonable-price" (GARP) play in the gold sector. Today’s 5% jump is a direct endorsement of the management’s ability to forecast and deliver aggressive production growth while maintaining cost discipline. For investors, GMIN has transitioned from a speculative developer to a proven operator, with 2026 serving as the pivotal year for its multi-asset expansion.

Please wait processing your request...

Please wait processing your request...