The Catalyst: Why MDA Space is Topping the TSX Today

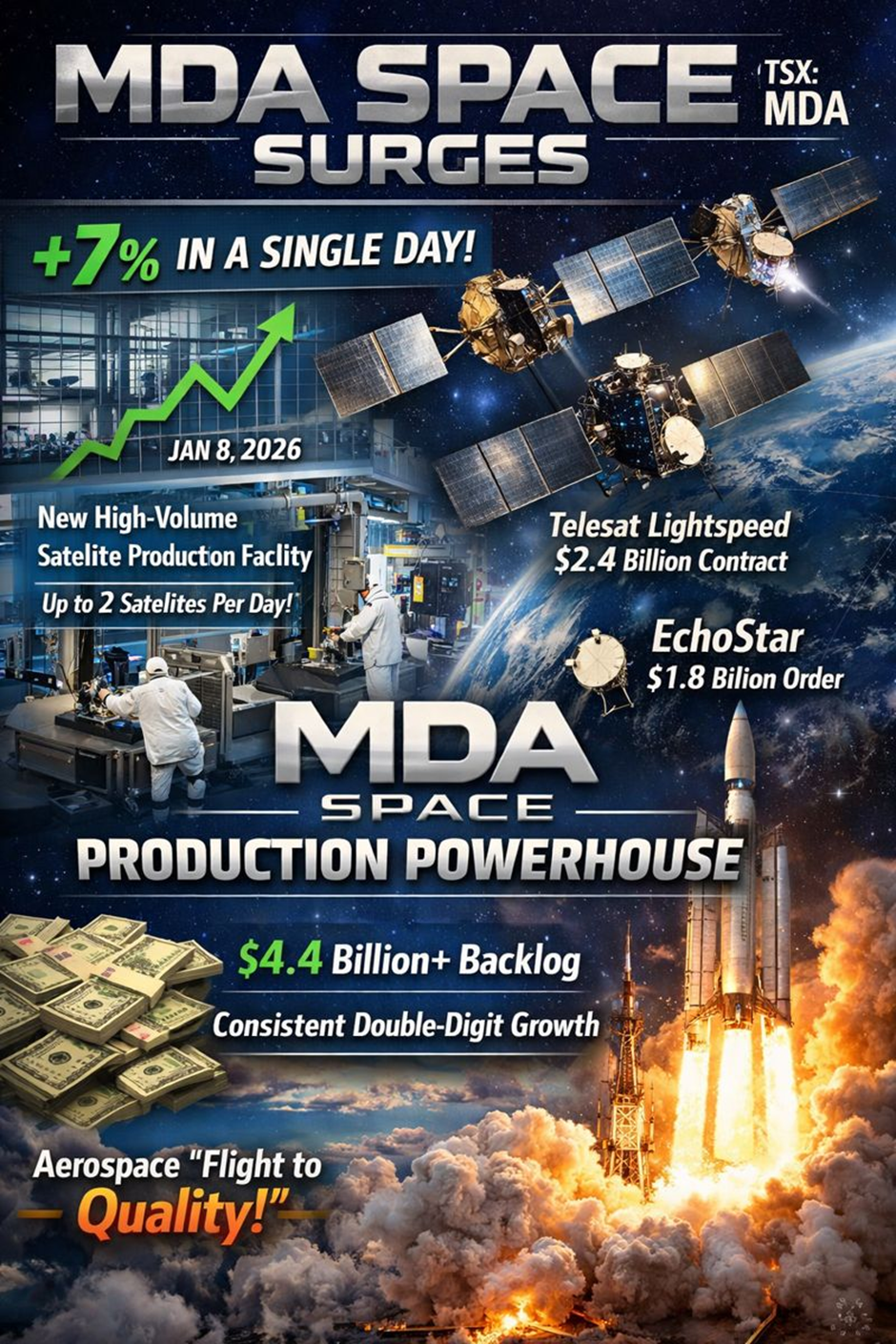

On January 8, 2026, MDA Space Ltd. (TSX: MDA) emerged as a standout performer, climbing approximately 7% in a single trading session. The primary driver behind this move is the market’s realization of the company’s transition from a "backlog builder" to a "production powerhouse."

Specifically, investors are reacting to the operational readiness of the newly expanded Montreal satellite production facility, which is now capable of producing up to two digital satellites per day. This massive scale-up is essential for fulfilling the anchor $2.4 billion Telesat Lightspeed contract and the $1.8 billion EchoStar order.

The stock is also benefiting from a "flight to quality" within the aerospace sector, as MDA remains one of the few players with a multi-billion dollar backlog (over $4.4 billion) and consistent double-digit revenue growth.

Source: Kalkine Group

Technical Analysis: The Bullish Breakout

From a technical perspective, today’s 7% surge has pushed the stock above its 50-day moving average of $25.69, signaling a potential reversal of the sideways consolidation seen in late 2025.

- Support and Resistance: The stock has established a firm floor around the $26.00 level. Today’s volume-backed move is challenging the immediate resistance at $28.50. A sustained close above this level could open the door to a retest of the $33.79 (200-day moving average).

- Indicators: The Relative Strength Index (RSI) has jumped from neutral territory toward 67, indicating increasing buying pressure without yet hitting "overbought" levels.

- Chart Pattern: A "cup and handle" formation appears to be developing on the weekly chart, suggesting that the long-term bullish trend that began in 2021 remains intact despite the volatility of the past year.

Source: Trading View

Latest Analyst Consensus: The "Buy" Signal

The Wall Street and Bay Street consensus remains overwhelmingly positive, with most analysts maintaining "Buy" or "Outperform" ratings as of January 2026.

- Upgrades and Price Targets: Stifel Canada recently upgraded the stock to a "Strong Buy," citing the derisking of the production ramp-up. While some firms like Desjardins and BMO Capital adjusted their price targets downward in late 2025 to reflect broader market multiples, the average one-year price target remains near $40.00, representing a significant upside from current levels.

- Fair Value Estimates: Independent research platforms like Simply Wall St suggest a narrative-driven fair value of approximately $40.19, though they caution that traditional Discounted Cash Flow (DCF) models may show lower values due to the heavy capital expenditure (CapEx) currently being deployed.

Business Model and Operational Updates

MDA Space has evolved into a diversified space infrastructure leader, operating through three primary pillars:

- Satellite Systems: Powered by the AURORA digital satellite product line. This software-defined technology is the company’s biggest growth engine, focusing on Low Earth Orbit (LEO) constellations for global broadband and direct-to-device connectivity.

- Robotics & Space Operations: The legacy of the Canadarm. MDA is currently developing Canadarm3 for the NASA-led Gateway (lunar orbit station) and is expanding into commercial on-orbit servicing.

- Geointelligence: Providing Earth observation data through RADARSAT-2 and the upcoming CHORUS constellation, which is scheduled for launch in late 2026. This segment provides high-margin recurring revenue through defense and environmental monitoring contracts.

Latest Financial Performance

The financial trajectory for MDA is characterized by rapid scaling:

- Revenue Growth: MDA reported Q3 2025 revenues of $410 million, a 45% year-over-year increase. For the full year 2025, the company guided for revenues between $1.57 billion and $1.63 billion.

- Profitability: Adjusted EBITDA margins have stabilized around 20%, with 2025 Adjusted EBITDA expected to reach $305–$320 million.

- Capital Structure: The company recently completed a $250 million debt refinancing to strengthen its balance sheet ahead of the 2026 production peak. Net debt-to-EBITDA remains healthy at roughly 0.3x to 0.8x (depending on the quarter), giving it significant room for further M&A or organic investment.

Critical Risks to Consider

Despite the bullish sentiment, several headwinds could impact the 2026 outlook:

- Execution Risk: Moving from prototype to high-volume manufacturing (two satellites/day) is a massive leap. Any delays in the Montreal facility’s output could lead to missed milestones and penalty clauses.

- Supply Chain & Inflation: As a prime contractor, MDA is vulnerable to rising costs of specialized components and labor, which could compress the current 20% EBITDA margins.

- Customer Concentration: A significant portion of the backlog is tied to a few mega-projects (Telesat, Globalstar, EchoStar). Any cancellation or funding delay from these anchor clients would be a major blow.

Conclusion

MDA Space is no longer just a "Canadian success story"; it is a global contender in the trillion-dollar space economy. Today's 7% gain reflects growing confidence that the company can successfully deliver on its massive $4.4 billion backlog. With the CHORUS launch and Canadarm3 milestones approaching in late 2026, the stock remains a primary vehicle for investors seeking exposure to space infrastructure and the digital connectivity revolution.

Please wait processing your request...

Please wait processing your request...