Is Power Corporation of Canada flying under the radar as a dependable dividend stock with valuation support in 2026? With steady price momentum, resilient cash flows, and a diversified financial empire behind it, POW (TSX:POW / OTC:PWCDF) is increasingly being discussed as a high-quality income play trading at a reasonable — and potentially discounted — multiple.

As of 5 February 2026, the stock is up ~2% on the day, outperforming several financial peers on the TSX, while maintaining a forward dividend yield near 3.7% and a P/E around 13.8x. That combination of income, stability, and valuation discipline is exactly what dividend-focused investors are hunting for in today’s market.

Power Corporation Stock Performance Snapshot (February 2026)

Recent trading action and longer-term trends point to improving investor confidence:

- +2% gain on 5 Feb 2026, supported by rising volumes

- Strong 1-year total return, firmly in positive territory

- Growing net asset value (NAV) per share and solid liquidity position

- Momentum supported by insurance, wealth management, and asset management exposure

Together, these signals suggest the market is gradually repricing Power Corp as a dependable compounder rather than a slow-moving financial conglomerate.

How Strong Is Power Corporation’s Dividend in 2026?

For Canadian income investors, dividend durability matters more than headline yield — and this is where Power Corp quietly shines.

Dividend Strength at a Glance

- Forward yield: ~3.6%–3.8%, attractive vs many TSX financial peers

- Payout ratio below 50%, indicating healthy earnings coverage

- Quarterly dividends with a multi-year growth record

- Cash flows diversified across insurance, wealth, and asset management

Compared with many legacy Canadian dividend stocks that face earnings pressure or limited growth, Power Corporation’s dividend profile remains balanced, sustainable, and inflation-resilient.

Macro Tailwinds: TSX Composite & Canada’s 2026 Outlook

Is the TSX Supportive for Financial Stocks in 2026?

The broader TSX Composite backdrop remains constructive:

- Expectations of record index levels supported by easing rate policy

- Financials, insurance, and asset managers benefit from liquidity and economic stability

- Strong commodity and trade fundamentals underpin Canadian equity sentiment

Lower interest rates tend to support asset valuations and wealth flows — both key drivers for Power Corp’s core businesses.

Canada’s Economic Impact on POW

Canada’s 2026 economic environment features:

- Moderating inflation

- Resilient consumer spending

- Stable exports to the U.S.

These conditions are broadly favorable for insurers and wealth managers. That said, global growth slowdowns and geopolitical uncertainty remain risks for investment returns and fee-based margins.

Power Corporation’s Business Model: Built for Stability

Power Corporation operates as a diversified financial holding company with exposure across multiple income streams:

- Life insurance & retirement solutions

- Wealth management via IGM Financial

- Global asset investments through GBL

- Alternative assets and selective fintech investments

This structure helps smooth earnings across cycles, reduce volatility, and support consistent shareholder distributions. Management continues to prioritize AUM growth, capital efficiency, and strategic partnerships heading into late 2025 and beyond.

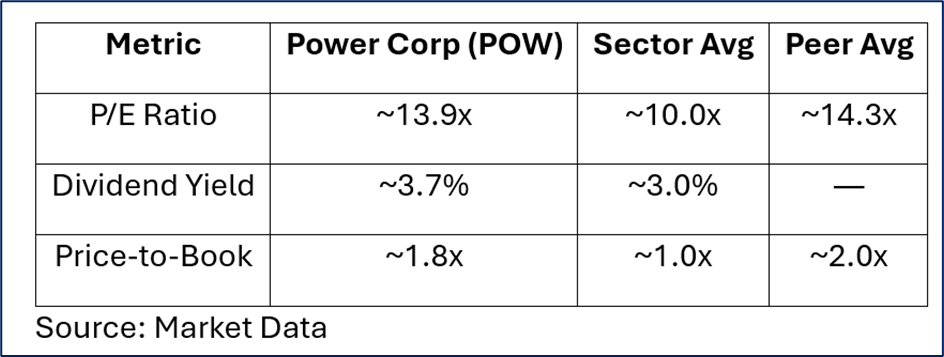

Valuation Check: How Does POW Compare With Peers?

The takeaway? Power Corp trades at a reasonable valuation, offers above-average income, and maintains solid balance-sheet strength relative to peers.

Analyst Outlook: What’s the Market Expecting?

- Consensus remains neutral to mildly positive

- Average price targets cluster around CA$70–71

- Dividend reliability is consistently cited as a valuation anchor

Analysts remain cautious on growth acceleration but acknowledge the stock’s defensive income appeal in uncertain macro conditions.

Bull, Base & Bear Cases for Power Corporation

Bull Case

- Reliable dividends attract long-term capital

- Diversified global exposure dampens volatility

- TSX upside and economic resilience support financials

- NAV growth aligns with earnings expansion

Bear Case

- Global slowdown pressures asset management fees

- Insurance and wealth cycles soften earnings momentum

- Geopolitical risks limit international optionality

Base Case (Most Likely)

- Steady dividends + moderate growth

- Range-bound price action with income-led total returns

Scenario Matrix: What Could Happen Next?

Forward-Looking Investor Playbook (Informational Only)

Short Term (3–6 months)

- Track TSX momentum and rate expectations

- Watch earnings updates and AUM trends

Medium Term (6–18 months)

- Focus on dividend growth and payout safety

- Compare relative strength vs insurers and asset managers

Long Term (2–5+ years)

- Evaluate diversification benefits through cycles

- Monitor global exposure and capital allocation discipline

FAQs: Power Corporation of Canada in 2026

What is Power Corporation’s dividend yield in 2026?

Approximately 3.6%–3.8% forward, paid quarterly and well covered by earnings.

Is POW bullish or bearish in the short term?

Short-term outlook is mixed, with dividend support offsetting market volatility.

How does POW compare with TSX financial peers?

It offers competitive valuation, reliable income, and broader diversification.

What macro factors matter most for POW?

Interest rates, TSX Composite trends, Canada’s economy, and global risk sentiment.

Final Takeaway: A Steady Dividend Compounder in 2026

As of February 2026, Power Corporation of Canada stands out as a high-quality, dividend-focused financial stock with diversified revenue streams and disciplined capital management. While not a high-growth story, its income reliability, valuation support, and business resilience position it well for investors seeking steady total returns.

In short: POW may not shout for attention — but for long-term, income-oriented investors, that quiet consistency could be exactly the point.

Please wait processing your request...

Please wait processing your request...