The Canadian energy sector just witnessed a massive jolt as Prairie Provident Resources Inc. (TSX: PPR) saw its stock price surge by approximately 70% in early January 2026.

While penny stocks in the oil and gas space are known for volatility, this specific move has retail investors and analysts digging through SEDAR+ filings to understand if this is a fundamental shift or a technical anomaly.

The "Big Bang" Driver: The 30-to-1 Share Consolidation

Source: Kalkine Group

The primary catalyst behind the sudden "70% increase" in the trading price on January 6, 2026, is a major structural change: a 30-to-1 reverse stock split (share consolidation).

As of December 31, 2025, Prairie Provident officially reduced its massive share count from approximately 1.4 billion shares to roughly 46.7 million. While a consolidation doesn't change the underlying value of the company, it often triggers significant price action for three reasons:

- Exchange Compliance: It moves the stock out of the "sub-penny" range (where it was trading at roughly $0.02 - $0.03) to a more "respectable" dollar figure, potentially attracting institutional interest.

- Liquidity Squeeze: The reduction in float can lead to high volatility as the market adjusts to the new "post-consolidation" trading price.

- TSX Listing Safety: The company previously utilized "financial hardship" exemptions. This move is a strategic attempt to satisfy TSX listing requirements and avoid delisting.

Latest Business Model: The "Michichi Strategy"

Prairie Provident has pivoted its business model toward low-risk, high-return development of existing assets rather than aggressive, expensive exploration.

- Core Focus: The Michichi and Princess areas in Southern Alberta.

- The "Basal Quartz" Engine: The company is betting heavily on the Basal Quartz (BQ) formation. Their latest model involves using horizontal drilling to unlock light/medium oil from these established fields.

- Waterflood Optimization: In the Evi area (Peace River Arch), they are employing secondary recovery (waterflooding) to maintain stable production and mitigate natural decline rates.

Financial & Operational Update (Q1 2026 Context)

The rally isn't just about the split; it's backed by a series of aggressive balance sheet cleanups completed in late 2025:

- Capital Injection: In November 2025, the company closed a $26.5 million preferred share financing. This provided the "oxygen" needed to fund the 2026 drilling program.

- Debt Lifeline: Maturity dates for First Lien Loans and Second Lien Notes were extended by 24 months (now pushing into 2028). Crucially, they secured the ability to defer cash interest payments through 2026, preserving precious cash flow.

- Production Metrics: As of the last report, production was averaging ~2,300 boe/d (with a high 57–60% liquids weighting).

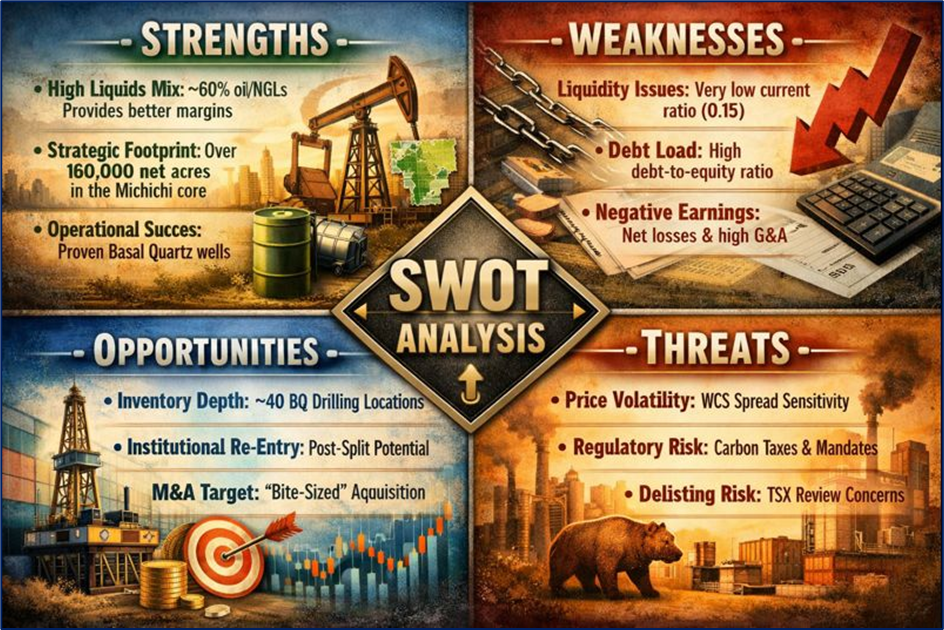

SWOT Analysis (Analytical Breakdown)

Source: Kalkine Group

Key Risks to Watch

Despite the 70% surge, Prairie Provident is a high-risk play.

- The "Reverse Split" Curse: Historically, many stocks that consolidate continue to face downward pressure if the underlying business doesn't turn profitable quickly.

- Altman Z-Score: Financial models still place the company in the "distress zone," suggesting that while the debt extensions helped, the company must execute perfectly on its 2026 drilling program to survive.

- Capital Intensity: If oil prices dip below $65-$70 USD, the "Operating Netback" may not be enough to cover the development costs of new wells.

Conclusion

The 70% jump on January 6, 2026, marks a "New Chapter" for Prairie Provident. By consolidating shares and pushing debt maturities into the future, management has bought the company time. The market is currently reacting to a tighter share structure and the successful completion of a $26.5M financing round. However, the true test will be the results of the upcoming Michichi drilling pad. For retail investors, the stock remains a high-beta bet on Alberta's Basal Quartz play.

Please wait processing your request...

Please wait processing your request...