Diversified operations, disciplined capital allocation, and exposure to essential infrastructure markets are positioning Russel Metals (TSX:RUS) as a compelling cyclical dividend opportunity in February 2026. As steel prices stabilize and North American industrial demand strengthens, investors are revisiting this Canadian materials leader for both yield and recovery upside.

Key Takeaways – February 2026 Market Update

- Russel Metals shares gained approximately 3% on 12 February 2026, outperforming segments of the S&P/TSX Composite Index

- Stabilising steel prices and improving North American construction demand boosted investor sentiment

- Canada’s resilient GDP growth and stable CAD supported materials sector flows

- Dividend yield remains attractive relative to TSX industrial and materials peers

- Short-term technical structure turning bullish; long-term outlook remains steel-cycle dependent

Why Is Russel Metals Rising in February 2026?

Global markets are showing renewed risk appetite as inflation moderates across North America and central banks signal policy stability. Commodity-linked equities, particularly steel distributors, are benefiting from rotation into value and cyclical sectors.

Key macro tailwinds include:

- US infrastructure expansion

- Energy pipeline and LNG investment

- Automotive production recovery

- Defence and heavy industrial growth

- Improving global manufacturing PMI readings

- China stimulus measures supporting base metals demand

Steel pricing has moved from 2025 volatility toward stabilization — historically a favourable environment for service center operators like Russel Metals.

Is the Canadian Economy Supporting a Materials Sector Revival?

Canada’s February 2026 macro backdrop remains constructive:

- Stable employment trends

- Moderating inflation

- Stronger-than-expected Q4 GDP

- Resilient housing starts

A relatively stable Canadian dollar versus USD reduces cost volatility for steel importers and distributors, improving margin visibility.

Sector rotation within the TSX has favoured energy and materials, directing fresh capital into companies with exposure to infrastructure and industrial recovery themes.

Russel Metals Business Model: Built for Cyclical Stability

Russel Metals operates across three primary segments:

- Metals Service Centers

- Energy Products

- Steel Distributors

Its diversified North American footprint reduces single-market risk while providing exposure to:

- Construction

- Energy infrastructure

- Industrial manufacturing

Core strengths include:

- Conservative inventory management

- Strong balance sheet flexibility

- Disciplined acquisitions strategy

- Focus on free cash flow generation

- Consistent dividend framework

Historically, the company performs best during steel price normalization phases rather than speculative peak pricing environments.

How Does TSX:RUS Compare With Peers?

Relative to Canadian industrial and materials stocks:

- Higher dividend yield than many TSX industrial peers

- Lower valuation multiples versus pure-play steel producers

- More diversified revenue base than single-product steelmakers

- Moderate earnings multiple reflecting cyclical sensitivity

The stock is not deeply undervalued — but it is not priced for peak-cycle optimism either.

Technical & Fundamental Outlook (February 2026)

Short-Term (3–6 Months)

Momentum indicators show improving structure following the 3% surge. Materials sector strength supports a mildly bullish bias.

Outlook: Mildly Bullish

Medium-Term (6–18 Months)

Performance will depend on:

- US infrastructure execution

- Energy capital expenditure trends

- Steel margin normalization

Outlook: Neutral-to-Constructive

Long-Term (2–5 Years)

Longer-term drivers include:

- Infrastructure megatrends

- Energy transition steel demand

- North American reshoring

Outlook: Constructively Cyclical

Analyst Consensus – February 2026

Based on recent Canadian brokerage commentary:

- Majority rating: Hold to Moderate Buy

- Consensus price targets imply mid-single-digit upside

- Valuation aligned with normalized steel margin expectations

Risk-reward appears balanced rather than aggressively asymmetric.

What Triggered the 3% Move?

The recent rally likely reflects:

- Steel price stabilization headlines

- Improved TSX materials ETF inflows

- Stronger North American manufacturing data

- Yield-driven buying amid market volatility

- Technical breakout patterns

No major company-specific news appears to have driven the surge.

Key Risks to Monitor

- Steel price downturn

- Construction or energy demand slowdown

- Inventory valuation adjustments

- CAD currency volatility

- Global recession shock

Cyclical exposure remains the primary investment risk factor.

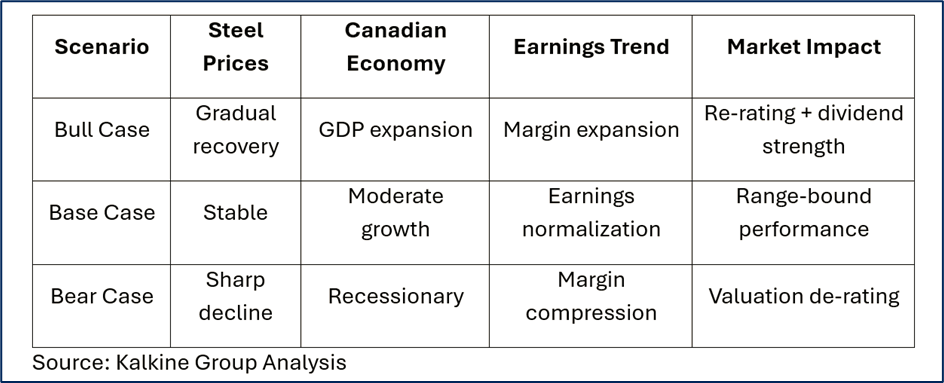

Bull, Base & Bear Case Scenarios

Is Russel Metals a True Recession-Resistant Dividend Stock?

Russel Metals offers cyclical income exposure, not a classic defensive dividend profile.

Why income investors consider it:

- Attractive yield relative to TSX average

- Historically disciplined payout policy

- Strong free cash flow focus

Why caution is required:

- Earnings tied directly to steel cycle

- Dividend sustainability linked to normalized margins

- Not immune to economic contraction

It is better classified as a cyclical dividend compounder rather than a recession-proof defensive stock.

Frequently Asked Questions (FAQ)

Why is Russel Metals stock up today?

The stock gained roughly 3% on 12 February 2026, likely due to steel price stabilization and improved materials sector momentum.

Is Russel Metals a good dividend stock in 2026?

It offers an above-average yield versus TSX peers but remains sensitive to steel market cycles.

Is TSX:RUS bullish right now?

Short-term technical momentum is improving; longer-term direction depends on steel demand sustainability.

What are analysts forecasting?

Consensus ranges from Hold to Moderate Buy with moderate upside expectations.

Final Investment Verdict – February 2026

Russel Metals is positioned within a stabilizing steel cycle, supported by resilient Canadian macro conditions and improving North American infrastructure activity. The recent 3% surge reflects cyclical optimism rather than structural transformation.

For investors seeking:

- Dividend yield exposure within TSX materials

- Participation in infrastructure and industrial recovery

- Balanced cyclical risk with disciplined management

Russel Metals represents a measured, income-oriented cyclical opportunity in 2026.

It is not recession-proof — but it is structurally stronger than many pure-play steel producers, making it a compelling watchlist candidate as the steel cycle evolves.

Please wait processing your request...

Please wait processing your request...