Key Takeaways (January 2026)

- Share Price: Trading around $17.57, up roughly 16% year-over-year, outperforming many cyclical TSX names.

- Dividend: $0.10 quarterly payout intact (≈ 2.3% yield), with the latest distribution paid January 15, 2026.

- Strategic Shift: Rebranded from Secure Energy to Secure Waste Infrastructure Corp., underscoring its move into higher-margin environmental services.

- Revenue Quality: 80%+ recurring revenue, driven by mandatory industrial waste compliance and produced-water infrastructure.

- Street View: Analysts maintain a Moderate Buy stance, with price targets stretching to $23.50.

SES Stock in 2026: Is the Momentum Real or Just Noise?

The share price of Secure Waste Infrastructure Corp. has quietly become a magnet for investors hunting defensive TSX dividend stocks with ESG credentials. While the S&P/TSX Composite Index has flirted with record highs above 33,000, capital is rotating away from frothy growth and into essential infrastructure plays—and SES fits that bill neatly.

This isn’t the old SECURE Energy story anymore. The business is now dominated by produced-water disposal, hazardous waste treatment, and metal recycling—services customers can’t simply cut during downturns. Add in Canada’s steady macro backdrop and a Bank of Canada policy rate holding at 2.25%, and SES is starting to look less like a cyclical energy stock and more like a regulated-style utility.

Bottom line: The stock’s strength isn’t speculative—it’s structural.

Canada’s 2026 Economy & Why It Matters for SES

Macro conditions are quietly lining up in SES’s favor:

- Canada GDP (2026E): ~1.9% growth, with infrastructure and energy remaining core pillars.

- Industrial Trends: Environmental compliance is no longer optional. Producers are outsourcing waste handling to specialists with scale and permits.

- Market Tailwinds: The global waste management market is expected to compound at ~5.5% CAGR through 2034, reaching $2.2 trillion.

Because SES operates mainly in Western Canada, it benefits from domestic pricing power and reduced FX exposure—even while the CAD/USD pair remains volatile.

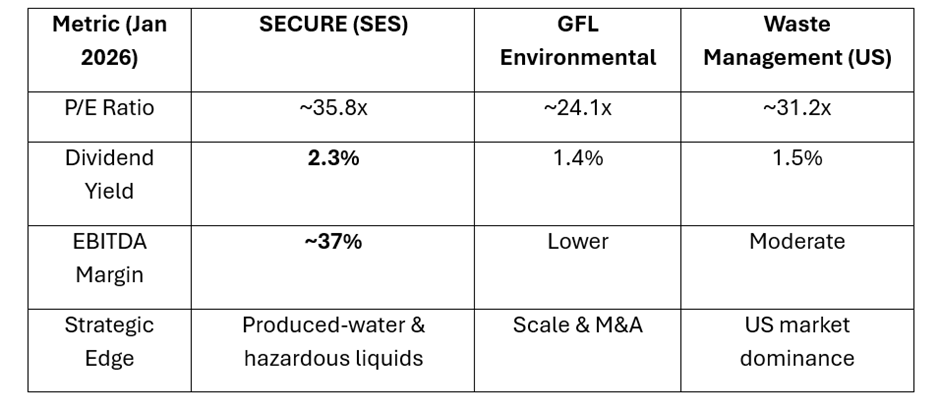

SES vs. Peers: How Does It Stack Up?

Compared with global giants like Waste Management and GFL Environmental, SECURE trades at a premium—but for good reason.

Source: Market Data

SES’s infrastructure-heavy, specialized assets deliver margins many traditional waste haulers simply can’t match.

2026 Outlook: Bull Case vs. Bear Case

Short Term (3–6 months): Neutral to Bullish

- Shares are consolidating after pulling back from the $21.15 52-week high.

- The NCIB renewal (up to 8.8% of shares) provides downside support.

- Recent $300M senior unsecured note issuance improves liquidity but may cap near-term upside.

Medium to Long Term (1–3 years): Clearly Bullish

- The revenue mix is now largely decoupled from oil price volatility.

- Higher North American production and the upcoming CUSMA review imply more—not less—waste and water-handling demand.

- Free cash flow supports dividends + buybacks simultaneously.

Analyst Ratings & Price Targets

Broker sentiment continues to trend positive:

- Stifel Canada: Buy — $23.50

- National Bank: Outperform — $23.00

- Raymond James: Outperform — $22.00

- Scotiabank: Sector Perform — $20.00

- CIBC: Hold — $19.00

Consensus target: ~$20.19, implying ~15% upside plus dividends.

Key Risks to Watch

- Regulatory risk: Changes in Alberta landfill or disposal rules could pressure margins.

- Interest rates: Capital-intensive assets mean higher-for-longer rates aren’t ideal.

- Regional exposure: A sharp downturn in Western Canadian production would hit volumes.

Investor FAQs

Why the rebrand to SECURE Waste Infrastructure?

To reflect that 75–80% of EBITDA now comes from environmental waste services, not traditional energy support.

Is the dividend safe in 2026?

Yes. Payouts are backed by recurring free cash flow and improved debt maturity profiles.

When are earnings next due?

Full-year 2025 results and 2026 guidance are expected February 2026.

Final Verdict: Buy, Hold, or Sell?

For investors looking for a defensive TSX stock with real growth and ESG credibility, SECURE Waste Infrastructure (TSX: SES) stands out as a BUY.

Strategy:

Accumulate on dips below $17.00

Collect a 2.3% dividend while waiting for infrastructure-driven upside

Why it works: Mandatory environmental compliance, sticky recurring revenue, and disciplined capital returns give SES a long runway into—and beyond—2026.

Please wait processing your request...

Please wait processing your request...