Telus (TSX: T): Navigating an 8.7% Dividend Yield in a Transformative Era

As 2026 unfolds, Telus Corporation has emerged as a focal point for income-seeking investors, presenting a staggering 8.7% dividend yield that stands as one of the most significant payouts among North American blue-chip entities. This yield surge is not merely a product of corporate generosity but a complex reflection of a stock price that has retracted significantly from historical highs, coupled with a management team that is aggressively pivoting its capital allocation framework.

While the company has paused its storied history of semi-annual dividend increases, its commitment to maintaining the current nominal payout of $0.4184 per quarter signals a defensive stance intended to bridge the gap until its massive infrastructure investments in PureFibre and 5G begin to yield higher free cash flow (FCF). In a market defined by volatile interest rates and shifting consumer habits, Telus finds itself at a critical crossroads, balancing its legacy as a dividend aristocrat with a modern necessity for deleveraging and technological diversification.

Latest Drivers and Reasons for the Yield Surge

Source: Kalkine Group

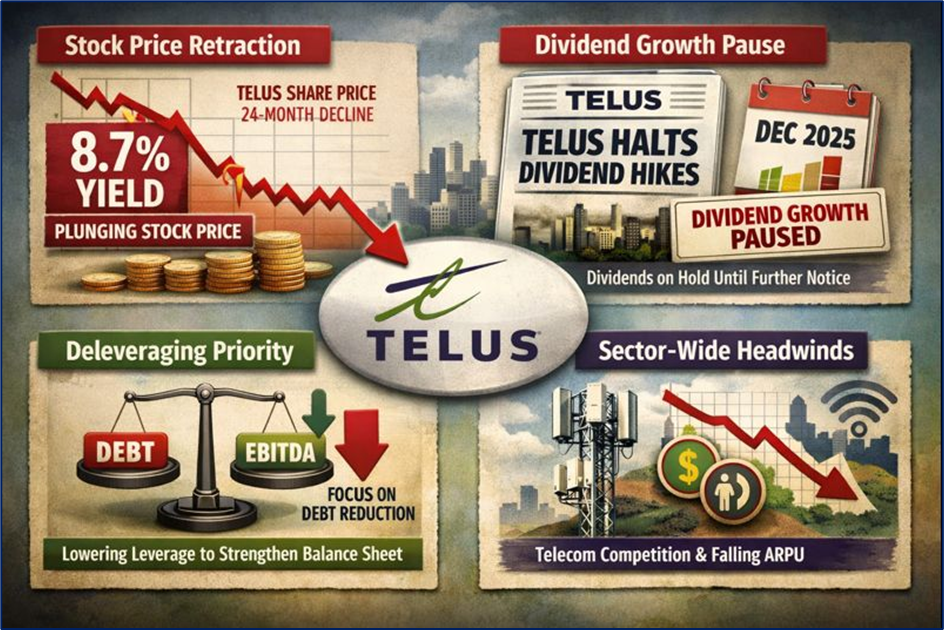

- Stock Price Retraction: The primary mechanical driver of the 8.7% yield is the significant decline in Telus’ share price over the past 24 months. Higher interest rates and investor concerns regarding debt levels have pressured the valuation, naturally elevating the yield for new entrants.

- Dividend Growth Pause: In late December 2025, Telus announced a formal pause in its dividend growth program. Management stated that further increases would be suspended until the share price more accurately reflects the company's growth prospects and deleveraging milestones (Source: TELUS Investor Relations, Dec 2025).

- Deleveraging Priority: The company is currently prioritizing the reduction of its net debt to adjusted EBITDA ratio. The shift in focus from increasing payouts to strengthening the balance sheet has caused some yield-sensitive investors to exit, contributing to the current stock pricing.

- Sector-Wide Headwinds: Intense competition in the Canadian wireless market and declining Average Revenue Per User (ARPU) for legacy services have created a cautious sentiment across the entire Canadian telecom sector.

Current Business Model: Beyond Connectivity

- TTech (Technology Solutions): This remains the core engine, comprising wireless and fixed connectivity. Telus is currently completing its transition from legacy copper to the high-speed PureFibre network, which now covers over 90% of its eligible footprint.

- TELUS Digital (formerly Telus International): This segment provides AI-integrated customer experience (CX) and digital transformation services. In 2026, the company is focusing on $150 million to $200 million in annual synergies following the privatization and rebranding of this unit (Source: TELUS Media Release, Nov 2025).

- TELUS Health: A global leader in digital health solutions, covering over 160 million lives. The company has recently engaged financial advisors (TD Securities and Jefferies) to seek strategic partners for this division, aiming to monetize its $5 billion+ valuation (Source: TELUS Corporate Update, Jan 2026).

- AI Infrastructure: Telus has launched Canada’s first "Sovereign AI Factory" in partnership with NVIDIA, positioning itself as a provider of secure, Canadian-hosted AI compute for government and enterprise clients.

Latest Financial, Operational, and Dividend Updates

- Free Cash Flow Targets: Telus has set a preliminary 2026 FCF target of $2.4 billion, projecting a minimum 10% compounded annual growth rate (CAGR) through 2028 (Source: TELUS Three-Year Outlook, Dec 2025).

- Debt Management: On January 16, 2026, the company completed the full redemption of C$600 million in 3.75% Notes. This was funded by a December 2025 "Hybrid Note" offering that raised approximately C$2.9 billion (Source: TELUS Financial Release, Jan 2026).

- Dividend Status: The quarterly dividend remains at $0.4184 per share. The company’s dividend payout ratio guideline is now targeted at 60% to 75% of free cash flow on a prospective basis through 2028 (Source: TELUS Dividend Information Page, 2026).

- DRIP Changes: The Discounted Dividend Reinvestment Plan (DRIP) is being systematically stepped down. The discount will move from 2% to 1.75% in early 2026, eventually hitting zero by 2028 to reduce share dilution (Source: TELUS Capital Allocation Framework, Dec 2025).

- Insider Confidence: Between November 2025 and January 2026, senior leadership, including CEO Darren Entwistle, acquired over 357,000 additional shares on the open market, demonstrating internal conviction (Source: TELUS Insider Filing, Jan 2026).

Latest SWOT Analysis

Source: Kalkine Group

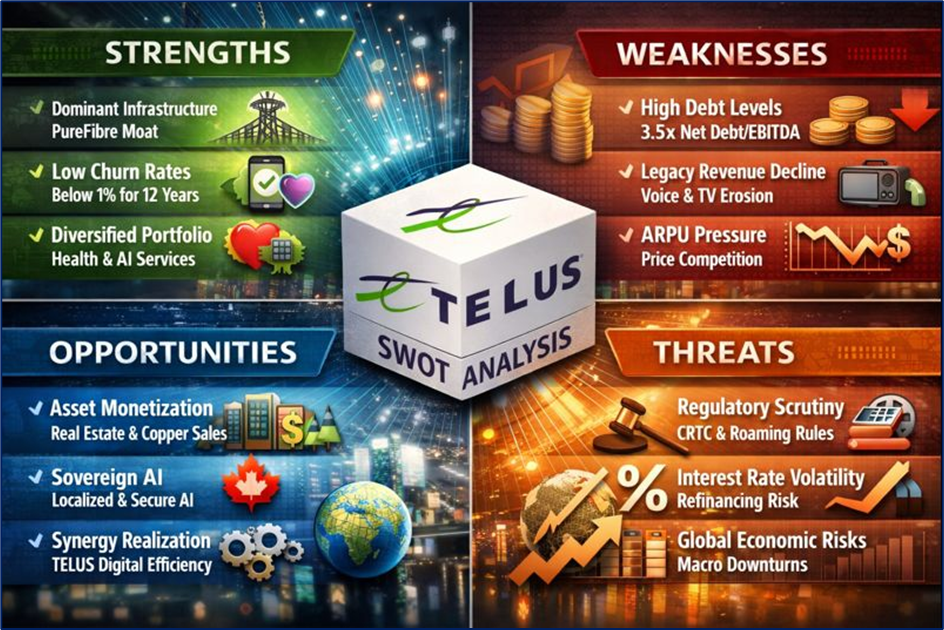

Strengths

- Dominant Infrastructure: Completion of the PureFibre build-out provides a significant moat against cable competitors.

- Low Churn Rates: Telus maintains industry-leading postpaid mobile churn, consistently below 1% for 12 consecutive years.

- Diversified Portfolio: Significant revenue contribution from non-telecom sectors like Health and Digital AI services.

Weaknesses

- Debt Profile: A net debt to EBITDA ratio currently hovering around 3.5x, which remains high compared to historic levels.

- Legacy Revenue Declines: Continuous erosion of high-margin legacy voice and TV services.

- ARPU Pressure: Intense price competition in the wireless segment is depressing monthly revenue per user.

Opportunities

- Asset Monetization: Potential for multi-billion dollar infusions from selling real estate or copper assets and partnering in the Health division.

- Sovereign AI: Capturing the growing demand for localized and secure AI compute in Canada.

- Synergy Realization: Consolidating TELUS Digital to improve margins and operational efficiency.

Threats

- Regulatory Environment: Ongoing scrutiny from the CRTC regarding wholesale wireline access and roaming rates.

- Interest Rate Volatility: High debt levels make the company sensitive to the cost of refinancing.

- Global Macro Risks: Economic downturns affecting the TELUS Digital segment's international enterprise clients.

Outlook and Risks

The outlook for Telus through the remainder of 2026 is centered on "execution over expansion." The company expects its capital expenditure (CapEx) to stabilize at approximately $2.3 billion as the heaviest phase of the fiber build-out concludes. This transition is intended to unlock the 10% FCF growth target, which management views as the primary mechanism for deleveraging. However, risks remain prominent; any failure to meet FCF targets could jeopardize the sustainability of the current dividend level, as the payout ratio currently exceeds 100% of FCF on a trailing basis. Furthermore, while the monetization of Telus Health represents a significant potential catalyst, the timing and valuation of such a deal are subject to global market conditions.

Conclusion

Telus presents a unique profile in 2026: a legacy telecom giant operating with the aggressive strategic shifts of a growth-focused tech firm. Its current 8.7% yield reflects a market that is pricing in both the high-interest-rate environment and the company's elevated debt levels. By pausing dividend growth and focusing on a "Sovereign AI" future and asset monetization, Telus is attempting to transform its financial foundation. For the market, the story of 2026 will be whether the company’s massive infrastructure bets can finally translate into the robust free cash flow growth promised by management to secure its dividend and deleverage its future.

Please wait processing your request...

Please wait processing your request...