As the global economy shifts into 2026, the Canadian utility sector has transformed from a "sleepy" defensive play into a high-conviction "wealth compounding" machine. The convergence of artificial intelligence (AI) data centre demand, aggressive decarbonization mandates, and a moderating interest rate environment has created a unique window for "multibagger" potential within large-cap TSX utilities.

While traditionally known for stability, specific players are now being rerated by "smart money" and global fund managers as growth-oriented infrastructure titans.

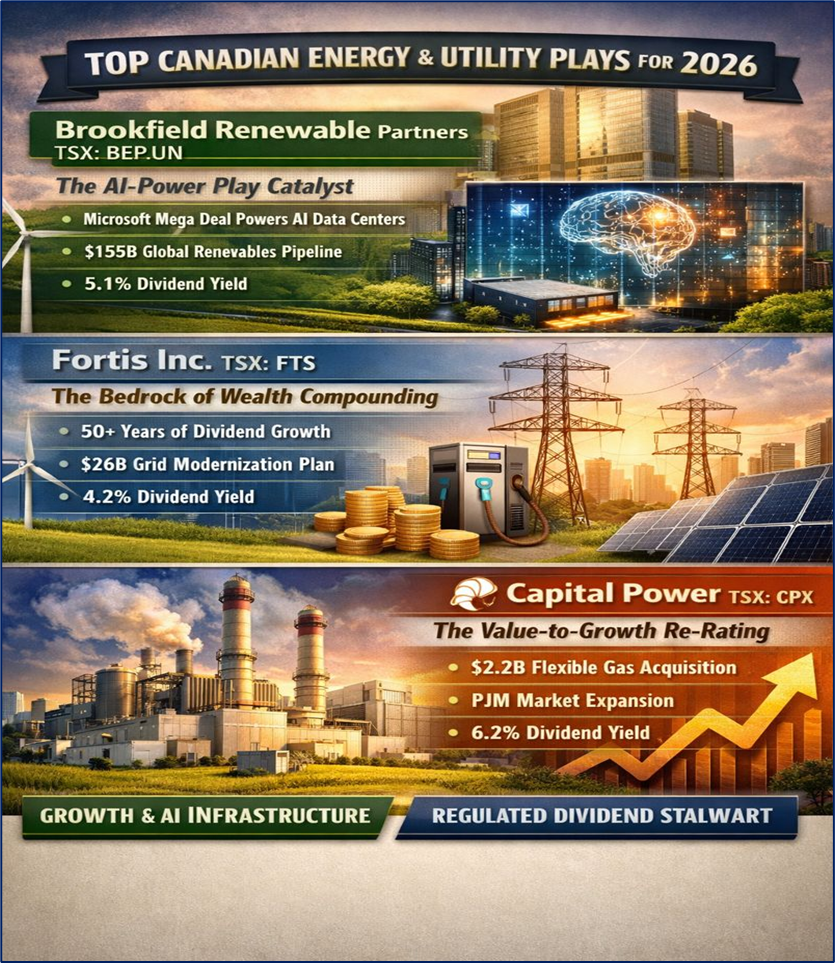

Source: Kalkine Group

1. Brookfield Renewable Partners (TSX: BEP.UN)

The AI-Power Play Catalyst

Brookfield Renewable (BEP) has transitioned from a pure-play green energy provider to a critical infrastructure partner for Big Tech. In early 2026, the company is reaping the rewards of its massive framework agreement with Microsoft—the largest of its kind—aimed at powering the next generation of AI data centers.

- Key Reasons & Drivers: BEP's competitive advantage lies in its global scale and its "first-call" status for corporations seeking carbon-free 24/7 power. The 2026 outlook is driven by the massive $10 billion AI infrastructure fund launched by its parent, Brookfield Asset Management, which funnels projects directly to BEP.

- Current Technical Analysis: As of January 2026, the stock has broken out of a multi-year consolidation pattern. It is currently trading above its 50-day and 200-day moving averages, with the RSI (Relative Strength Index) indicating healthy momentum without entering overbought territory. Analysts note a "golden cross" formed in late 2025, signaling a sustained long-term uptrend.

- Analyst Sentiment: J.P. Morgan and Scotiabank recently boosted targets, citing BEP’s "unmatched development pipeline." Hedge funds have increased positions as the company’s Green Bond issuance of C$500 million in January 2026 was oversubscribed, showing high institutional demand.

- Business Model & Financials: BEP operates a diversified portfolio of hydro, wind, solar, and storage. Its latest financial update highlights a record 155 GW development pipeline. The dividend remains a core attractant, recently increased to yield approximately 5.1%, supported by a target 5–9% annual growth.

- Valuation & Risks: While trading at a premium to peers (P/E approx. 28x), its FFO (Funds From Operations) growth justifies the multiple. Primary risks include supply chain bottlenecks for turbine components and regulatory changes in PJM (U.S. power market) regions.

The Bedrock of Wealth Compounding

Fortis is the "Gold Standard" for Canadian dividend aristocrats, having achieved over 50 consecutive years of dividend increases. In 2026, it is no longer just a "widow and orphan" stock; it is a capital appreciation play driven by the largest capital plan in its history.

- Key Reasons & Drivers: The driver for 2026 is the $26 billion five-year capital plan (2025–2029). This plan focuses heavily on grid modernization and transmission to support the electrification of everything—from EVs to industrial heat pumps.

- Current Technical Analysis: FTS is exhibiting "stair-step" growth. It recently hit a new all-time high of $72.00, supported by strong volume. Support is firmly established at the $68.00 level. Unlike more volatile growth stocks, FTS’s beta remains low, making it a favorite for "smart money" looking to hedge against broader market volatility.

- Analyst Sentiment: Royal Bank of Canada (RBC) and BMO Capital Markets have maintained "Outperform" ratings, praising the company’s visibility. "Smart money" trackers show increased inflows from pension funds seeking 7% rate base growth visibility.

- Business Model & Financials: Virtually 100% of Fortis's assets are regulated, meaning its income is essentially guaranteed by government-approved rates. The latest dividend declaration reflects a 4.2% yield, with management confirming a 4–6% annual growth target through 2029.

- Valuation & Risks: Currently undervalued according to DCF (Discounted Cash Flow) models used by firms like Simply Wall St, which estimate a fair value closer to $80.00. The primary risk is "regulatory lag"—the delay between spending money and getting permission to raise rates to cover it.

3. Capital Power Corporation (TSX: CPX)

The Value-to-Growth Re-Rating

Capital Power has traditionally been viewed as a value play, but its strategic pivot into flexible generation and the PJM market has caught the attention of global brokers like Barclays and Goldman Sachs.

- Key Reasons & Drivers: The 2026 "multibagger" thesis rests on its recent US$2.2 billion acquisition of flexible gas assets. These plants act as "batteries" for the grid, providing power when renewables drop off, a service that is becoming incredibly lucrative as the grid becomes more complex.

- Current Technical Analysis: After a 14% retreat in late 2025 due to interest rate jitters, CPX has formed a "double bottom" and is currently rebounding. It is trading at a significant discount to its 5-year average valuation multiples, presenting a classic "value-gap" opportunity.

- Analyst Sentiment: Recent upgrades from "Hold" to "Buy" by several domestic brokers highlight the company’s "accretive growth" from its PJM entry. Analysts at National Bank recently raised their price target to $76.00.

- Business Model & Financials: CPX has moved toward a "balanced" portfolio of renewables and high-efficiency natural gas. Its latest financial update showed Adjusted EBITDA growth in the mid-teens. The dividend yield is among the highest in the sector at approximately 6.2%.

- Valuation & Risks: It trades at a P/E of roughly 14x, significantly lower than BEP or FTS. The "multibagger" potential comes from a P/E rerating toward the industry average of 18x. Risks include carbon pricing volatility and the speed of the global transition away from natural gas.

Please wait processing your request...

Please wait processing your request...