Endeavour Silver’s (TSX: EDR) stock performance was robust yesterday, driven not by a new resource discovery, but by a decisive strategic move. The announcement of a definitive agreement to sell its mature Bolañitos gold-silver mine in Mexico for a consideration of up to $50 million was widely interpreted by the market as a significant de-risking and value-accretive maneuver.

On November 26, 2025, Endeavour Silver's stock on the TSX experienced a notable jump, gaining 9.79% to close at C$12.11 per share, with an intra-day high of C$12.19. This surge clearly signals market approval for the strategic shift.

- The Market Catalyst: Portfolio Rationalization and Capital Infusion

The divestiture of the Bolañitos mine to Guanajuato Silver was the key catalyst. The market responded positively because this sale achieves two major goals: portfolio simplification and a non-dilutive capital injection.

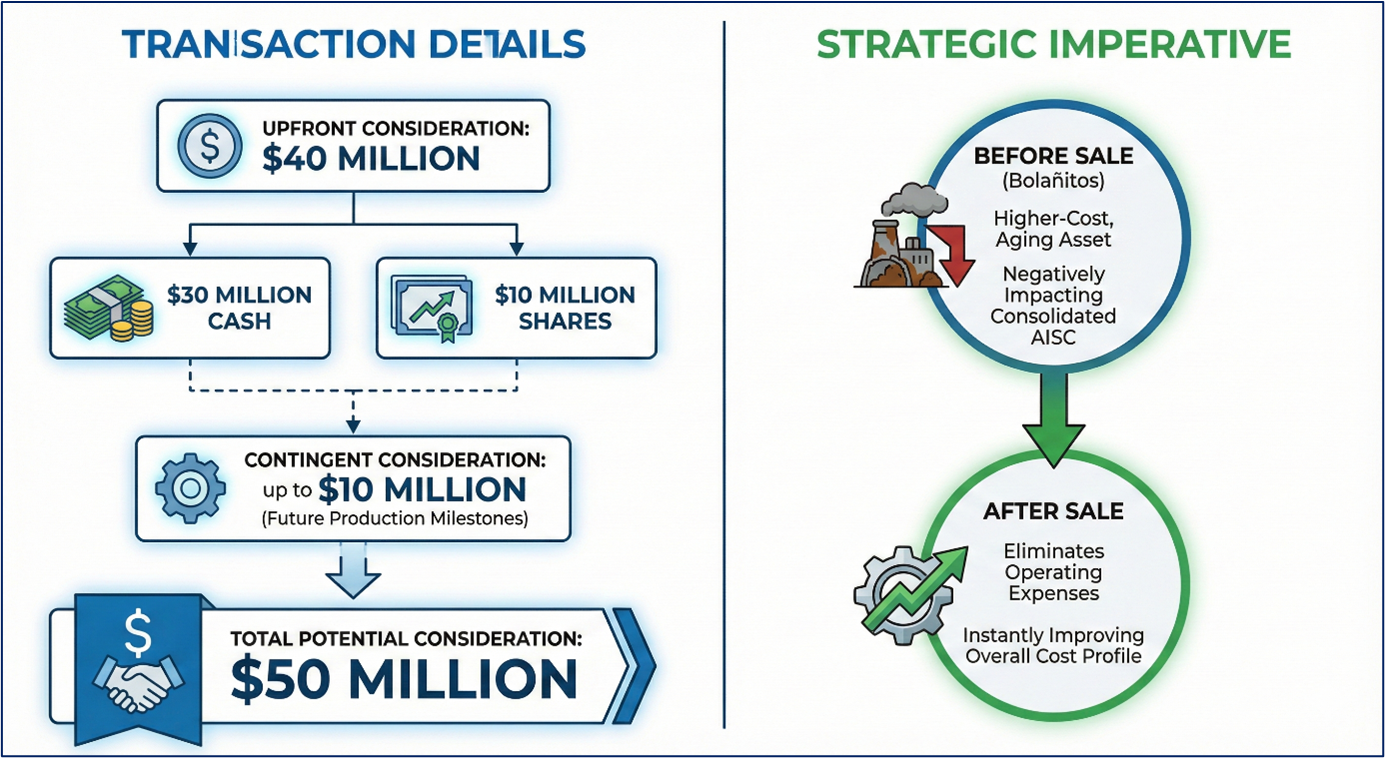

- Transaction Details: The deal secures an upfront $40 million in base consideration, composed of $30 million in cash and $10 million in shares of the acquiring company. An additional up to $10 million is contingent on future production milestones, bringing the total potential consideration to $50 million.

- Strategic Imperative: Bolañitos was a higher-cost, aging asset. The sale eliminates the associated operating expenses that were negatively impacting the consolidated All-In Sustaining Costs (AISC), thereby instantly improving the company’s overall cost profile.

Source: Kalkine Group

- Business Model: Evolving Towards a Premier Developer

Endeavour Silver is fundamentally reshaping its identity, pivoting from a multi-asset operator managing older Mexican mines to focusing on developing large-scale, low-cost cornerstone assets.

- The Transition: The divestiture signals a full commitment to focusing management expertise and capital on the Terronera development and the world-class Pitarrilla deposit.

- New Flagship (Terronera): The recent declaration of commercial production at Terronera in late 2025 is the most critical operational update. The new business model is now heavily reliant on Terronera becoming the company's low-cost, high-volume engine, projected to drastically reduce average unit costs and double silver-equivalent production.

- Operational and Financial Updates

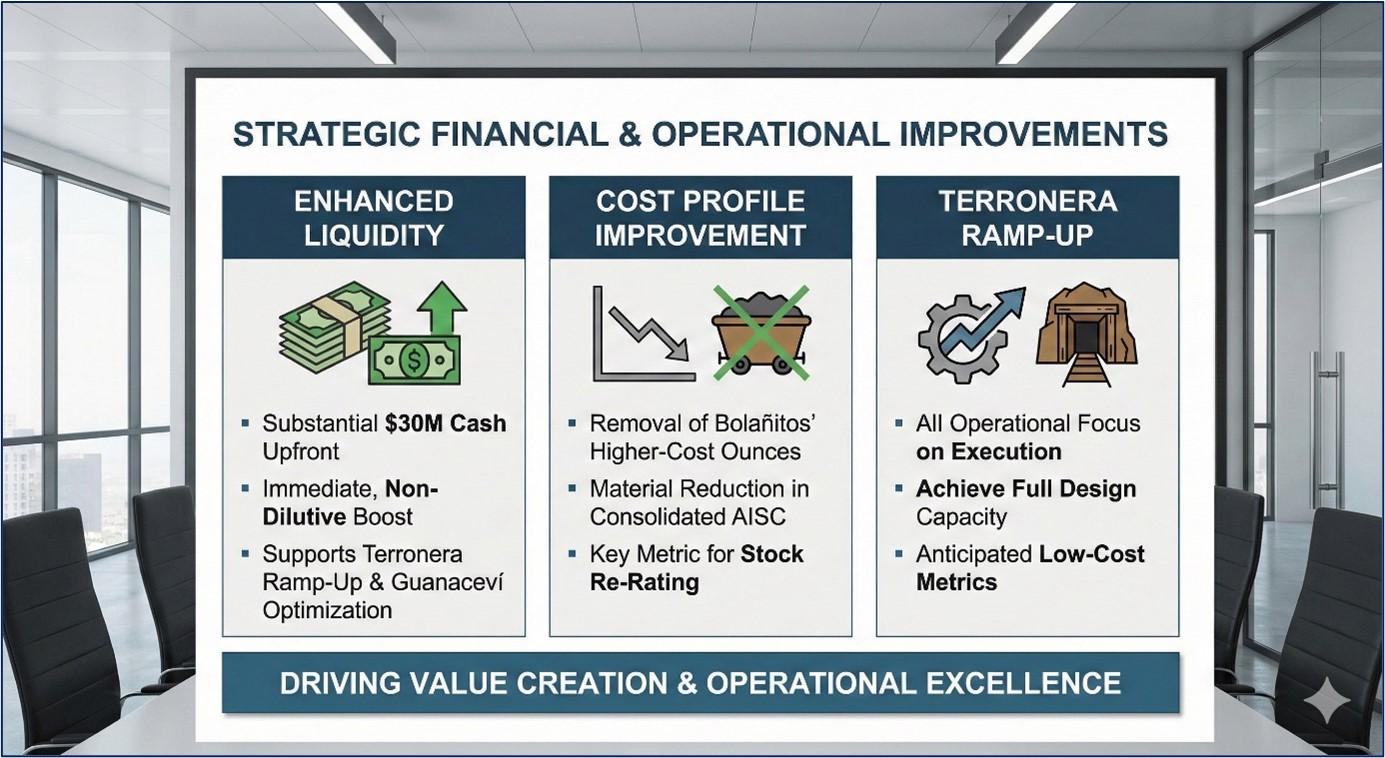

The divestiture significantly enhances Endeavour's financial position and clarifies its path to lower-cost production.

- Enhanced Liquidity: The substantial $30 million cash component of the upfront payment provides an immediate, non-dilutive boost to the balance sheet. This liquidity is essential for managing the initial ramp-up phase at Terronera and optimizing its other operating mine, Guanaceví.

- Cost Profile Improvement: The removal of Bolañitos' higher-cost ounces is expected to result in a material reduction in consolidated AISC in forthcoming quarterly reports—a key metric for re-rating the stock in the mining sector.

- Terronera Ramp-Up: All operational focus is now on executing the ramp-up at Terronera to ensure it achieves its full design capacity and anticipated low-cost metrics.

Source: Kalkine Group

- Strategic Drivers: Maximizing Margin and Focus

The market is rewarding management's strategic discipline in prioritizing profitability and growth quality over volume.

- Unit Cost Reduction: The sale directly accelerates the reduction in company-wide production costs, leading to improved operating margins, especially if silver prices remain favorable.

- De-Risking Capital: The cash infusion acts as a financial buffer, mitigating execution risks at Terronera and providing the flexibility to advance early work on Pitarrilla without immediate reliance on external, potentially dilutive, financing.

- Simplification: A streamlined portfolio with a clearer focus on two major assets (Terronera and Pitarrilla) is easier for analysts and investors to value, which often results in increased institutional interest.

- Risks and Headwinds

The newly focused portfolio introduces specific concentration risks that investors must monitor.

- Execution at Terronera: The company is now highly leveraged to the flawless execution, consistent operation, and cost-effective ramp-up of the Terronera mine. Delays or cost overruns here would have a magnified negative impact.

- Asset Concentration: Relying on a smaller number of core assets (Terronera and Guanaceví), all operating within Mexico, increases the potential impact of localized operational disruptions or adverse regional political changes.

- Commodity Price Sensitivity: Profitability remains closely tied to the inherent volatility of silver and gold prices.

Conclusion

Endeavour Silver’s surge following the Bolañitos sale is a clear indication that the market fully endorses the shift toward a high-margin, streamlined operating structure. The divestiture efficiently monetized a non-core asset, provided necessary capital, and, most importantly, provided the financial and managerial focus required to ensure the successful ramp-up of its new flagship asset, Terronera.

- Strategic Win: The sale of Bolañitos efficiently monetized a non-core asset and significantly boosted liquidity.

- Stock Surge: The market reacted by sending the TSX: EDR stock up 9.79% on the announcement.

- Cost Profile Improvement: Expect the removal of higher-cost ounces to positively impact future quarterly AISC reporting.

- Terronera Focus: All operational and capital resources are now heavily aligned to maximize the output and efficiency of the new Terronera mine.

Source: Trading View, 26 Nov 2025

Please wait processing your request...

Please wait processing your request...