Get the latest January 2026 Loblaw (TSX: L) stock analysis. Explore expert price targets, dividend updates, and forward-looking strategies for Canadian investors.

Key Takeaways for January 2026

- Current Stock Price: Loblaw (TSX: L) is trading near $62.11 CAD, maintaining strong support above its 52-week low of $43.32.

- Dividend Update: The company recently declared a quarterly dividend of $0.14 CAD with a forward yield of approximately 0.92%.

- Earnings Watch: Q4 2025 and full-year fiscal results are officially scheduled for release on February 25, 2026.

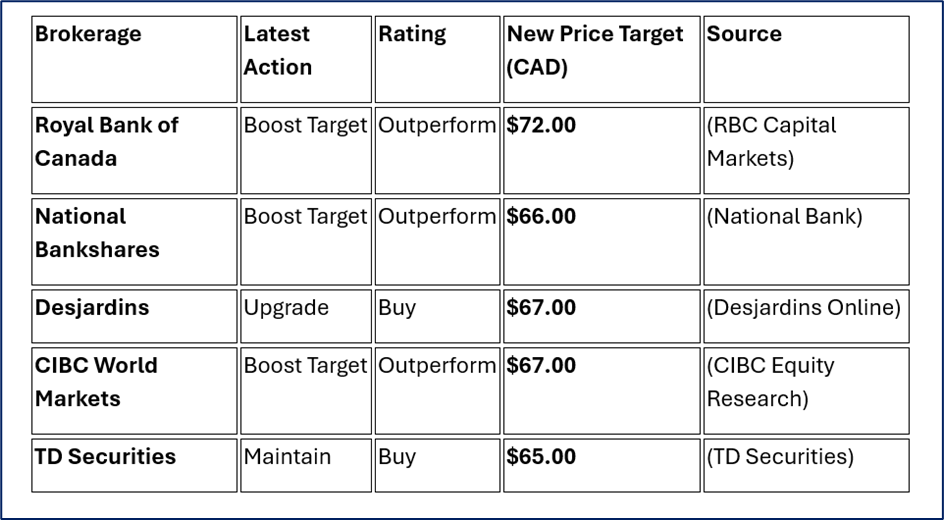

- Analyst Sentiment: Consensus remains a "Moderate Buy" with top-tier price targets reaching as high as $72.00 CAD (Royal Bank of Canada).

- Economic Backdrop: Canadian GDP growth is projected to hit 1.4% in 2026, providing a steady environment for consumer staples.

Why is Loblaw (TSX: L) Dominating the TSX Composite in January 2026?

As we navigate the opening month of 2026, Loblaw Companies Limited (TSX: L) continues to be a cornerstone for retail investors seeking defensive growth. In a volatile TSX Composite Index, which has seen significant swings due to shifting Bank of Canada interest rate expectations and fluctuating CAD/USD exchange rates, Loblaw remains a "safe haven" play. The Canadian economy is currently balancing on a fine line between cooling inflation and a softening labor market, making essential retailers like Loblaw more attractive than high-growth tech or cyclical energy stocks. With the "Buy Canadian" sentiment at an all-time high, the company’s vast footprint—from No Frills to Shoppers Drug Mart—is capturing a massive share of the consumer wallet.

Investors are flocking to TSX: L because the business model is built for resilience. Even as global market dynamics face pressure from trade uncertainties and supply chain shifts, Loblaw’s internal food inflation has historically tracked lower than the national CPI, driving increased "tonnage" and customer loyalty through its PC Optimum program. In January 2026, the stock is seeing a surge in retail interest as many anticipate a strong Q4 earnings beat. The strategic exit from certain low-margin electronics and a pivot toward high-margin Pharmacy and Healthcare Services has streamlined the balance sheet, making it a viral topic across LinkedIn and Financial Twitter (X).

Is the current Loblaw stock price a bargain or a peak? Analytical retail sentiment suggests that while the P/E ratio is sitting slightly high at 30.29x, the company’s aggressive share buyback programs and consistent dividend growth (14 consecutive years of increases) justify the premium. As the Canadian Dollar (CAD) remains sensitive to oil prices and US trade renegotiations, owning a domestic giant with essential pricing power is a logical move for 2026. This article breaks down the expert broker ratings, latest financial updates, and the forward-looking strategies you need to master your portfolio this year.

How is the 2026 Canadian Economy Impacting Your Portfolio?

What is the current state of the TSX Composite and the CAD?

The S&P/TSX Composite Index is hovering around the 32,834 mark as of late January 2026. While the broader market has struggled with a "trade shock" and tariffs affecting the industrial sector, the Consumer Staples sector remains a top performer. The Canadian economy is expected to grow by 1.4% this year, a modest but steady improvement over 2025. For investors, this means the Canadian Dollar (CAD) is stabilizing, but the Bank of Canada’s decision to likely hold rates at 2.25% through 2026 keeps the focus on "quality" companies with high free cash flow.

Industry Analysis: Why is Grocery and Pharmacy Winning?

- Food Inflation Cooling: Experts predict retail food inflation will ease to a range of 3.3% – 4.3% in 2026. This allows Loblaw to stabilize margins while continuing to offer "hard discount" value through banners like No Frills.

- Pharmacy Growth: The healthcare segment is the silent hero. With Shoppers Drug Mart expanding its clinical services and specialty drug offerings, Loblaw is no longer just a grocer; it is a healthcare provider.

- Digital Transformation: E-commerce sales grew by over 17% recently, proving that the PC Express and AI-driven personalization tools are working.

What are the Forward-Looking Strategies for Investors?

Short-Term Strategy (3-6 Months): The Earnings Play

- Action: Monitor the February 25, 2026 earnings call closely.

- Reason: Historical data shows Loblaw often beats conservative estimates. Investors should look for updates on the PC Financial acquisition and the rollout of the "Robin" AI tool for store management.

- Outlook: Bullish, provided the company maintains its "tonnage" market share growth.

Medium-Term Strategy (6-18 Months): Sector Rotation

- Action: Accumulate on dips below the $60.00 CAD support level.

- Reason: As the labor market resets and the unemployment rate edges toward 6.7%, consumers will likely trade down to private labels like No Name and President's Choice. Loblaw owns this "value" space.

- Outlook: Neutral to Bullish.

Long-Term Strategy (2+ Years): The Infrastructure & ESG Bet

- Action: Hold for compounding dividends and capital appreciation.

- Reason: Loblaw is investing over $10 billion by 2030 in its store network and a massive 1.2 million-square-foot automated distribution center. Their commitment to Net-Zero emissions by 2040 also makes them a favorite for ESG-focused institutional funds.

- Outlook: Bullish.

Is Loblaw Stock Bullish, Bearish, or Neutral?

Short-Term Personal Analysis (Bullish):

The stock is showing "catchy" momentum in January. After a slight dip in early Jan, it has recovered to the $62 range. The logic here is simple: "Fear of Missing Out" (FOMO) ahead of the fiscal year-end report. Retailers are seeing that even with trade tensions, Canadians still need to eat and buy medication.

Long-Term Personal Analysis (Bullish):

The business model is a fortress. By integrating Artificial Intelligence (AI) into supply chains and expanding Shoppers Drug Mart clinics, Loblaw is creating a high-barrier-to-entry ecosystem. While some might say the P/E is "rich," the consistent 10%+ adjusted EPS growth justifies the price.

Latest Analyst Ratings & Share Price Forecasts

The following table highlights the latest ratings from top brokers as of January 29, 2026:

Source: Market Data

Consensus View: A "Moderate Buy" with an average 12-month target of approximately $67.33 CAD, representing a potential upside of ~8% from current levels.

Investor FAQ: Everything You Need to Know

When is the next Loblaw dividend date?

The last ex-dividend date was December 15, 2025. Based on historical patterns, the next ex-dividend date is expected in mid-March 2026.

What are the key risks for TSX: L?

- Regulatory Scrutiny: Increased government pressure on grocery margins and the "Grocery Code of Conduct."

- Competition: Expansion of discount rivals like Aldi (entering 2026 with 3,200 stores globally) and Walmart Canada.

- Valuation: Trading at a P/E of 30x is significantly higher than the sector average of 22x.

Why did the stock surge in late 2025?

The announcement of the issuance of $500 Million in Senior Unsecured Notes and the strategic acquisition of PC Financial assets by EQB provided a fresh capital injection and a more focused corporate structure.

Analytical Investment Conclusion: Buy, Sell, or Hold?

Conclusion: HOLD / ACCUMULATE ON DIPS

While the stock is clearly a high-quality asset, it is currently trading near its fair value. For new investors, jumping in at $62.11 might offer limited immediate upside compared to the $72.00 ceiling set by analysts. However, for those seeking a recession-proof dividend payer with a massive competitive moat in the Canadian market, Loblaw is a "must-have" in a 2026 portfolio.

Wait for the February 25th report to see if margins are expanding. If the company shows continued success in its private-label strategy, this stock could easily break toward the $70.00 mark by spring.

Please wait processing your request...

Please wait processing your request...