As the clock struck midnight on 2025, Luca Mining Corp. (TSXV: LUCA) provided a final firework for shareholders. Closing the year with a ~3.5% gain on December 31, the stock reached CAD1.49, capping off a transformative year that saw the company rise from a penny stock to a serious mid-tier contender.

This isn't just a "Santa Claus rally." Behind the movement is a high-octane shift in the company's business model and a balance sheet that is finally breathing easy.

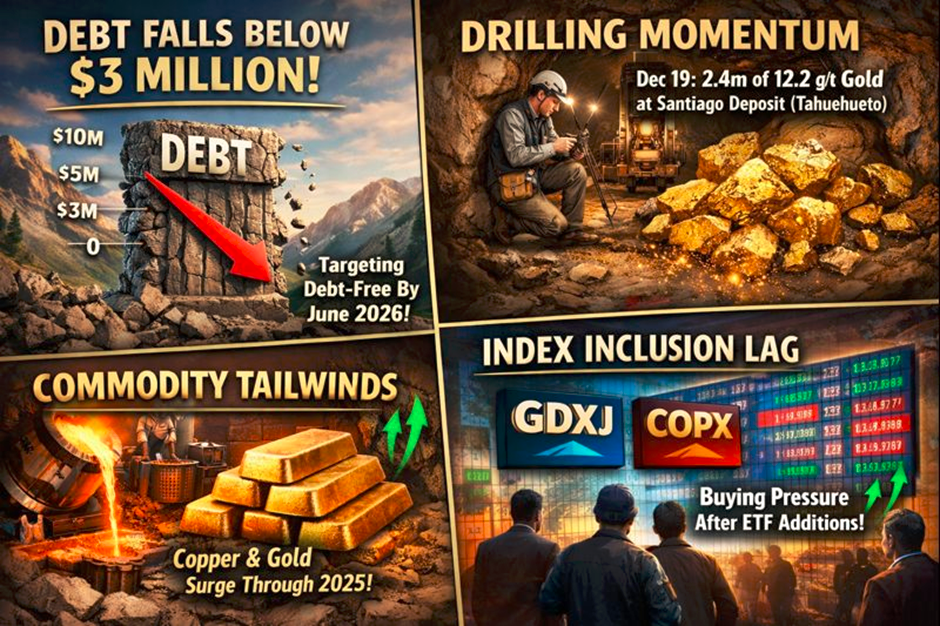

Key Reasons & Drivers: Why the End-of-Year Pop?

Source: Kalkine Group

The December 31st jump was the culmination of several weeks of positive momentum. Key drivers included:

- Year-End Debt Milestone: Management’s aggressive debt-reduction plan hit a major milestone, with total debt falling below $3 million by year-end. Investors are front-running the "Debt-Free by June 2026" narrative.

- Drilling Momentum: Just before the holidays (Dec 19), Luca reported high-grade gold intercepts at the Santiago Deposit (Tahuehueto), including 2.4 metres of 12.2 g/t Gold.

- Commodity Tailwinds: Record refined copper output and a resurgence in gold demand throughout 2025 provided a macro-economic floor for polymetallic producers.

- Index Inclusion Lag: Continued buying pressure following the company's inclusion in the GDXJ ETF and the Global X Copper Miners ETF (COPX) earlier in the year.

Latest Business Model: From Base Metal Miner to Gold Producer

Luca Mining has pivoted its strategy. Historically viewed as a zinc-heavy polymetallic miner, the "New Luca" model focuses on:

- Gold-First Optimization: At Campo Morado, the company is moving away from purely base metal concentrates. By engaging specialists like Ausenco, they aim to triple gold recoveries from 20% to over 60%.

- The "Reforma" Growth Engine: Shifting production toward high-grade zones like the Reforma deposit, which acts as a "high-grade pod" to boost cash flow.

- Path to 200k: The business model is built on scaling production from ~40,000 oz Gold Equivalent (AuEq) to a 200,000 oz AuEq annual run rate through organic expansion and mill throughput increases.

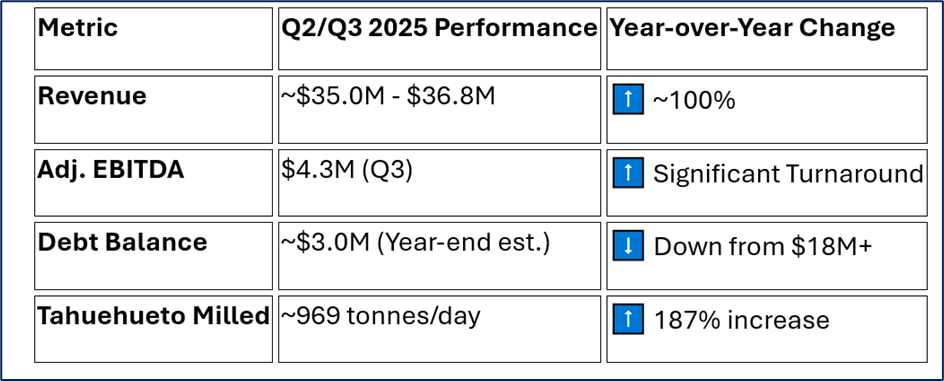

Latest Financial & Operational Updates

Source: Company Data

Operational Highlights:

- Tahuehueto (Durango): Achieved record milling rates. The installation of the copper-lead separation circuit is expected to be fully integrated in early 2026, which will significantly improve payables.

- Campo Morado (Guerrero): Reached 98.7% grinding availability, the highest in the mine's recent history.

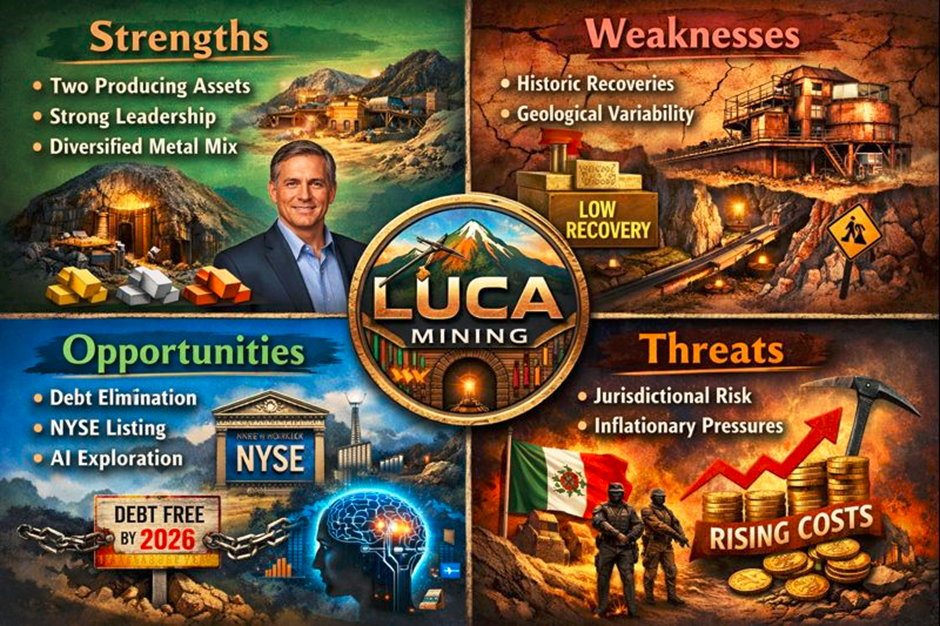

SWOT Analysis

Source: Kalkine Group

Strengths

- Two Producing Assets: Unlike many juniors, Luca has active cash flow from two distinct mines in Mexico.

- Strong Leadership: CEO Dan Barnholden has successfully cleaned up the balance sheet and regained institutional trust.

- Diversified Metal Mix: Exposure to Gold, Silver, Copper, and Zinc.

Weaknesses

- Historic Recoveries: Campo Morado still struggles with historically low gold recovery rates.

- Geological Variability: Narrow-vein mining at Tahuehueto can lead to fluctuating grades and "hiccups" in quarterly earnings.

Opportunities

- Debt Elimination: Becoming debt-free by mid-2026 removes a massive overhang on the share price.

- NYSE Listing: Management has signaled a goal to list on the New York Stock Exchange once they reach mid-tier status.

- AI Exploration: Utilizing AI to re-analyze 25 years of historical drilling data at Campo Morado to find "hidden" high-grade zones.

Threats

- Jurisdictional Risk: Operating in Mexico carries inherent risks regarding security and shifting mining regulations.

- Inflationary Pressures: Rising costs for labor and energy can squeeze the All-In Sustaining Costs (AISC), which were ~$2,276/oz earlier in 2025.

Key Risks to Watch

Investors should remain cautious about operational volatility. Turning around older, capital-starved mines is not a linear process. Any mechanical failure at the mills or a sudden drop in ore grade could lead to short-term cash burn, as seen in Q2 2025. Additionally, the company's reliance on achieving higher recoveries at Campo Morado is a "technical bet" that has yet to be fully proven at a commercial scale.

Conclusion

Luca Mining’s 3.5% climb on the final day of 2025 suggests that the market is beginning to price in the "2026 Debt-Free" catalyst. With revenues doubling year-over-year and a clear path toward 200,000 oz of production, LUCA is no longer just a penny stock gamble—it's an operational turnaround story.

Please wait processing your request...

Please wait processing your request...