Investors waking up to the TSX Venture charts on December 23rd were met with a golden surprise: Monument Mining Limited (TSXV: MMY) surged approximately 12%, capping off a month of aggressive bullish momentum. While the broader mining sector has been heating up, Monument’s sudden vertical move suggests more than just a rising tide lifting all boats.

Below is the deep-dive analysis of why this junior-turned-mid-tier producer is suddenly the talk of the retail circuit.

The "Perfect Storm": Key Drivers Behind the Dec 23rd Surge

The double-digit jump wasn't a fluke; it was the culmination of three major catalysts hitting the tape simultaneously:

Source: Kalkine Group

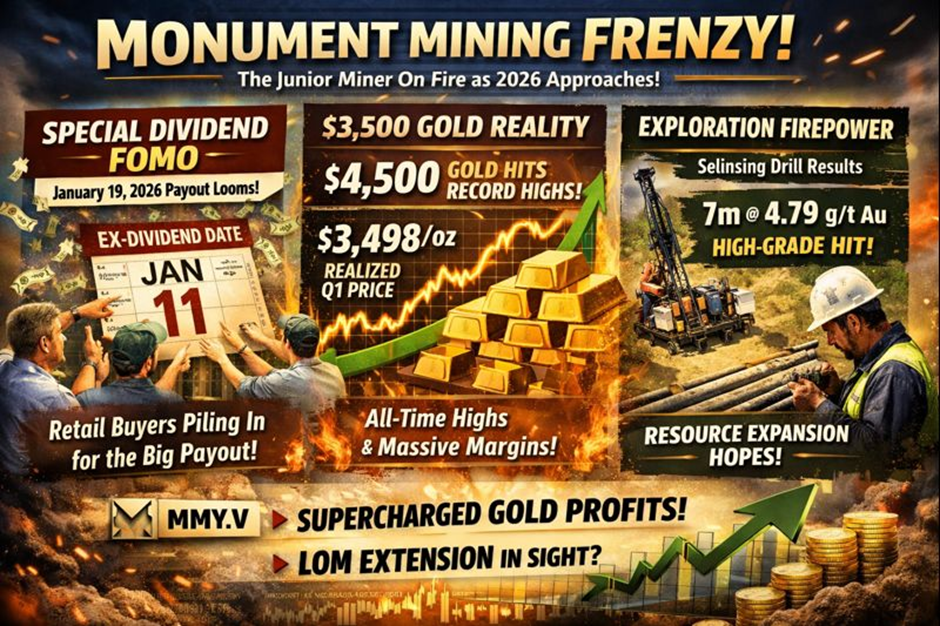

- The "Special Dividend" FOMO: On December 11, Monument announced a Special Cash Dividend payable on January 19, 2026. As the "ex-dividend" date approaches, retail buyers are piling in to capture the yield, a rarity in the junior mining space.

- The $3,500 Gold Reality: In its latest Q1 2026 report (released Dec 1), Monument revealed a record average realized gold price of $3,498/oz. With gold prices testing all-time highs in late December at $4,500/oz, the market is finally re-rating MMY's massive gross margins.

- Exploration Firepower: The "First 16 Drill Hole" results from the Selinsing expansion (Dec 3) showed high-grade hits like 7m @ 4.79g/t Au. Investors are betting that the upcoming Resource Statement (slated for mid-2026) will significantly extend the Life of Mine (LOM).

Latest Business Model: From Exploration to Cash Machine

Monument has successfully pivoted from a speculative explorer to a disciplined producer.

- Self-Funded Growth: Unlike many peers who dilute shareholders to keep the lights on, Monument is using its $62.84M cash pile to fund its own exploration.

- Dual-Jurisdiction Play: * Malaysia (Selinsing): The "Cash Cow." A fully operational sulphide flotation plant churning out consistent ounces.

- Western Australia (Murchison): The "Growth Engine." Currently undergoing economic assessments to restart production at the Burnakura Mill.

- The "Filter Press" Alpha: Recent technical upgrades, including a new filter press, have removed processing bottlenecks, allowing the company to process more ore at lower costs.

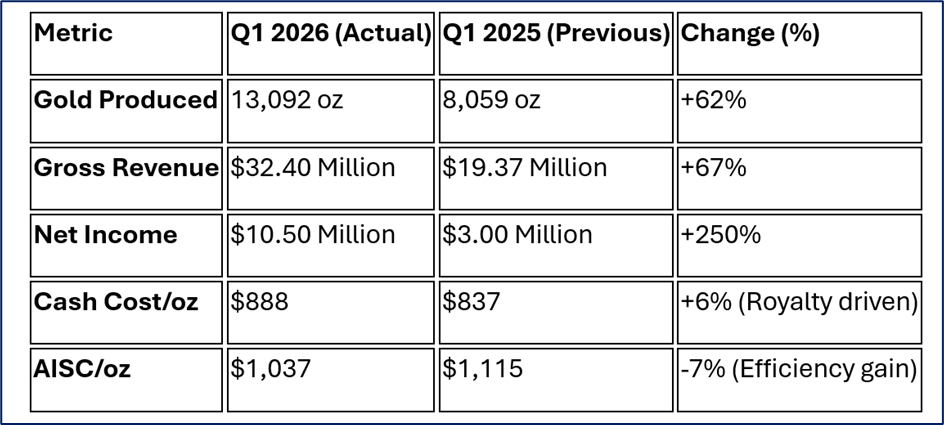

Financial & Operational Snapshot (Q1 Fiscal 2026)

The numbers released in December explain the stock's sudden magnetism:

Source: Company Data

Note: The company’s working capital has swelled to $69.55 million, providing a massive safety net for 2026 operations.

SWOT Analysis: The Analytical Lens

Source: Kalkine Group

Strengths

- Zero Debt: One of the cleanest balance sheets in the TSXV materials sector.

- High Margins: With AISC at ~$1,037 and gold at $3,500, the profit spread is nearly $2,500/oz.

- Experienced Management: Proven track record of building and operating mines in SE Asia.

Weaknesses

- Share Dilution History: While minimized lately, a 5.1% increase in shares over the last year has slightly capped EPS growth.

- Single-Asset Reliance: Most current cash flow depends on the Selinsing Mine in Malaysia.

Opportunities

- Murchison Restart: Bringing the Western Australian project into production could double the company's output.

- Resource Expansion: Current drilling at Buffalo Reef could turn a "small" mine into a large-scale open pit.

- M&A Target: Given its cash and production, MMY is a prime acquisition target for larger miners looking for "bolt-on" cash flow.

Threats

- Geopolitical Risk: Operations in Malaysia are subject to changing local mining laws and royalty structures.

- Gold Volatility: A sudden drop in gold prices would hit the "Special Dividend" narrative hard.

- Technical Risks: Sulphide ore processing is complex; any plant downtime would immediately impact quarterly targets.

Key Risks to Watch

Investors shouldn't ignore the "volatility" tag. Simply Wall St recently noted that MMY’s weekly volatility has increased from 10% to 16% over the past year. Furthermore, the 52-week range ($0.28 – $1.20) shows that while the trend is up, the pullbacks can be aggressive. The "Special Dividend" may lead to a "sell the news" event once the payment is processed in late January.

Conclusion

Monument Mining is no longer a "penny stock" story; it is a fundamental-driven growth play. The 12% surge on December 23 reflects a market that is finally pricing in record-high gold prices and the company’s transition into a dividend-paying producer. If the Murchison project in Australia gets the green light in 2026, the current $1.16–$1.20 price level may just be the new baseline.

Source: Trading View, 23 December 2025

Please wait processing your request...

Please wait processing your request...