Core Principles: Defining Retail Investment Objectives

A sound investment strategy for retail clients in Canada begins with a clear understanding of their objectives, which often revolve around time horizon and liquidity needs.

- Capital Preservation: Clients primarily seeking to protect their principal and maintain purchasing power against inflation. Common objectives include emergency funds or short-term savings (e.g., a down payment in 1-3 years).

- Income Generation: Clients needing a steady cash flow from their investments, often retirees or those supplementing regular income. Objectives include retirement distributions or fixed expenses.

- Capital Appreciation/Growth: Clients focused on maximizing the long-term value of their portfolio, typically those with long time horizons (e.g., young savers, education savings for a child).

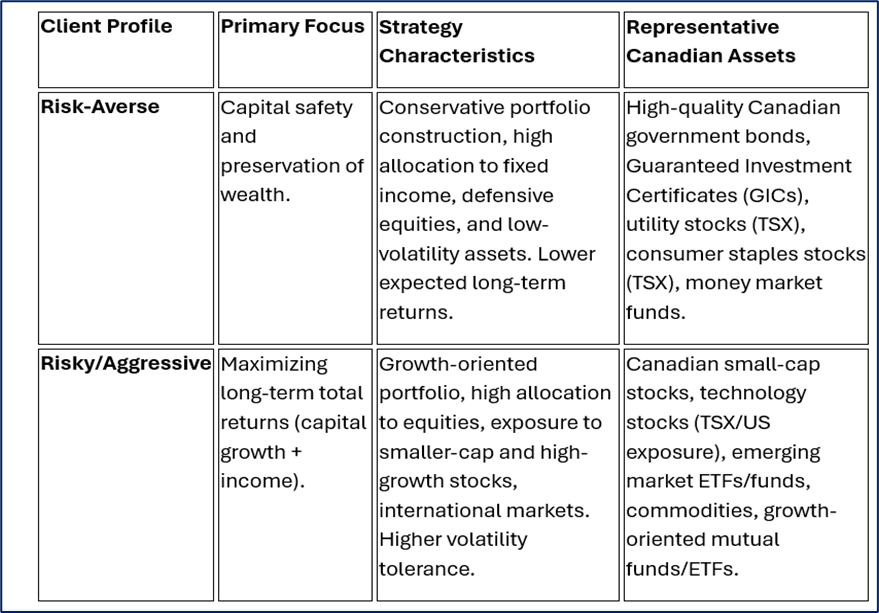

Risk Profiling: Strategies for Risky vs. Risk-Averse Clients

Risk assessment is a critical first step, combining the client's risk tolerance (emotional comfort with volatility) and risk capacity (objective ability to absorb losses without jeopardizing goals).

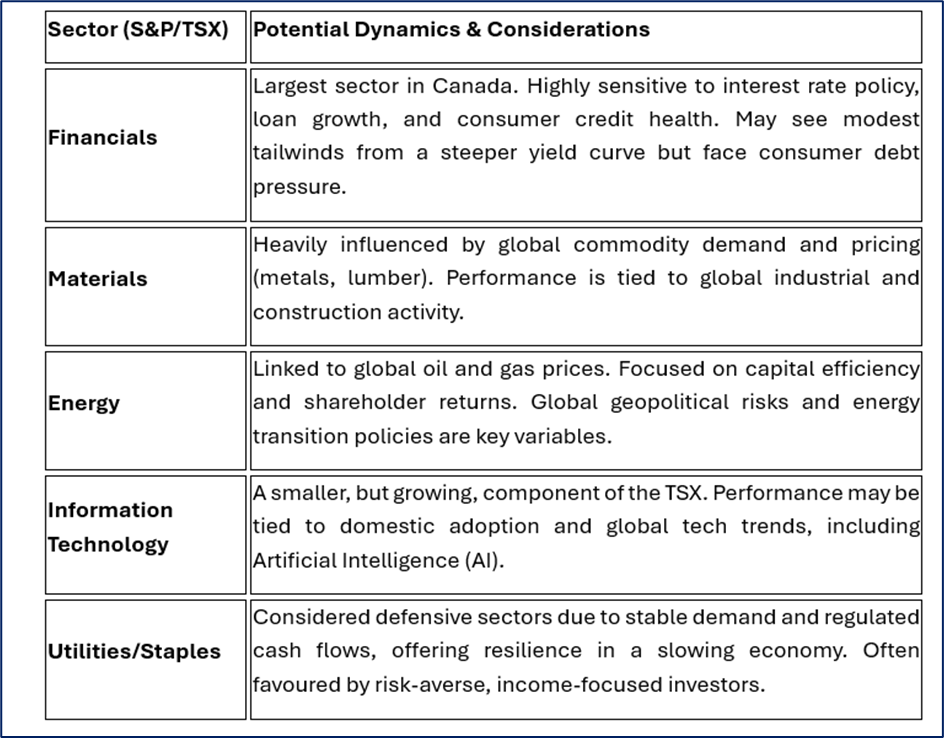

Source: Kalkine Group

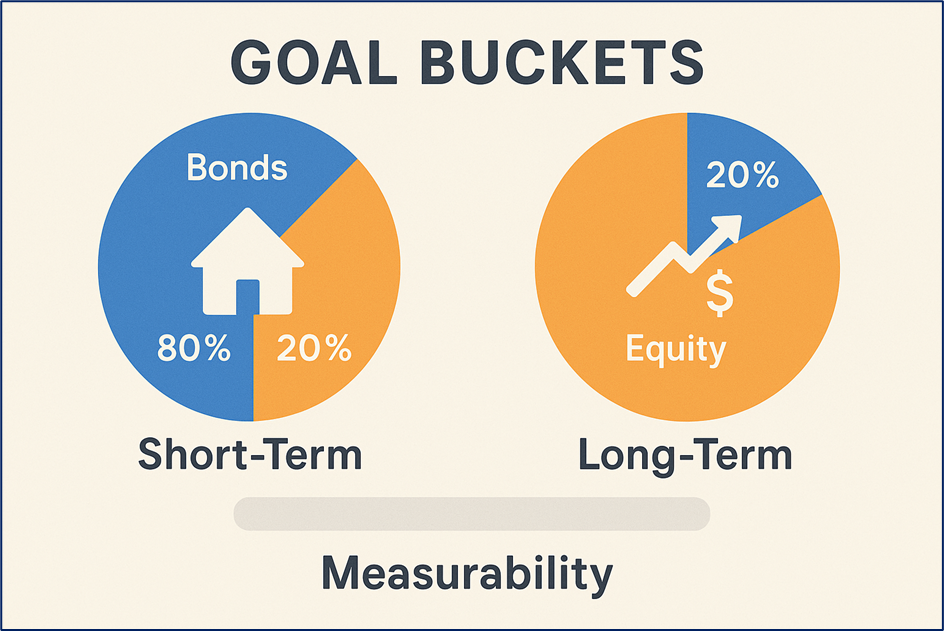

Goal-Based Investing (GBI): Structuring the Portfolio

GBI moves beyond a single portfolio risk profile by connecting specific investments to specific financial goals, each with its own time horizon and required return.

- Goal Buckets: The portfolio is segmented into "buckets" (e.g., Short-Term for a house down payment, Long-Term for retirement).

- Asset Allocation Alignment: The allocation for each bucket is customized. A short-term goal (3 years) would use a conservative allocation (e.g., 80% bonds/cash, 20% equity), while a long-term goal (25 years) would be more aggressive (e.g., 80% equity, 20% bonds).

- Measurability: Progress is tracked relative to the goal rather than simply beating a benchmark, which helps maintain discipline and reduce emotional decision-making.

Source: Kalkine Group

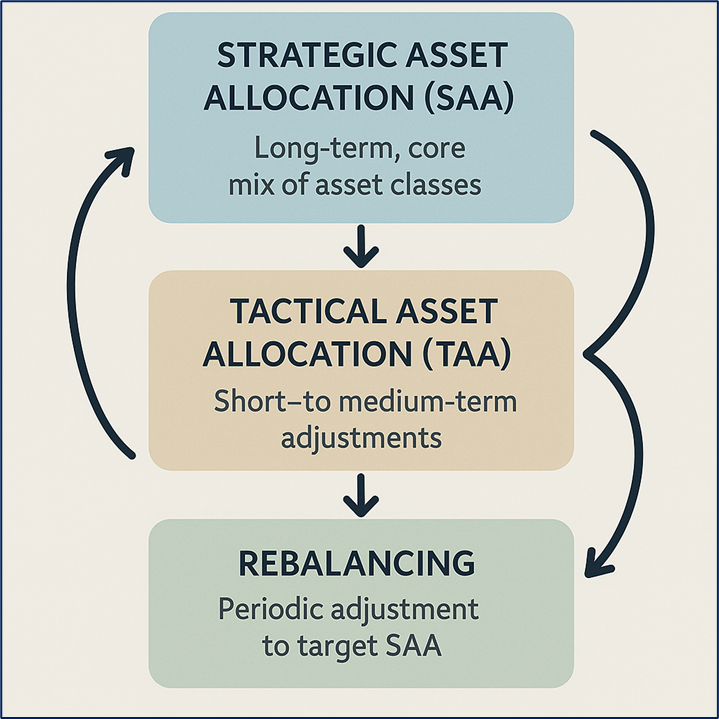

Portfolio Optimization and Management Techniques

Portfolio Optimisation

Modern Portfolio Theory (MPT) suggests constructing a portfolio that maximizes expected return for a given level of risk or minimizes risk for a target expected return. Retail portfolio management often uses simplified approaches:

- Strategic Asset Allocation (SAA): The long-term, core mix of asset classes (stocks, bonds, cash, real estate) based on the client's risk profile and time horizon. This forms the foundation of the portfolio.

- Tactical Asset Allocation (TAA): Short- to medium-term, temporary adjustments to the SAA based on current market views (e.g., slightly overweighting a sector expected to perform well). These shifts are typically modest to avoid excessive risk.

- Rebalancing: The disciplined process of periodically selling assets that have grown (and become overweight) and buying assets that have lagged (and become underweight) to restore the target SAA. This systematically enforces a "sell high, buy low" approach and maintains the desired risk level.

Source: Kalkine Group

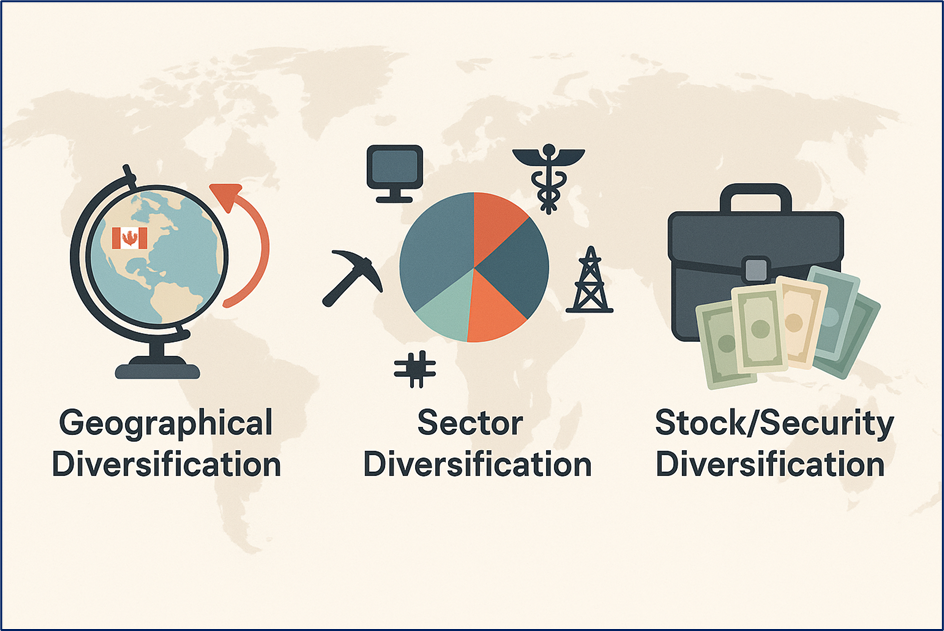

Diversification: Mitigating Unsystematic Risk

Diversification is crucial in Canada, where the benchmark S&P/TSX Composite Index is heavily weighted toward Financials and Energy.

- Geographical Diversification: Reducing "home-country bias" by investing outside of Canada. This is vital for sector diversification, as Canadian markets have limited representation in certain global sectors (e.g., technology, healthcare).

- Opportunity: Exposure to faster-growing foreign markets or sectors not prominent in Canada.

- Consideration: Currency risk and foreign withholding taxes.

- Sector Diversification: Spreading investments across different industries (e.g., Technology, Healthcare, Materials, Utilities) whose performance drivers are not perfectly correlated.

- Stock/Security Diversification: Holding a sufficient number of individual securities (typically 20-30 across multiple sectors) or using diversified funds (ETFs/mutual funds) to minimize the impact of poor performance from a single company.

Source: Kalkine Group

"Smart Money" Strategies for Retail Investors

Portfolio managers often translate complex institutional strategies into accessible retail products:

- Factor-Based Investing (Smart Beta): Investing in funds that target specific drivers of long-term returns (factors) such as Value, Momentum, Quality (strong balance sheets, stable earnings), and Low Volatility.

- Active vs. Passive Management:

- Passive (ETFs/Index Funds): Low-cost funds tracking a benchmark (e.g., S&P/TSX 60). Suitable for long-term core holdings.

- Active (Managed Mutual Funds): Funds attempting to outperform a benchmark through stock picking or market timing. May involve higher fees. A blend is common.

2026 Outlook and Potential Market Considerations

The outlook for 2026 for the Canadian market is influenced by global economic conditions, domestic fiscal policy, and sector-specific dynamics.

- Economic Context: Expectations may include moderating, albeit below-average, economic growth, a softening labour market, and potentially continued consumer caution. The Bank of Canada (BoC) policy and its impact on interest rates will remain a primary driver.

- Investment Opportunity Considerations:

- Quality/Defensive Stocks: With economic uncertainty persisting, a focus on companies with strong balance sheets, stable cash flows, and sustainable-to-growing earnings may be a preference.

- Fixed Income: A potentially steepening yield curve in Canada could improve the risk/reward profile for taking on longer-term government bond duration, but caution remains around credit spreads for corporate bonds.

- Value-Seeking Consumer Trends: Continued caution among consumers may favour value-oriented retail and essential-service businesses.

Source: Kalkine Group

Conclusion

Effective retail portfolio management is a disciplined, client-centric process that anchors investment decisions to specific, quantified goals. In the Canadian context, managing portfolio concentration risk, particularly in Financials and Energy, through strategic global and sector diversification is paramount. The path toward 2026 requires a continued analytical focus on company quality, disciplined rebalancing, and careful alignment of portfolio structure with evolving domestic economic conditions and individual risk capacity.

Please wait processing your request...

Please wait processing your request...