Executive Summary: Why the sudden pop on New Year's Eve?

NervGen Pharma (TSXV: NGEN) closed 2025 with a dramatic ~11% surge, acting as a "delayed fuse" detonation following a transformative Q4. While December 31 is typically a quiet trading day, this move was likely driven by Year-End Window Dressing (funds adding high-performers to their books before the year closes) and the market pricing in the imminent NASDAQ up-listing signaled by their recent SEC filings.

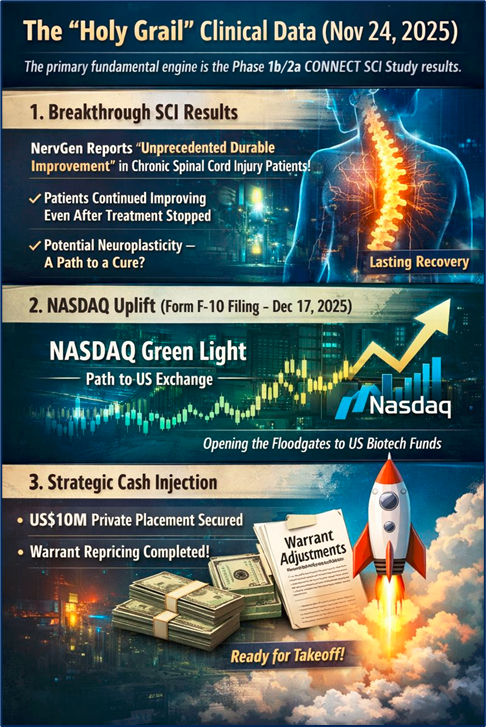

The stock is no longer trading just on "hope"—it is trading on "unprecedented" clinical data released in late November.

The 3 Key Drivers of the Rally

Source: Kalkine Group

- The "Holy Grail" Clinical Data (Nov 24, 2025) The primary fundamental engine is the Phase 1b/2a CONNECT SCI Study results.

- The News: NervGen reported "unprecedented durable improvement" in chronic spinal cord injury (SCI) patients.

- The Impact: Patients didn't just improve; they kept improving 4 weeks after treatment stopped. This suggests the drug (NVG-291) isn't just masking symptoms but potentially remodeling the nervous system (neuroplasticity).

- Why it matters now: The market took a few weeks to fully digest the "durable" aspect of this data. This is the difference between a "treatment" and a "cure" narrative.

- The NASDAQ Uplift (Form F-10 Filing – Dec 17, 2025) Just two weeks prior to the surge, NervGen filed a Form F-10 with the US SEC.

- Translation: This is the administrative "green light" application to list on a major US exchange (NASDAQ).

- The Driver: TSXV stocks are often invisible to big US institutional investors. A NASDAQ listing opens the floodgates to US biotech funds. The 11% jump likely represents "front-running" investors buying before the official NASDAQ bell rings in early 2026.

- Strategic Cash Injection & Valuation Reset

- Funding Secured: Closed a US$10M private placement in November to fund the listing and trials.

- Warrant Repricing (Dec 12): The company cleaned up its capital structure by amending warrant terms to align with Canadian currency. While technical, this is a classic "housekeeping" move before a major corporate graduation (like an uplisting), signaling to sophisticated traders that management is clearing the runway.

SWOT Analysis

Source: Kalkine Group

Strengths (Internal Power)

- First-in-Class Asset: NVG-291 is a PTPσ inhibitor, a novel mechanism with no direct approved competitors for neural repair.

- Durable Efficacy: Clinical data proves the drug works after dosing stops, a massive competitive moat.

- Fast Track Designation: FDA status accelerates the review process, crucial for burning less cash.

Weaknesses (Internal Gaps)

- Single-Asset Reliance: The company is heavily dependent on NVG-291. If it fails in Phase 3, the company value collapses.

- Cash Burn: High operational costs ($4.4M R&D spend in Q3 alone) mean they are constantly racing against their bank balance.

- No Commercial Revenue: Purely speculative valuation based on future cash flows.

Opportunities (External Growth)

- NASDAQ Liquidity: Up-listing will drastically increase trading volume and analyst coverage.

- Indication Expansion: Mechanism applies to Alzheimer’s, MS, and Stroke—markets 100x larger than SCI.

- Big Pharma Buyout: Positive Phase 2 data makes NGEN a prime acquisition target for giants like Biogen or Novartis who are starving for neuro assets.

Threats (External Risks)

- Regulatory delays: The FDA could demand larger, longer Phase 3 trials, draining resources.

- Macro-Economics: A high-interest-rate environment hurts pre-revenue biotech disproportionately (capital is expensive).

- Short Seller Attacks: As the stock rises, it becomes a target for volatility and "sell the news" campaigns.

Latest Business Model & Financial Health

Business Model: NervGen operates as a lean clinical-stage biotech. They do not manufacture or sell drugs yet. Their model is:

- Develop: Advance NVG-291 through FDA trials.

- De-risk: Prove efficacy in humans (accomplished Nov 2025).

- Monetize: Either commercialize alone (high cost) or, more likely, partner/license the drug to a major pharma player for upfront cash + royalties.

Operational Updates (Q3/Q4 2025):

- Cash on Hand: ~$11.4M (Sept 30) + ~$10M (Nov Raise) = ~$21M estimated liquidity entering 2026.

- Burn Rate: Approx. $1.5M - $2M per month.

- Runway: The recent raise extends their runway through the critical NASDAQ transition, likely into mid-2026.

- Leadership: Strengthened clinical team in July 2025 to prepare for Phase 3 design.

Risks: The "Widow-Maker" Factors

- Dilution Risk: Despite the recent raise, Phase 3 trials cost $50M+. Expect more stock offerings (dilution) in 2026.

- The "Placebo" Trap: Neuro trials are notorious for high placebo responses. Even if patients improve, if the placebo group also improves, the trial fails.

- Liquidity Trap: Until the NASDAQ listing is live, selling large positions on the TSXV can crash the stock price due to low volume.

Conclusion

The 11% rise on December 31, 2025, was not a random fluctuation; it was a rational repricing of risk. The market has moved NervGen from the "speculative science" bucket to the "proven mechanism" bucket following the November data. Combined with the friction-clearing F-10 filing, the stock is being accumulated by investors anticipating a "NASDAQ Pop" in Q1 2026.

Verdict: The science appears real, the pathway is clear, but the volatility will be violent.

Please wait processing your request...

Please wait processing your request...