NFI Group Inc. (TSX: NFI) is turning heads on Bay Street today, December 18, 2025, with shares surging approximately 6%. After a rollercoaster year marked by supply chain hurdles and a massive battery recall, the "bus of the future" manufacturer is finally hitting its stride.

If you've been watching the EV and transit space, today’s move is a massive signal that the market is re-rating NFI's massive $13 billion backlog and its aggressive leadership pivot.

Key Drivers: Why NFI is Surging Today

The ~6% rally on December 18 is fueled by a "perfect storm" of positive news that has significantly de-risked the stock for retail and institutional investors alike.

Source: Kalkine Group

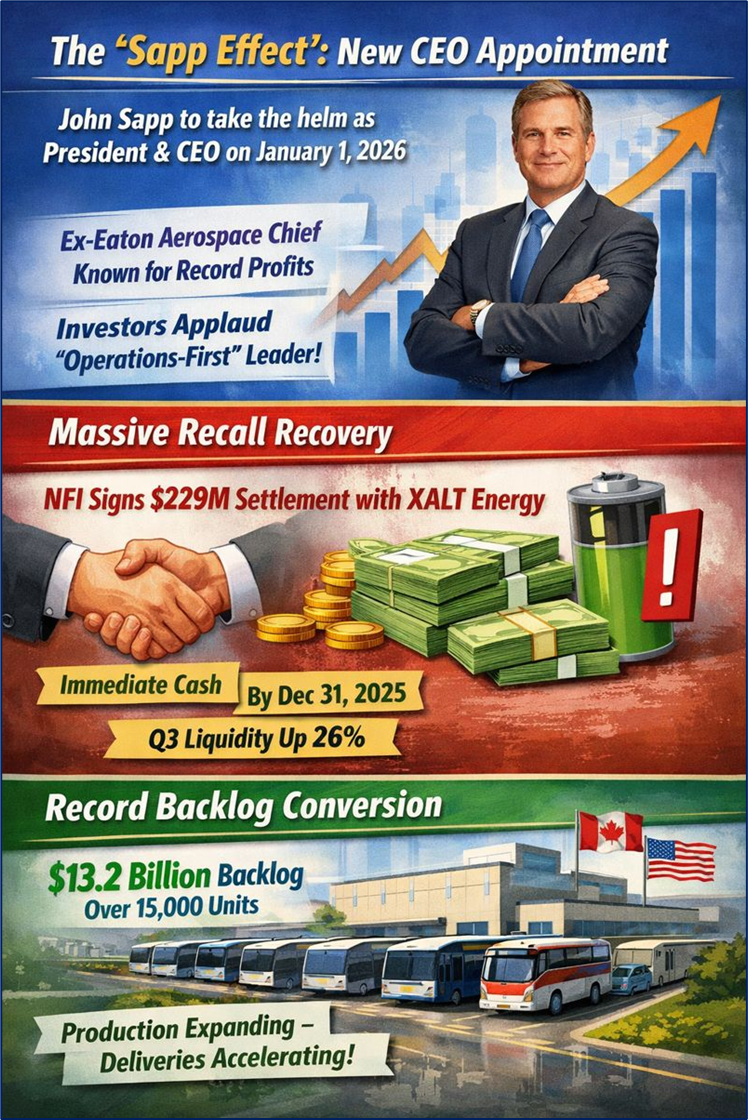

1. The "Sapp Effect": New CEO Appointment

NFI announced that John Sapp will take the helm as President and CEO on January 1, 2026. Sapp is a heavy hitter from Eaton Corporation’s Aerospace division, where he delivered record profits. Investors are cheering this "operations-first" leader who is expected to convert NFI’s massive order book into actual bottom-line cash.

2. Massive Recall Recovery

Earlier this week, NFI signed a Master Settlement Agreement (MSA) with XALT Energy. This is huge: NFI expects to recover 75%–80% of the $229 million battery recall provision.

- Immediate Cash: A significant payment is due by December 31, 2025.

- Liquidity Boost: This settlement is expected to increase NFI’s Q3 liquidity by roughly 26%.

3. Record Backlog Conversion

The market is finally pricing in the $13.2 billion backlog (over 15,000 equivalent units). With seat supply issues resolving and production expanding in Canada to free up U.S. capacity, NFI is moving from "ordering" phase to "delivering" phase.

SWOT Analysis

Source: Kalkine Group

Business Model & Updates

NFI Group operates as a global leader in bus and coach manufacturing. Their business model is a "razor and blade" strategy:

- Manufacturing: Selling complex, high-value buses (New Flyer, MCI, Alexander Dennis).

- Aftermarket: Providing parts and service for the life of the vehicle (12–15 years), which generates high-margin recurring revenue.

Latest Business Updates:

- Production Ramp: NFI is aiming to return to pre-pandemic production volumes by the end of 2025.

- Zero-Emission Focus: ZEBs (Zero-Emission Buses) now make up over 35% of the total backlog.

- Financial Health: Adjusted EBITDA for Q4 2025 is guided at $105M - $125M, signaling a strong finish to the year.

The Risks: What to Watch

While the stock is up, NFI isn't without its "potholes":

- Execution Risk: Ramping production while simultaneously managing a 24-month battery recall campaign is a logistical nightmare.

- Interest Rates: As a capital-intensive business with high debt, NFI remains sensitive to the cost of borrowing.

- Supplier Concentration: Reliance on specific battery cell technologies can create bottlenecks if a single supplier fails.

Conclusion

The 6% jump on December 18 reflects a "clearing of the air." By settling the battery recall and bringing in an aerospace-grade CEO, NFI Group has signaled to the TSX that its darkest days are likely behind it. For retail investors, the story is no longer about if they have orders—it's about how quickly and profitably they can fill them.

Source: Trading View, 18 December 2025, 10:15 AM, ON, Canada

Please wait processing your request...

Please wait processing your request...