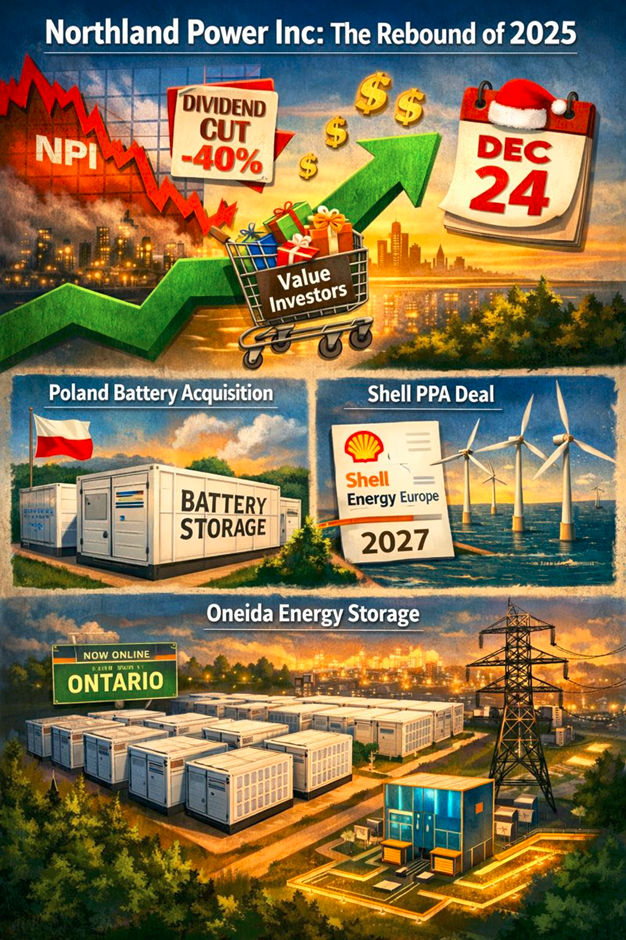

Northland Power Inc. (TSX: NPI) closed trading on December 24, 2025, up approximately 1.53% to CAD 17.91. While a single-day gain might seem modest, in the context of NPI’s turbulent Q4, this green candle signals something deeper. After a bruising November that saw a dividend slash and significant earnings miss, investors are starting to ask: Is the bottom finally in?

Here is your analytical deep dive into what drove the price action on Christmas Eve 2025, the state of the business, and whether this utility giant is a value trap or a turnaround king.

Why the Green Candle? Key Drivers of the Dec 24 Move

The 1.53% uptick wasn't driven by a single explosive press release on the 24th, but rather a confluence of stabilization factors and "bargain hunting" following the November capitulation.

Source: Kalkine Group

- The "Oversold" Bounce

Following the November 14, 2025 shock—where NPI cut its dividend by ~40% (to $0.72 annually) and reported a massive net loss—the stock plummeted ~24%. By late December, the "weak hands" had largely exited. The Christmas Eve buying pressure likely came from value-oriented retail and institutional investors spotting a disconnected entry point relative to the company's long-term asset value.

- Strategic "Wins" in December

Despite the financial noise, Northland kept executing operationally in December 2025:

- Poland Battery Acquisition: In late November/early December, NPI announced the acquisition of 300 MW of battery storage in Poland. This reassured the market that growth hasn't stalled—it’s just pivoting.

- Shell PPA Deal: A subsidiary (Nordsee One) inked a 5-year Power Purchase Agreement (PPA) with Shell Energy Europe, securing revenue visibility starting in 2027. This reminded the market that NPI’s core assets are still cash cows.

- Oneida Storage Success

The massive Oneida Energy Storage project in Ontario (commissioned earlier in 2025) is now fully contributing to the grid. Investors are pricing in the stability of this new revenue stream, which offsets some of the volatility from offshore wind.

2025 Business Model: The "Reset" Strategy

Northland Power is no longer the "growth at all costs" darling of 2021. The 2025 business model has shifted toward Profitability & Resilience.

- Regional Hubs: NPI has restructured into two main operational hubs: Americas and International. This cuts administrative bloat and streamlines decision-making.

- Technology Mix:

- Offshore Wind (The Core): Remains the heavyweight (Gemini, Nordsee One, Deutsche Bucht).

- Battery Storage (The New Growth Engine): Aggressive expansion in Poland and Canada to smooth out renewable intermittency.

- Onshore Renewables: Continued steady cash flow from solar/wind in North America.

- Revenue Security: The model relies heavily on long-term, indexed PPAs (inflation-protected) to shield against market volatility.

Financial & Operational Reality Check (Q3/Q4 2025 Context)

To understand the stock price, you must look at the financials that terrified the market just weeks ago.

- Revenue: $554 Million (Up 13% YoY). The top line is actually growing, driven by higher wind resources and the Oneida project.

- Net Loss: $456 Million. This was the ugly part. It was driven by a massive non-cash impairment ($527M) on the Nordsee One asset. Key Takeaway: The business isn't bleeding cash operationally; the loss was an accounting write-down.

- Adjusted EBITDA: $257 Million (Up 13%). This is the metric that matters for debt servicing, and it is healthy.

- The Dividend Cut: Slashed from $1.20 to $0.72/share. While painful, this frees up roughly $125M annually to fund the massive Hai Long and Baltic Power projects without diluting shareholders with new equity.

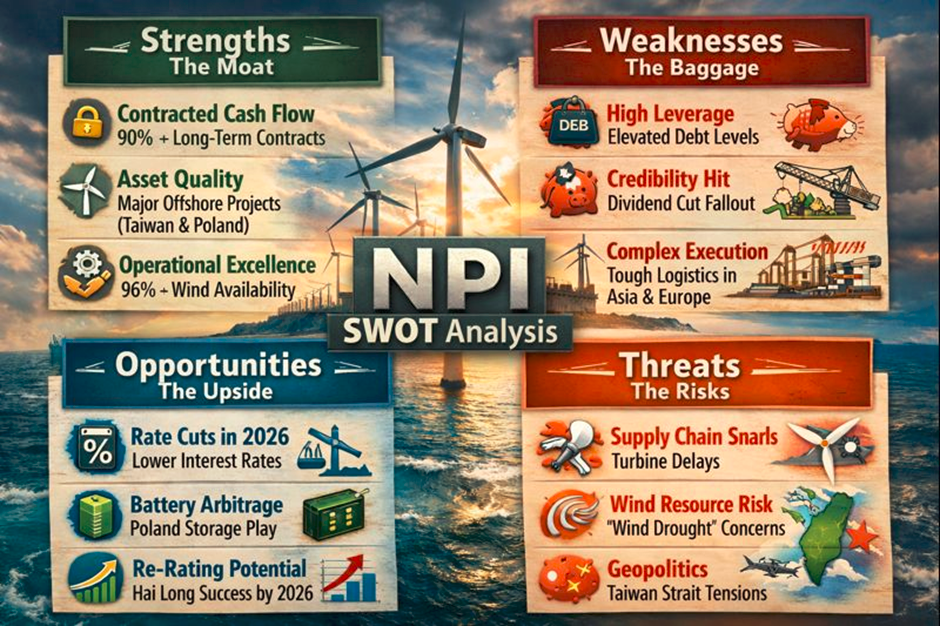

SWOT Analysis: The Bull vs. Bear Case

Source: Kalkine Group

Strengths (The Moat)

- Contracted Cash Flow: 90%+ of revenue is locked into long-term contracts with credit-worthy counterparties.

- Asset Quality: New projects (Hai Long in Taiwan, Baltic Power in Poland) are some of the largest global offshore wind assets.

- Operational Excellence: Wind availability remains high (>96%), proving they know how to run these complex machines.

Weaknesses (The Baggage)

- High Leverage: Debt levels remain elevated, making the company sensitive to interest rates (even with expected rate cuts).

- Credibility Hit: The dividend cut blindsided many retail investors, damaging trust in management’s forward guidance.

- Complex Execution: Building offshore wind in Taiwan and Poland is logistically and geopolitically harder than building a solar farm in Ontario.

Opportunities (The Upside)

- Rate Cuts in 2026: As central banks ease rates, capital-intensive utilities like NPI usually outperform.

- Battery Arbitrage: The Poland storage acquisition positions NPI to profit from Europe's volatile energy prices.

- Re-rating: If execution on Hai Long stays on track (completion 2026/27), the stock could re-rate from "distressed" to "growth."

Threats (The Risks)

- Supply Chain Snarls: Any delay in turbine delivery for Hai Long or Baltic Power burns cash and delays revenue.

- Wind Resource Risk: Q1 2025 saw a "wind drought." Mother Nature doesn't care about quarterly guidance.

- Geopolitics: Taiwan Strait tensions always loom over the Hai Long project valuation.

Key Risks to Watch

- Project Delays: The Hai Long project is the elephant in the room. It is massive (1 GW). If it comes online late (past 2026), the stock will suffer.

- Interest Rates: If inflation spikes and rates stay high, NPI's debt servicing costs will eat into the new, lower dividend.

- Regulatory Shifts: Changes in clean energy credits in Canada or the EU could alter project IRRs overnight.

Conclusion: The "Show Me" Story

Northland Power’s 1.5% rise on December 24, 2025, is a sigh of relief, not a victory lap. The company has effectively hit the "Reset" button. By cutting the dividend, they have chosen balance sheet safety over yield chasing.

The Verdict:

- For Income Investors: The 4% yield (at $17.91) is safe but no longer sector-leading.

- For Value Investors: Trading at depressed multiples with massive projects coming online in 2026/27, NPI is a classic "turnaround" play. If they execute Hai Long without delays, $17.91 will look like a steal. If they stumble, $15 is in play.

Please wait processing your request...

Please wait processing your request...