The final trading days of 2025 are proving lucrative for gold bugs. On December 30, 2025, OceanaGold Corporation (TSX: OGC) surged ~2.4%, outperforming several mid-tier peers and catching the eye of retail and institutional investors alike.

But this isn't just a "rising tide lifts all boats" scenario—OceanaGold is riding a wave of fundamental breakthroughs, strategic permit approvals, and a debt-free balance sheet that makes it a standout in the materials sector.

Key Reasons & Drivers for the Dec 30 Surge

Several tailwinds converged to push OGC higher as the year winds down:

Source: Kalkine Group

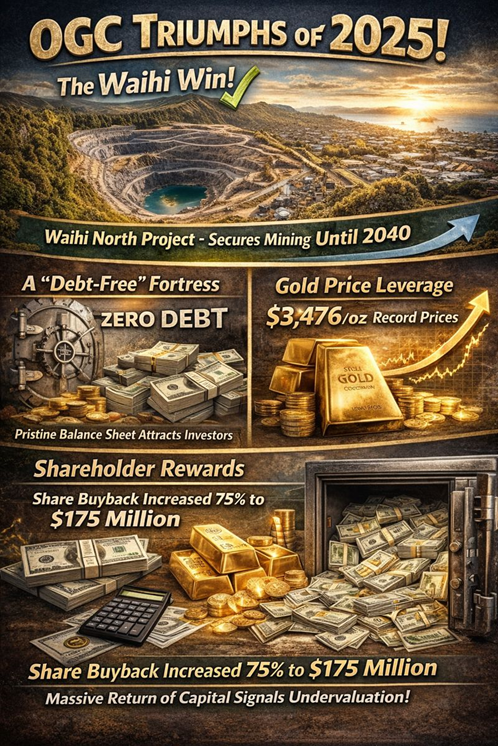

- The "Waihi Win": On December 18, 2025, the company received the final "Fast-Track" permit approval for the Waihi North Project in New Zealand. This was a massive de-risking event that ensures mining operations in the district until at least 2040.

- A "Debt-Free" Fortress: Investors are flocking to OGC’s pristine balance sheet. As of the latest updates, the company reports zero debt and a massive cash cushion of $335M, a rare feat for an intermediate producer in a capital-intensive industry.

- Gold Price Leverage: With realized gold prices hitting records (averaging $3,476/oz in the latter half of 2025), OGC’s "unhedged" status means 100% of that upside flows directly to the bottom line.

- Shareholder Rewards: The company recently increased its share buyback program by 75% to $175 million, signaling management's belief that the stock remains undervalued despite recent gains.

Latest Business Model: The "Intermediate Powerhouse"

OceanaGold has transitioned from a high-debt explorer to a high-margin, free-cash-flow (FCF) machine. Its business model now rests on four pillars:

- Multi-Jurisdictional Diversity: Operating in the USA (Haile), Philippines (Didipio), and New Zealand (Macraes & Waihi).

- Organic Growth over M&A: Instead of expensive acquisitions, OGC is spending $40M+ annually on exploration to find "gold under the doorstep" at existing sites.

- Copper By-Product: The Didipio mine provides significant copper credits, which acts as a natural hedge and lowers the All-In Sustaining Cost (AISC) for gold production.

- Tier-1 Jurisdiction Focus: A heavy tilt toward the United States and New Zealand provides a lower risk profile compared to miners operating solely in emerging markets.

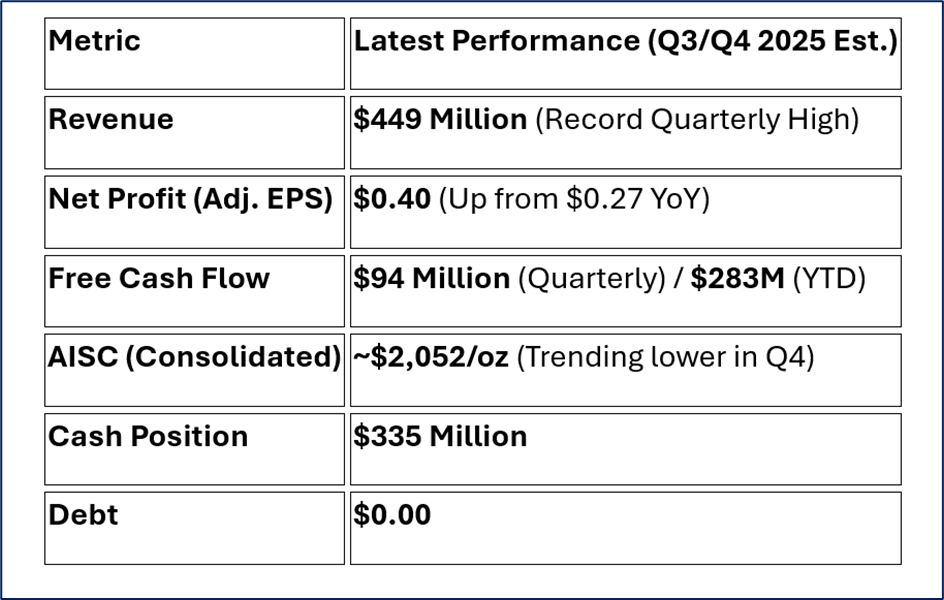

Financial & Operational Snapshot (2025 Update)

Source: Company Data

Operational Milestone: The Haile Gold Mine in the USA has successfully transitioned into higher-grade ore zones in late 2025, which is expected to make Q4 the strongest quarter of the year.

SWOT Analysis: The Hard Truths

Source: Kalkine Group

Strengths

- Zero Debt: Complete financial flexibility.

- High Margins: EBITDA margins sitting at a robust 46-50%.

- Unhedged: Direct exposure to spot gold prices.

Weaknesses

- High AISC: Compared to "Majors" like Barrick or Newmont, OGC’s sustaining costs are higher (over $2,000/oz), making them more sensitive to gold price drops.

- Geographic Concentration: Significant reliance on New Zealand’s regulatory environment.

Opportunities

- Wharekirauponga (WKP): The high-grade discovery at WKP is being hailed as a "company maker" with the potential for ultra-low-cost production.

- U.S. Listing: Ongoing rumors and steps toward a potential U.S. stock exchange listing to unlock higher valuation multiples.

Threats

- Environmental Opposition: Anti-mining groups in New Zealand (e.g., Coromandel Watchdog) remain active and could challenge future expansions.

- Resource Depletion: Constant need for exploration success to replace mined ounces.

Risks to Watch

- Gold Price Volatility: While gold is at record highs, any hawkish pivot by central banks could cool the "safe haven" trade.

- Operational Disruptions: Mining is inherently dangerous; any geotechnical issues at the Haile pit or Didipio underground could halt cash flow.

- Currency Fluctuations: OGC operates in NZD, PHP, and USD, but reports in USD. Strengthening local currencies can inflate operating costs.

Conclusion

OceanaGold’s 2.4% jump on December 30 isn't a fluke; it's the market finally pricing in the successful execution of the 2025 turnaround plan. With the Waihi North permit in hand, a $175M buyback in progress, and zero debt, OGC has entered 2026 as one of the leanest and most cash-generative mid-tier miners on the TSX.

Please wait processing your request...

Please wait processing your request...