_01_05_2026_16_59_02_096621.jpg)

Orla Mining Ltd. (TSX: OLA) started the first trading week of 2026 with a decisive jump, gaining ~4.3% on January 5 to trade around CAD 18.88.

While the broader gold sector benefited from macroeconomic tailwinds, Orla’s outperformance is a direct result of its transformation from a single-asset developer into a multi-asset producer with a newly minted dividend policy.

Key Drivers for the Jan 5 Surge

Source: Kalkine Group

The rally was fueled by a "perfect storm" of operational recovery and investor-friendly capital allocation:

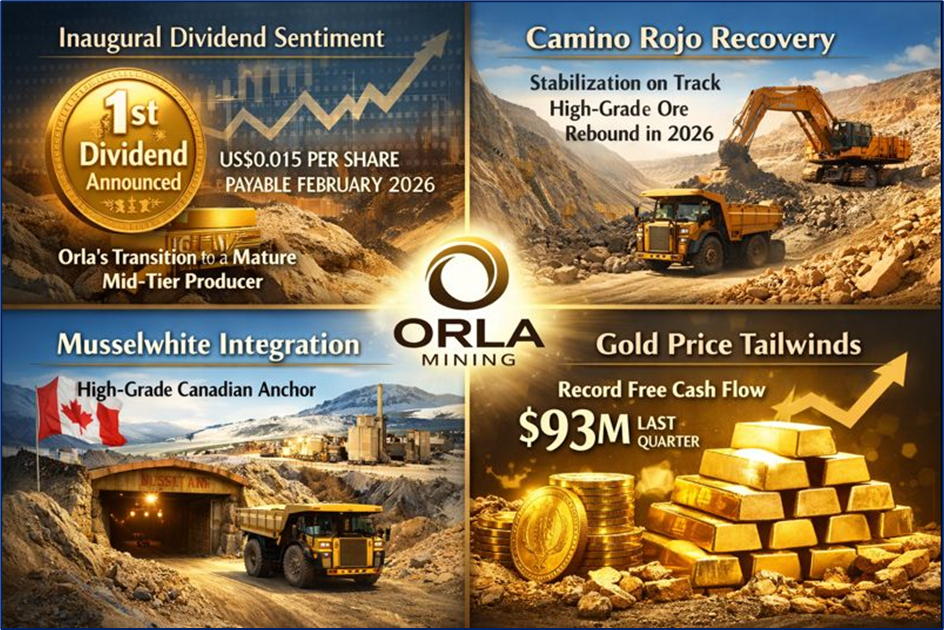

- Inaugural Dividend Sentiment: The market continues to react positively to Orla’s December announcement of its first-ever quarterly dividend (US$0.015 per share), payable in February 2026. This marks Orla's transition to a "mature" mid-tier producer.

- Camino Rojo Recovery: Following a pit wall event in mid-2025, recent updates confirm that the stabilization plan is on track. Investors are buying into the "rebound" story as the mine re-sequences toward higher-grade ore in 2026.

- Musselwhite Integration: The Musselwhite Mine (acquired in early 2025) has exceeded integration expectations, providing a stable, high-grade Canadian anchor that balances the jurisdictional risks of Mexico and Nevada.

- Gold Price Tailwinds: As 2026 begins, gold prices remain robust, amplifying Orla's record free cash flow ($93M reported in the most recent quarter).

Latest Business Model & Strategy

Orla has shifted its business model from high-risk exploration to a low-cost, high-margin production engine.

- The "Three Pillars" Strategy: Orla now operates in three tier-1 mining jurisdictions:

- Mexico (Camino Rojo): Low-cost, open-pit heap leach (Oxide) and long-term underground potential (Sulphide).

- Canada (Musselwhite): High-grade underground production providing stable CAD-denominated cash flow.

- USA (South Railroad): The next growth leg in Nevada, currently in the final permitting stages.

- Self-Funded Growth: Unlike many peers, Orla is using its internal cash flow to fund the construction of the South Railroad project (estimated $200M capex) while simultaneously paying dividends.

Financial & Operational Update (2025–2026)

Source: Company Data

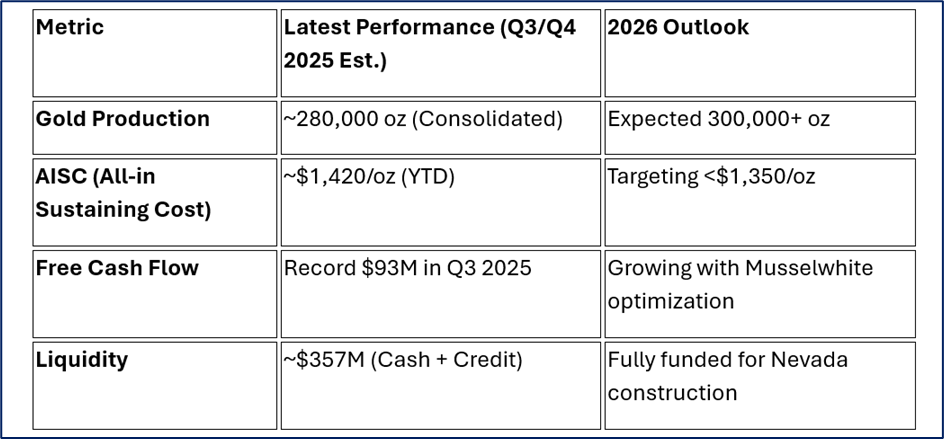

Operational Milestones:

- South Railroad (Nevada): Achieved FAST-41 coverage, a federal designation that streamlines the permitting process. A final Record of Decision (ROD) is expected in Q2 2026.

- Camino Rojo Sulphides: A Preliminary Economic Assessment (PEA) for the massive underground sulphide resource is expected in early 2026, which could significantly extend the mine's life beyond a decade.

SWOT Analysis: The Orla Outlook

Source: Kalkine Group

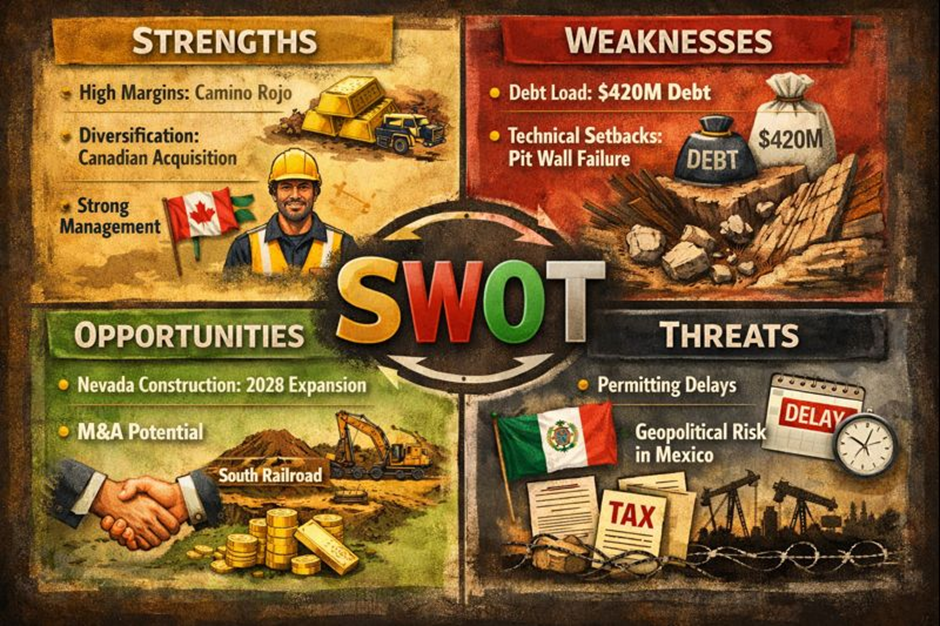

Strengths

- High Margins: Camino Rojo remains one of the lowest-cost gold mines in the world.

- Diversification: Recent Canadian acquisition reduces "single-mine" risk.

- Management: Led by Jason Simpson, the team has a track record of meeting or beating construction timelines.

Weaknesses

- Debt Load: ~$420M in total debt following the Musselwhite acquisition, though offset by high cash levels.

- Technical Setbacks: The 2025 pit wall event showed vulnerability to geotechnical risks.

Opportunities

- Nevada Construction: Breaking ground at South Railroad in mid-2026 will be a major re-rating catalyst.

- M&A: Orla’s strong cash flow makes it a potential "consolidator" of other junior miners.

Threats

- Permitting Delays: Any delay in Nevada’s Q2 2026 permitting could dampen momentum.

- Geopolitical Risk: Potential tax or mining law changes in Mexico.

Key Risks to Watch

- Geotechnical Stability: Investors will be watching the Q1 2026 results to ensure no further movement in the Camino Rojo pit walls.

- Inflationary Pressures: While gold prices are high, the cost of labor and energy in Canada (Musselwhite) remains a pressure point for AISC.

- Jurisdictional Concentration: While diversified, a large portion of value remains tied to Mexico, which has seen fluctuating sentiment toward foreign mining entities.

Conclusion

Orla Mining’s 4.3% jump today isn't just a "gold price" move; it's a validation of the company's evolution. By balancing a new dividend program with aggressive growth in Nevada and operational stability in Canada, Orla is positioning itself as a "top-pick" mid-tier gold producer for 2026.

Please wait processing your request...

Please wait processing your request...