1. Market Snapshot: Why the 1.9% Pop?

Peyto Exploration & Development Corp. (TSX: PEY) caught a bid on Monday, Dec 29, outperforming the broader energy index. While no singular "breaking news" dropped mid-day, the move aligns with a perfect storm of seasonal and fundamental drivers that retail investors love.

Source: Kalkine Group

- The "Winter Premium" Trade: Late December often signals peak heating demand. With cold snaps forecasted across North America for early 2026, natural gas prices (AECO and NYMEX) are seeing support. Peyto, being a gas-weighted pure play, acts as a leveraged proxy to these prices.

- Dividend Locking: Investors are likely positioning ahead of the January 2026 dividend (confirmed at $0.11/share). The 1.9% gain reflects "dividend capture" psychology combined with safety seeking in high-yield assets as we close out the 2025 tax year.

- Technical Rebound: After some tax-loss selling pressure earlier in December, bargain hunters are stepping in. The stock is reacting to the realization that 2026 hedges (at ~$4.00/Mcf) are locking in robust free cash flow regardless of short-term volatility.

2. The "Deep Basin" Machine: 2025 Business Model Update

Peyto remains the lowest-cost producer in Canada, but its 2025 strategy has evolved from simple "drill and fill" to a more sophisticated Integrated Margin Model.

- The Repsol Asset Integration: The major acquisition from late 2023 is now fully optimized. Peyto isn't just drilling; they are filling their own plants (1.5 Bcf/d capacity) with their own gas. This vertical integration allows them to capture the processing margin that peers pay to third parties.

- Diversification Beyond AECO: The "fatal flaw" of Canadian gas was always the AECO price discount. Peyto’s 2025 model aggressively bypasses this. Through diversification to Henry Hub, Ventura, and Emerson, they are realizing prices significantly higher than local Alberta benchmarks.

- LNG Canada Readiness: With LNG Canada Phase 1 effectively entering commercial operations (mid-2025 startup), Peyto is positioned as a key feeder. The physical pull of gas toward the West Coast is finally tightening the AECO market, lifting the floor price for Peyto’s unhedged volumes.

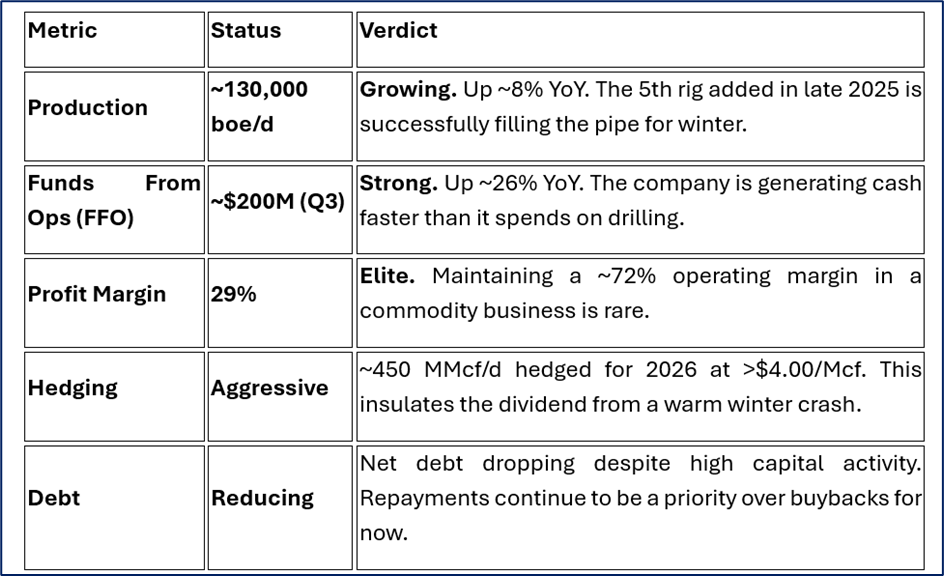

3. Financial & Operational Health (Q3/Q4 2025 Context)

Based on latest available data (Q3 2025 Reporting)

Source: Company Data

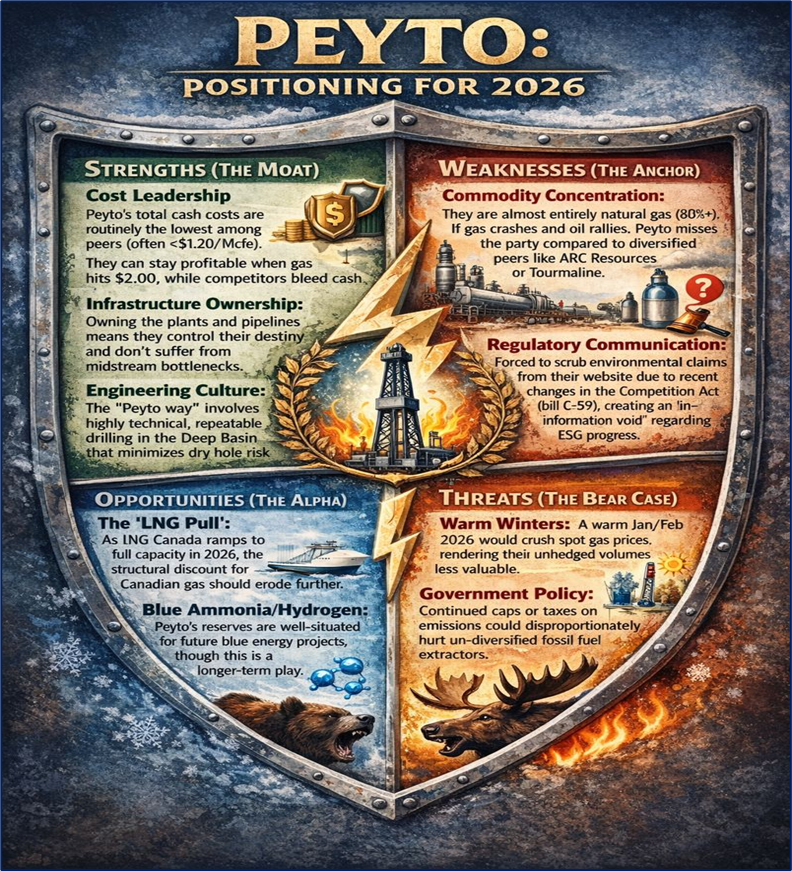

4. SWOT Analysis

Source: Kalkine Group

Strengths (The Moat)

- Cost Leadership: Peyto’s total cash costs are routinely the lowest among peers (often <$1.20/Mcfe). They can stay profitable when gas hits $2.00, while competitors bleed cash.

- Infrastructure Ownership: Owning the plants and pipelines means they control their destiny and don't suffer from midstream bottlenecks.

- Engineering Culture: The "Peyto way" involves highly technical, repeatable drilling in the Deep Basin that minimizes dry hole risk.

Weaknesses ( The Anchor)

- Commodity Concentration: They are almost entirely natural gas (88%+). If gas crashes and oil rallies, Peyto misses the party compared to diversified peers like ARC Resources or Tourmaline.

- Regulatory Communication: Recent amendments to the Competition Act (bill C-59) forced Peyto to scrub environmental claims from their website to avoid litigation risks, creating an "information void" regarding their ESG progress.

Opportunities (The Alpha)

- The "LNG Pull": As LNG Canada ramps to full capacity in 2026, the structural discount for Canadian gas should erode further.

- Blue Ammonia/Hydrogen: Peyto’s reserves are well-situated for future blue energy projects, though this is a longer-term play.

Threats (The Bear Case)

- Warm Winters: A warm Jan/Feb 2026 would crush spot gas prices, rendering their unhedged volumes less valuable.

- Government Policy: Continued caps or taxes on emissions could disproportionately hurt un-diversified fossil fuel extractors.

5. Key Risks to Watch

- AECO Volatility: Despite diversification, a significant portion of volume is still exposed to Alberta pricing. If the NGTL system gets bottlenecked (maintenance/outages), local prices can invert to negative, forcing shut-ins.

- Interest Rates: While rates are stabilizing, Peyto carries debt. Higher-for-longer rates eat into the free cash flow available for dividends.

- Execution Risk: The 2026 capital program ($450M-$500M) relies on efficient drilling. Any service cost inflation (rigs, labor) could squeeze margins.

6. Conclusion: The "Sleep Well at Night" Gas Stock?

Peyto’s 1.9% rise on Dec 29, 2025, isn't a speculative pump—it’s a recognition of resilience. In a world of volatile energy transitions, Peyto offers a simple proposition: We produce gas cheaper than anyone else, and we pay you monthly to wait for higher prices.

With the dividend yielding handsomely and 2026 production hedged at profitable levels, the stock remains a favorite for retail income investors who believe in the long-term "Gas is the Bridge" thesis.

Please wait processing your request...

Please wait processing your request...