On December 24, 2025, Colliers International Group Inc. (TSX: CIGI) saw its shares climb approximately 0.82%, closing at CAD 205.52. While a sub-1% move might seem quiet, it represents a significant resilience in a year defined by high-interest rates and shifting global capital.

The move on Christmas Eve wasn't just holiday cheer—it was the result of a strategic pivot from a traditional brokerage to a high-margin, engineering-heavy professional services powerhouse.

Key Drivers: What Pushed the Needle on Dec 24?

The modest uptick on the final trading day before Christmas was fueled by a combination of macro optimism and specific corporate tailwinds:

Source: Kalkine Group

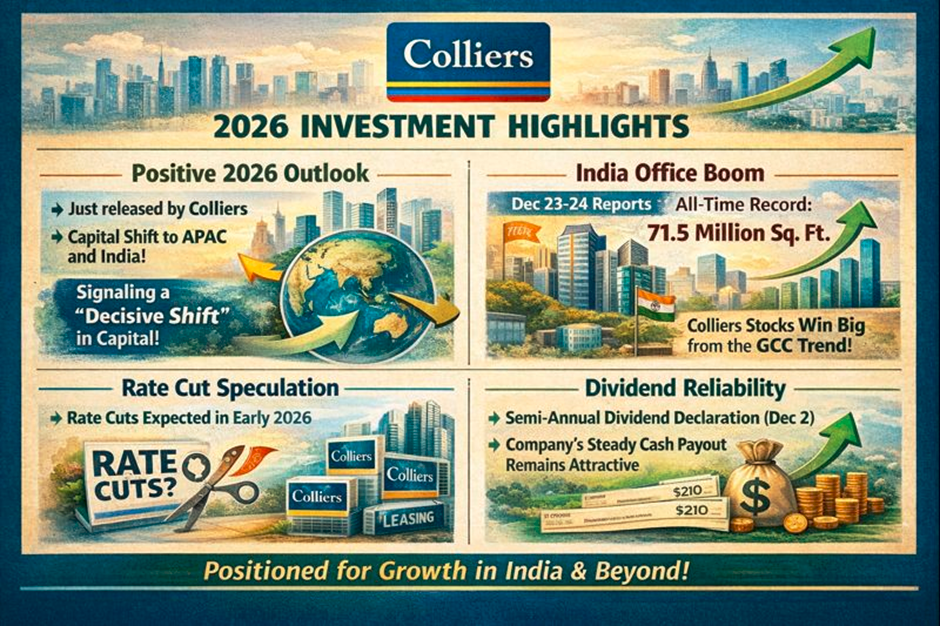

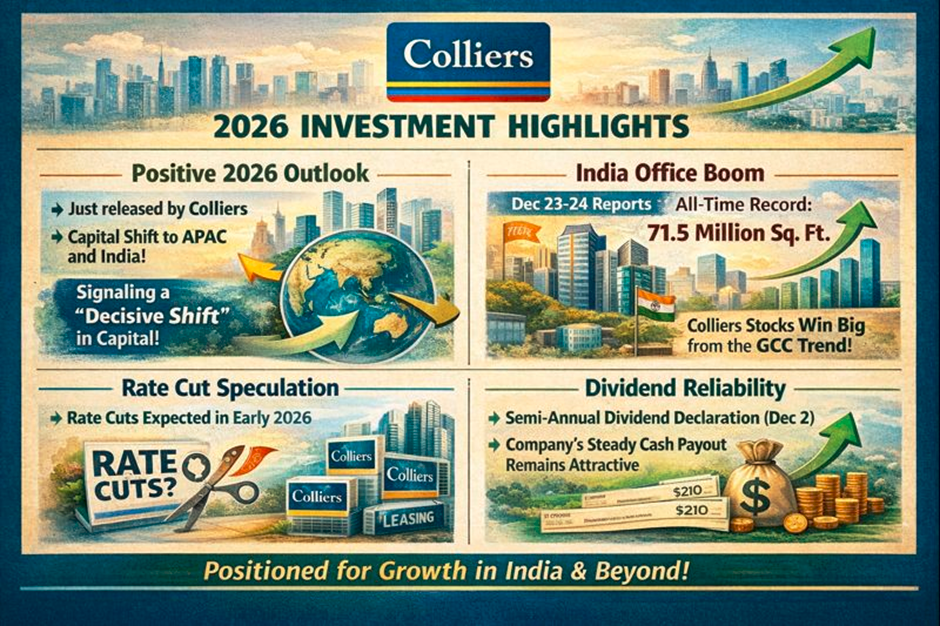

- Positive 2026 Outlook: Just weeks prior, Colliers released its 2026 Global Investor Outlook, signaling a "decisive shift" in capital back to real estate, particularly in the APAC region and India.

- India Office Boom: On Dec 23-24, reports surfaced that Indian office leasing hit an all-time high of 71.5 million sq. ft. in 2025. As a dominant player in that market, Colliers is seen as the primary beneficiary of the "Global Capability Centre" (GCC) trend.

- Rate Cut Speculation: Investors used the final sessions of 2025 to position for a "normalization" of interest rates in early 2026, which historically triggers a surge in Colliers’ Capital Markets and Leasing segments.

- Dividend Reliability: The company’s recent semi-annual dividend declaration (Dec 2) reminded retail investors of its stable yield in an uncertain environment.

The 2025 Business Model: Not Your Grandfather’s Brokerage

Colliers has spent 2025 aggressively shedding its image as a simple real estate broker. The "New Colliers" model is built on three pillars:

- Engineering & Design (The Growth Engine): Now accounting for roughly 31% of revenue, this segment provides steady, long-term infrastructure consulting that isn't tied to the volatile housing or office sales market.

- Investment Management (The Margin King): With over $108 Billion in Assets Under Management (AUM), this segment provides recurring, high-margin fee income.

- Real Estate Services (The Legacy Core): While still the largest by volume, this segment is increasingly focused on Outsourcing and Advisory (recurring revenue) rather than one-off transaction commissions.

Latest Financial & Operational Updates (Q3/Q4 2025)

Colliers enters the end of 2025 with a "Beat and Raise" momentum:

- Q3 Revenue Surge: Reported $1.46 Billion, a massive 24% increase year-over-year.

- Earnings Beat: Adjusted EPS hit $1.64, surpassing analyst forecasts of $1.58.

- Recurring Income: A record 70% of earnings now come from recurring services, drastically reducing the "boom or bust" risk of the past.

- AI Integration: In December 2025, Colliers partnered with Google Cloud to deploy AI-powered property valuation and predictive analytics, aiming to cut operational costs by 15%.

SWOT Analysis: A Strategic Deep-Dive

Source: Kalkine Group

Risks to Watch in 2026

- Execution Risk: The company's "Enterprise '25" strategy relies on perfectly integrating a dozen different engineering and investment firms. Any cultural clash could stall growth.

- The "Office Crisis" Narrative: While Colliers' data shows a rebound, a sudden shift back to remote work or a global recession could hit the Leasing segment hard.

- Currency Fluctuations: As a global entity, a strong USD/CAD can eat into reported earnings from international operations.

Conclusion

Colliers International closed 2025 on a high note, not because the real estate market is "back to normal," but because the company successfully de-risked its revenue stream. By pivoting into engineering and investment management, Colliers has built a "weather-proof" model that can grow even when skyscrapers aren't selling. For the retail investor, the 0.8% rise on Dec 24 is a signal of stability in a portfolio that values both growth and resilience.

Please wait processing your request...

Please wait processing your request...