Performance Drivers: Why FNV Jumped on January 8, 2026

The nearly 4% rally in Franco-Nevada (TSX: FNV) during the January 8 trading session was fueled by a convergence of macroeconomic tailwinds and specific asset-level recovery news. Investor sentiment shifted significantly as the broader gold market continued its record-breaking run, with spot prices remaining elevated due to persistent central bank demand and structural safe-haven buying.

Source: Kalkine Group

- Cobre Panama Re-authorization: A major catalyst was the renewed progress regarding the Cobre Panama mine. Reports indicating that the government and First Quantum have advanced toward a stable operational restart provided a massive relief rally, as this asset represents a significant portion of FNV's potential revenue.

- Safe Haven Rotation: Market volatility early in the year led institutional investors to rotate into "low-risk" mining exposure. FNV, as a royalty player, is often viewed as a defensive gold play compared to direct miners.

- Record Margins: News of the company maintaining its ~90% gross profit margins even as operating costs rose for traditional miners underscored the resilience of the streaming business model.

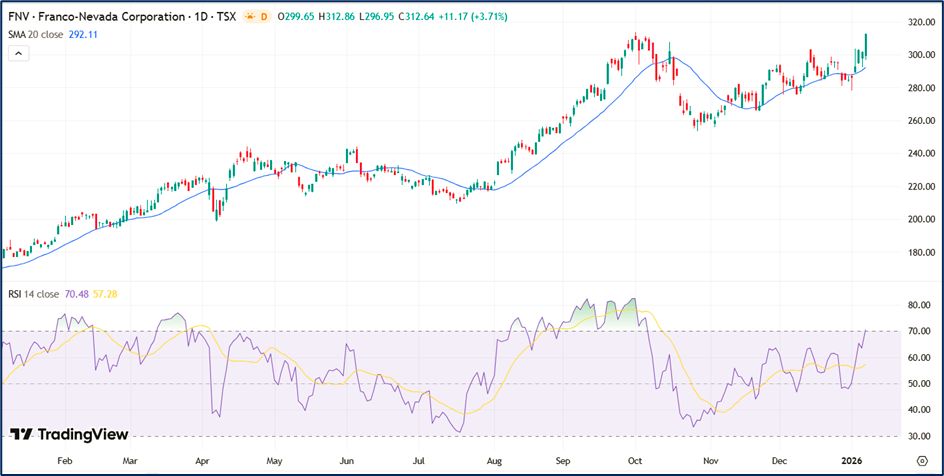

Current Technical Analysis

Source: Trading View

Franco-Nevada’s technical profile transitioned into a "Blue Sky" breakout phase as of early January 2026. After hitting an all-time high of approximately $312.64 CAD (and $225.70 USD), the stock successfully cleared its 52-week resistance levels with significant volume.

- Moving Averages: The stock is trading well above its 50-day SMA ($281.82) and 200-day SMA ($264.48), confirming a robust long-term bullish trend.

- RSI and Momentum: The Relative Strength Index (RSI) is currently in the overbought territory (above 70), which typically indicates strong momentum but also warns of a possible short-term consolidation or "cooling off" period.

- Support Levels: Current immediate support is found at the previous resistance level of $303. If the stock retreats, the 15-day moving average near $292 acts as a secondary buffer.

Latest Analyst Ratings: Upgrades and Targets

The analyst community has turned increasingly bullish on Franco-Nevada as the 2026 fiscal year begins. The consensus rating has shifted toward a "Moderate Buy" with several key upward revisions.

- RBC Capital: Recently upgraded the stock from "Sector Perform" to "Outperform" and raised the price target to $250.00 USD (approx. $345 CAD).

- UBS Group: Boosted their price objective to $270 USD, citing attractive valuation relative to the explosive growth in the gold sector.

- CIBC: Issued one of the most aggressive targets at $460 CAD, reflecting a belief that the market is still underestimating the long-term cash flow from the Cobre Panama restart.

- Scotiabank: Maintains a more cautious "Hold" rating but raised the floor of its valuation to $184 USD to account for higher realized gold prices.

Business Model: The Royalty & Streaming Advantage

Franco-Nevada operates as the world’s leading gold-focused royalty and streaming company. Unlike traditional mining firms, it does not manage mines, hire labor, or maintain heavy machinery. Instead, it provides upfront capital to miners in exchange for the right to a percentage of the metal produced for the life of the mine.

- Inflation Insulation: Because FNV's costs are largely fixed at the time of the contract, it is uniquely protected from the rising labor and fuel costs that often erode the profits of actual mining operators.

- Diversification: The portfolio is highly diversified across gold (approx. 65%), silver (15%), and energy/transition metals (10%), spreading risk across hundreds of assets.

- Scalability: The company operates with a very lean corporate team, allowing it to generate massive EBITDA margins (often exceeding 80%) with minimal overhead.

Latest Financial and Operational Updates

The company’s most recent reports highlight a period of record-setting financial efficiency. With revenue surpassing $487.7 million in the latest quarter, the company is on track for a record-breaking 2026.

- Earnings Beat: FNV reported an EPS of $1.43, comfortably beating the consensus estimate of $1.38. This was driven by a 100% surge in stream revenues.

- Dividend Consistency: The board recently declared its 18th consecutive year of dividend increases, a rarity in the volatile mining sector.

- Geographic Pivot: While Panama remains a focus, the company has aggressively added new royalties in stable jurisdictions like North America and Australia to mitigate geopolitical risks.

Critical Risks to Consider

Despite the record highs, Franco-Nevada is not without its challenges. Investors continue to monitor several key "bottleneck" risks that could impact the stock's trajectory.

- Concentration Risk: A large portion of FNV's valuation is tied to just a handful of tier-one assets. Any regulatory or environmental setback at sites like Cobre Panama or Candelaria has a disproportionate impact on the share price.

- Commodity Volatility: While the company is insulated from operating costs, it is 100% exposed to commodity price fluctuations. A sudden drop in gold or silver prices would directly hit the bottom line.

- Jurisdictional Tension: Increased "resource nationalism" in developing nations can lead to tax disputes or contract renegotiations, as seen in the company’s recent (though now settled) Canadian tax disputes.

Conclusion

Franco-Nevada’s 4% jump on January 8, 2026, serves as a validation of its "asset-light" philosophy during a period of mining sector volatility. By hitting all-time highs, the stock has proven its ability to capture the upside of record gold prices while providing a safety net against the inflation-driven cost pressures facing its peers. While the technical indicators suggest the stock is currently "hot," the fundamental support from analyst upgrades and improved asset clarity in Panama suggests a new baseline for the company’s valuation in the 2026 market.

Please wait processing your request...

Please wait processing your request...