Seabridge Gold (TSX: SEA) closed up approximately 1.9% on December 30, 2025, capping off a year of massive outperformance. While a 2% daily move might seem modest in the volatile mining sector, the context is everything: SEA has gained over 100% year-to-date, and this late-December nudge reflects a market finally pricing in the "optionality" that CEO Rudi Fronk has preached for decades.

With the KSM Project—the world's largest undeveloped gold-copper project—sitting on the verge of a major partnership and a massive spin-out on the horizon, the "Retail Catchy" narrative is shifting from "long-term potential" to "imminent catalyst."

Key Drivers: Why SEA Moved on Dec 30

The 1.9% lift is a result of three converging factors that hit the wire in the final weeks of 2025:

Source: Kalkine Group

- The "Valor Gold" Spin-Out Momentum: On December 16, 2025, Seabridge announced the spin-out of its Courageous Lake Project into a new entity, Valor Gold. Retail investors are bidding up SEA to capture the "free" shares of Valor, which holds 11 million ounces of gold that management argues are currently valued at "zero" by the market.

- KSM Partnership Anticipation: Although the company missed its self-imposed year-end 2025 deadline for a Joint Venture (JV) announcement, the December 18 update confirmed that three finalists have completed site visits. The market is betting on a "New Year’s Surprise" in Q1 2026.

- Gold Price Tailwinds: With gold prices up over 30% in 2025, Seabridge’s leverage—holding more gold per share than any other company—is acting as a force multiplier for the stock price.

Latest Business Model & Strategy

Seabridge does not operate mines; it builds value through the drill bit and then seeks to partner with "majors" to handle the multi-billion dollar CAPEX of construction.

- The Goal: Maintain a significant carried interest in world-class mines while minimizing share dilution and capital exposure.

- The Asset Base: A staggering 183M oz of gold and 59B lbs of copper in the ground.

- Current Focus: Transitioning KSM from "exploration" to "construction-ready" through its "Substantially Started" status and the Mitchell-Treaty Tunnel (MTT) development.

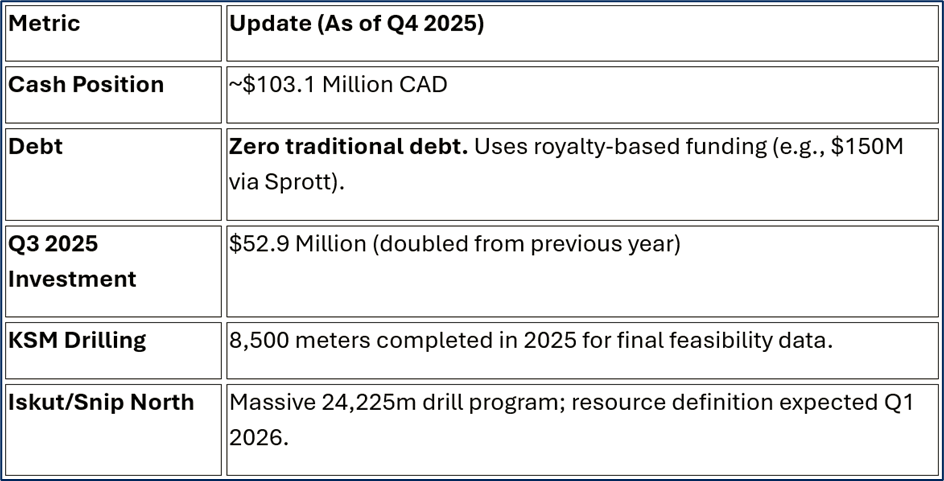

2025 Financial & Operational Snapshots

Seabridge’s financials are those of a classic developer: heavy spending, zero revenue, but a rock-solid balance sheet.

Source: Company Data

SWOT Analysis: The 2026 Outlook

Source: Kalkine Group

Strengths

- Asset Magnitude: Largest gold-copper reserves of any junior/developer globally.

- Jurisdiction: Projects are located in Canada (BC, NWT, Yukon) and Nevada, avoiding high-risk geopolitical zones.

- Capital Structure: No traditional debt; significant insider ownership (over 30%).

Weaknesses

- Capex Intensity: KSM requires billions to build, making the company entirely dependent on finding a "Major" partner (like a Rio Tinto or Barrick).

- Unprofitability: The company will remain pre-revenue for years.

Opportunities

- Valor Gold Spin-Out: Unlocking value from Courageous Lake as a standalone high-grade open-pit play.

- Copper Demand: With 59B lbs of copper, SEA is as much a "Green Energy" play as it is a gold play.

Threats

- Legal Challenges: Tudor Gold and environmental groups have challenged the "Substantially Started" designation; a court decision is expected in Q1 2026.

- Permit Delays: The M-245 tunnel permit amendment is still pending (expected Q1 2026).

Critical Risks to Watch

Investors should not ignore the "Red Flags" highlighted in recent filings:

- Dilution Risk: While they raised US$100M in 2025, future delays in a JV partner could force more equity raises.

- Technical Complexity: The Mitchell-Treaty Tunnels are a massive engineering feat. Any setback here delays the entire KSM project.

- Market Sensitivity: SEA’s high beta means if the gold price corrects, the stock could drop significantly faster than the metal itself.

Conclusion

Seabridge Gold's 1.9% move on December 30 isn't a random fluctuation—it is the sound of the market "positioning" for a transformative 2026. Between the Valor Gold spin-out and the imminent KSM partnership, the "optionality" story is finally becoming a "liquidity" story. However, the pending legal decisions and the high-stakes JV negotiations mean the road ahead remains as steep as the mountains in the Golden Triangle.

Please wait processing your request...

Please wait processing your request...