Discovery Silver (TSX: DSV) surged nearly 8% on December 22, 2025, closing at CAD 9.07. This wasn't a random fluctuation; it was a perfect storm of macro tailwinds and a radically transformed business model that the market is finally pricing in.

Here is the analytical breakdown of the move, the drivers, and the new reality for DSV.

Source: Kalkine Group

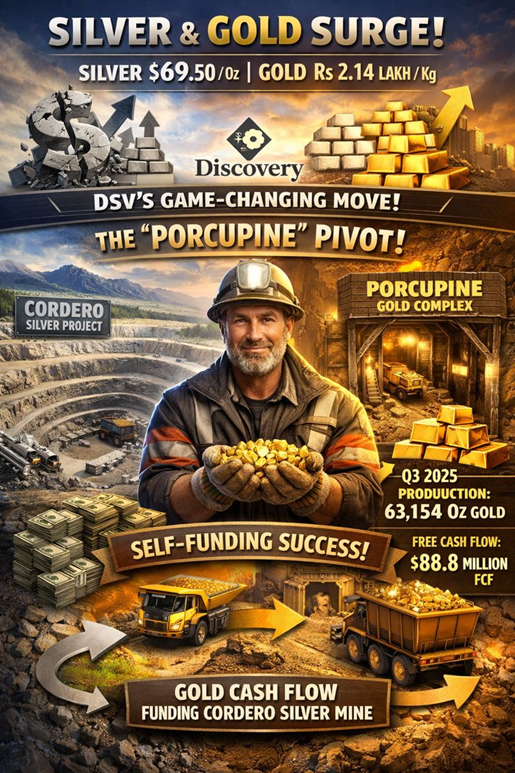

1. The Macro "Super-Fuel": Silver Hits $69

The primary engine behind the 8% rise is the historic breakout in silver prices.

- Record Highs: Silver futures smashed through $69.50 USD/oz globally and Rs 2.14 Lakh/kg on the MCX.

- The Catalyst: The Fed’s aggressive rate cuts combined with cooling inflation have weakened the dollar, sending "hard assets" like gold and silver parabolic.

- Why DSV Benefits: Discovery Silver has historically been a "leverage play." For every $1 rise in silver, DSV’s massive resource base (Cordero) typically reprices aggressively. Yesterday, the entire sector lifted, but DSV outperformed because of its unique new leverage (see below).

2. The Game Changer: The "Porcupine" Pivot

The market is waking up to the fact that DSV is no longer just a developer burning cash—it is now a producer generating it.

In 2025, Discovery Silver completed the acquisition of the Porcupine Gold Complex (formerly Newmont). This fundamentally altered their DNA:

- From Developer to Producer: DSV is now producing gold. In Q3 2025 alone, they produced 63,154 ounces of gold.

- Free Cash Flow (FCF): They generated $86.8 million in FCF in Q3.

- The Strategy: Instead of diluting shareholders to build their flagship Cordero silver project, they are using cash flow from the Porcupine gold mines to fund it. This "self-funding" model is rare for juniors and commands a premium valuation.

3. Business Model: The "Hybrid" Engine

DSV has evolved into a two-pronged beast, reducing the binary risk usually associated with silver explorers.

- Engine 1 (Cash Cow): Porcupine Gold Operations (Ontario, Canada).

- Role: Generate immediate cash to strengthen the balance sheet ($341M cash on hand).

- Upside: Doubling production through mill expansion (targeting 9M tonnes/year).

- Engine 2 (Growth): Cordero Project (Chihuahua, Mexico).

- Role: The world-class silver leverage. One of the largest undeveloped silver deposits globally.

- Status: Moving through final permitting. The goal is to build this using the gold profits from Engine 1.

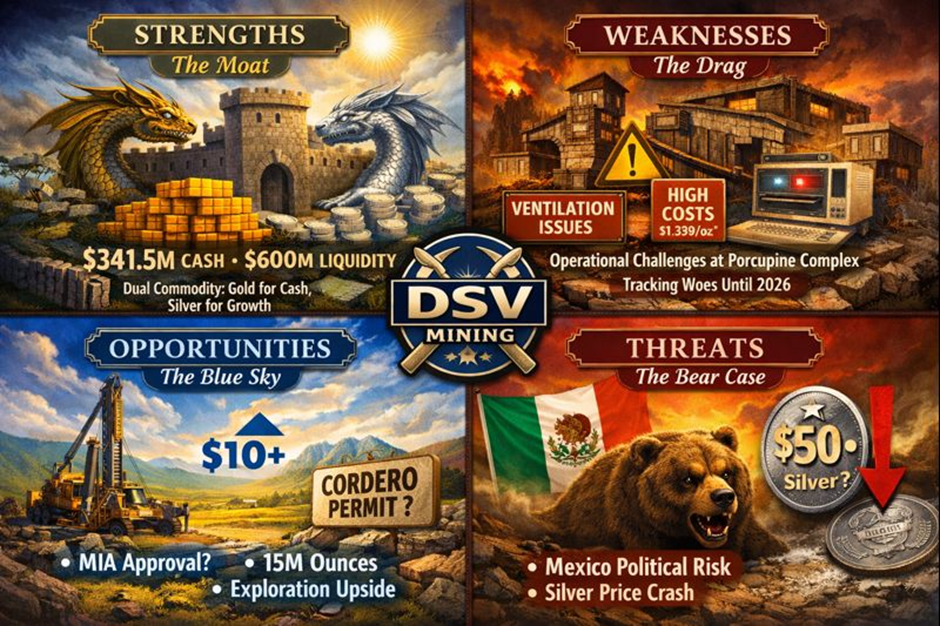

4. SWOT Analysis

Source: Kalkine Group

Strengths (The Moat) DSV is cash-rich in a sector starved for capital. With $341.5M in cash and total liquidity near $600M, they are bulletproof against short-term volatility. The dual-commodity exposure (Gold for cash, Silver for growth) dampens the risk of a single metal crashing.

Weaknesses (The Drag) Operational "growing pains" at the newly acquired Porcupine complex are real. Q3 saw ventilation constraints and mill maintenance issues, keeping costs high ($1,339/oz operating cash cost). They are also working with legacy systems that make granular cost tracking difficult until mid-2026.

Opportunities (The Blue Sky)

- The Cordero Permit: CEO Tony Makuch hinted that recent Mexican permit approvals are a positive sign. Receiving the MIA (environmental permit) for Cordero would be a massive re-rating event, potentially sending the stock well past $10.

- Exploration: The Porcupine land package has 15 million ounces of resources. Aggressive drilling could unlock new high-grade zones.

Threats (The Bear Case)

- Mexico Jurisdiction: Political risk remains the elephant in the room. Any changes to Mexican mining laws or permit denials for Cordero would crush the "Growth" half of the thesis.

- Silver Volatility: If silver retreats from $69 back to $50, the premium currently being built into the stock will evaporate.

5. Financial Snapshot (Q3 2025)

- Revenue: $237 Million (Up 67% QoQ).

- EPS: $0.08 (Beat expectations of $0.07).

- Cash Position: $341.5 Million (Up 35%).

- EBITDA: $122 Million.

Key Takeaway: The company is profitable and liquid. The revenue miss in Q3 was minor compared to the massive jump in Free Cash Flow.

6. Risks to Watch

- Execution Risk: Can they actually double Porcupine's mill capacity without cost blowouts?

- Inflation: Mining cost inflation (labor, energy) could eat into the margins that are currently looking so healthy due to high metal prices.

Conclusion: The "Perfect Storm" Rally

Discovery Silver's 8% rise on December 22 is justified. It is a lagging response to a company that has successfully de-risked itself. They are no longer begging the market for money; they are printing it in Ontario to build a silver giant in Mexico.

As long as silver holds above $60 and gold remains robust, DSV offers a rare mix of safety (cash flow) and explosive upside (Cordero).

Source: Trading View, 22 December 2025

Please wait processing your request...

Please wait processing your request...