- The Move: Breaking Down the ~12.2% Surge

On December 24, 2025, Aftermath Silver (TSXV: AAG) posted a sharp ~12.2% gain, closing near CAD 1.10. This double-digit move wasn't an isolated anomaly; it was a high-beta reaction to a historic macro event occurring simultaneously in the commodities market.

The primary catalyst was Silver spot prices shattering all-time highs, briefly touching ~$77 per ounce during the holiday trading week. As a junior explorer with significant in-ground leverage, Aftermath Silver acted as a "coiled spring," amplifying the metal's spot price gains. Investors aggressively bid up AAG to secure exposure to its newly expanded resource base at the Berenguela Project in Peru.

- Key Drivers: The "Perfect Storm" for AAG

Three distinct forces converged to drive this valuation re-rate:

Source: Kalkine Group

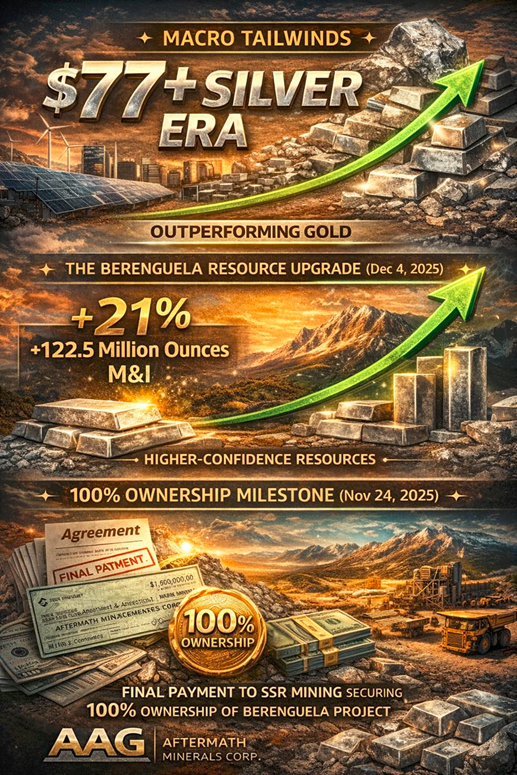

- Macro Tailwinds (The $77+ Silver Era): Silver is currently outperforming gold, driven by industrial panic-buying (solar/EVs) and monetary easing. With silver prices up over 150% in 2025, juniors like AAG—which define their value by ounces in the ground—are seeing their asset values theoretically double or triple overnight.

- The Berenguela Resource Upgrade (Dec 4, 2025): Just weeks prior, Aftermath released a pivotal update for its flagship Berenguela project. They successfully converted a massive chunk of "Inferred" resources to the higher-confidence "Measured & Indicated" (M&I) category.

- Key Stat: M&I Silver resources rose 21% to 122.5 million ounces.

- Why it matters: In a $77 silver environment, higher-confidence ounces command a premium valuation from potential acquirers.

- 100% Ownership Milestone: On November 24, 2025, the company completed its final payment to SSR Mining, securing 100% unencumbered interest in Berenguela. This removed a major "overhang" risk, making the stock cleaner for institutional investors or M&A activity.

- SWOT Analysis (Strategic Snapshot)

Source: Kalkine Group

Strengths (Internal)

- Asset Quality: Berenguela is not just a silver play; it is a polymetallic beast (Silver-Copper-Manganese). The manganese component is strategic for the EV battery supply chain, potentially attracting non-traditional partners.

- Jurisdictional Footprint: The project is located near Santa Lucia, Peru, with excellent infrastructure (road, rail, power lines within 6km).

- Management Pedigree: Led by Ralph Rushton and backed by heavyweights (historical ties to Eric Sprott), the team has a proven track record of raising capital even in bear markets.

Weaknesses (Internal)

- Pre-Revenue Status: AAG burns cash. It is entirely dependent on equity financing to fund the 2025/2026 drill programs.

- Metallurgical Complexity: Separating the manganese from silver/copper effectively and economically is the project's technical "Achilles heel," though recent test work has been positive.

Opportunities (External)

- M&A Takeover: With major miners desperate to replace depleting reserves, AAG’s 100M+ ounce resource makes it a prime acquisition target.

- Copper "Kicker": Recent drilling identified a "Copper East" zone with high-grade copper intercepts. If they can prove this is a large copper system with a silver cap, the valuation multiple expands significantly.

Threats (External)

- Peruvian Politics: While Peru is a mining powerhouse, political instability or community protests in the Puno region remain a persistent risk factor that can halt operations overnight.

- Silver Price Volatility: A sharp correction in silver prices (e.g., dropping back to $50) would disproportionately punish AAG’s stock price due to its leveraged nature.

- Latest Business Model

Aftermath Silver operates as a Resource Developer & De-risker. They do not currently intend to build the mine themselves (a CAPEX-heavy endeavor). Instead, their model is:

- Acquire undervalued assets with historical resources (Berenguela in Peru, Challacollo in Chile).

- Drill to expand the resource and increase confidence (Inferred $\to$ M&I).

- Optimize metallurgy and economics (PEA/PFS studies).

- Exit via sale to a mid-tier or major producer, or partner for construction.

Current Focus: The company is currently executing a 4,000m diamond drill program at Berenguela (started Dec 10, 2025) to further prove up the high-grade copper zones and initiate a bulk sample for metallurgical testing.

- Financial & Operational Updates (Late 2025)

- Cash Position: Following the late 2024/early 2025 financing rounds (approx. $10M raised), the company is well-funded for the current drill campaigns at both Berenguela and Challacollo.

- Berenguela Update: The updated Mineral Resource Estimate (MRE) is the critical anchor. With 122.5 Moz Ag (M&I) and meaningful copper/manganese credits, the project is approaching "critical mass" for development.

- Challacollo (Chile): While Berenguela steals the headlines, drilling also commenced here in Dec 2025 to test new vein extensions. This provides a "Plan B" asset that the market often overlooks.

- Risks to Watch

- The "Paper" Gain: The 12% rise is largely driven by sentiment around silver prices. If the underlying commodity falters, the stock will retrace.

- Dilution: The company recently issued millions of stock options and RSUs (Dec 2025). While standard for juniors, it adds to the share count.

- Geopolitics: Puno (Peru) has seen social unrest in the past. Maintaining a "social license to operate" is the single biggest operational risk.

- Conclusion

Aftermath Silver's 12.2% surge on Christmas Eve 2025 was a textbook "beta chase." The company has successfully de-risked its flagship asset (100% ownership + growing M&I resource) exactly as silver prices entered a historic parabolic phase.

For investors, AAG represents a leveraged bet on silver staying above $70. If the metal holds, AAG’s expanded resource base makes it a compelling takeover target. However, the reliance on Peruvian stability and sustained commodity fervor means this is a play for those with a high risk tolerance.

Please wait processing your request...

Please wait processing your request...