The "next mid-tier" silver giant is waking up. On December 23, 2025, investors witnessed a massive ~12.4% surge in Sierra Madre Gold & Silver (TSXV: SM), fueled by a perfect storm of strategic acquisitions, massive capital injections, and a historic silver bull run.

While others are watching the charts, smart money is looking at the fundamentals. Here is the deep dive into why Sierra Madre is the retail favorite of the 2025 holiday season.

The Catalyst: Why the December 23rd Spike?

The double-digit jump wasn't a coincidence—it was a reaction to three massive "green flags" that hit the wire in late December:

Source: Kalkine Group

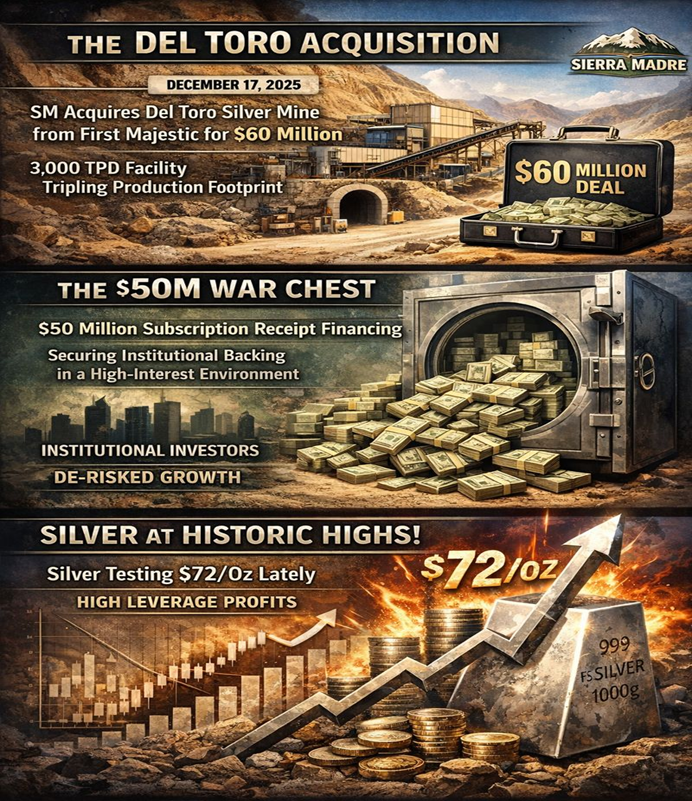

- The Del Toro Acquisition: On Dec 17, 2025, SM announced a definitive agreement to acquire the Del Toro Silver Mine from First Majestic Silver for US$60 million. This isn't just a property; it's a 3,000 tpd facility that could triple SM's production footprint.

- The $50M War Chest: To fund the deal, the company launched a $50 million subscription receipt offering. In a high-interest environment, securing this level of institutional backing is a massive signal of "de-risked" growth.

- Silver at Historic Highs: With silver testing $72/oz lately, Sierra Madre's "High Leverage" model means their profit margins are expanding exponentially faster than the metal price itself.

2025 Business Model: The "Fast-Track" Producer

Sierra Madre has moved away from the "explore and hope" model. Their current strategy is Asset Rehabilitation:

- Brownfield Focus: They buy past-producing mines (La Guitarra, Del Toro) with hundreds of millions in existing infrastructure.

- Infrastructure Advantage: Instead of spending 5 years building a mill, they repair existing ones in 6-12 months.

- Strategic Partnership: First Majestic Silver remains a major shareholder (~44%), providing technical backing and "big brother" credibility.

Latest Financial & Operational Updates

- Commercial Production: Achieved at La Guitarra on Jan 1, 2025.

- Q3 2025 Revenue: $5.5 million, a significant jump from early-year figures.

- Operating Leverage: Q3 saw a 27% increase in Adjusted EBITDA over Q2, proving that as they ramp up tonnage, costs are being diluted.

- Expansion Roadmap:

- Phase 1 (Q2 2026): Ramping La Guitarra to 800 tpd.

- Phase 2 (Q3 2027): Doubling capacity to 1,500 tpd.

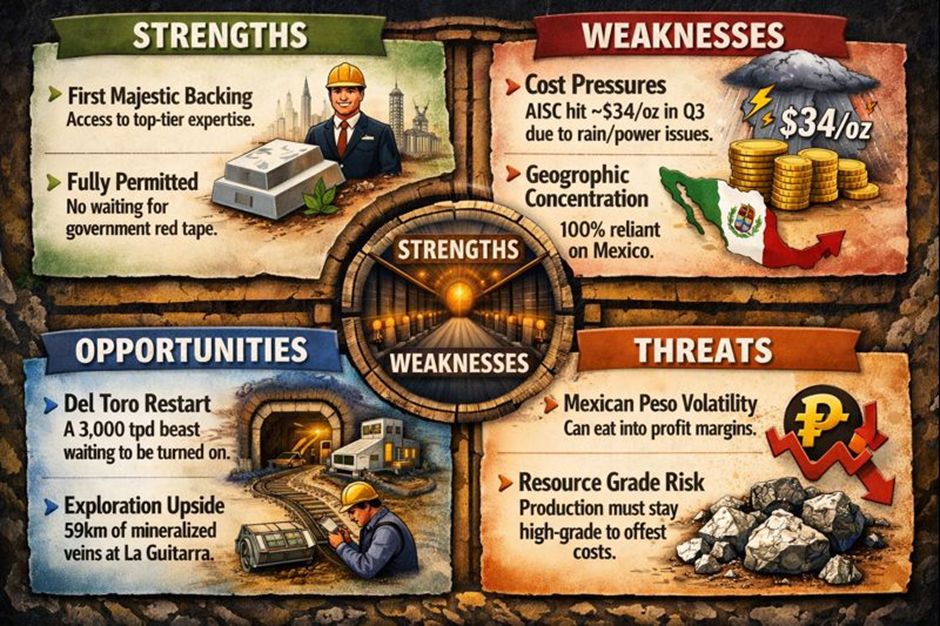

SWOT Analysis: The Brutal Truth

Source: Kalkine Group

Key Risks: The "Retail Warning"

Investing in junior silver producers is not for the faint of heart. Watch out for:

- Execution Risk: Moving from one mine to two (Del Toro) is a massive management challenge.

- Financing Dilution: The $50M raise means more shares on the market, which can cap short-term price gains.

- The "Rainy Season" Factor: Q3 was hampered by power outages in Mexico. While they are installing backup power for 2026, weather remains a wild card.

Conclusion

Sierra Madre is no longer just a "story stock"—it is a revenue-generating producer in the heart of the world’s richest silver belt. The 12% jump on Dec 23 reflects the market pricing in the Del Toro transition and the end of 2025's operational "hiccups." If they hit their 2026 expansion targets, the current valuation may look like a bargain in hindsight.

Source: Trading View, 23 December 2025

Please wait processing your request...

Please wait processing your request...