Is this the "Silver Squeeze" retail has been waiting for? While the rest of the market was sipping eggnog, Santacruz Silver Mining (TSXV: SCZ) delivered a 4.1% gain on December 24, 2025, closing at CAD13.52. This isn't just a holiday fluke—it’s the result of a massive 12-month transformation that has the "Silver Apes" and institutional desk-traders buzzing.

The "Santa Rally" Drivers: Why SCZ is Trending

The Christmas Eve spike was fueled by a "perfect storm" of three late-Q4 catalysts:

Source: Kalkine Group

- The NASDAQ Countdown: On Dec 8, SCZ confirmed the effective date for its share consolidation. This is the final "boss level" before its official NASDAQ listing in early 2026. Retail investors are buying the "uplisting" hype, expecting a massive influx of US liquidity.

- The "Glencore Ghost" is Gone: In September 2025, Santacruz officially finished paying off its $40M debt to mining giant Glencore. The company is now 100% owner of its massive Bolivian cash-flow machine.

- Silver’s Bull Run: With global silver prices hovering near $77/oz, SCZ—a high-beta play—is outperforming the physical metal as investors chase leveraged returns.

2025 Business Model: The "Hybrid" Money Machine

Santacruz isn't just a miner anymore; it's a regional mineral hub.

- The Core: Production from the Zimapán (Mexico) and Bolívar/Porco (Bolivia) mines.

- The Secret Sauce: The San Lucas Group business model. Santacruz acts as a "mini-Glencore" in Bolivia, purchasing and processing high-grade ore from local cooperatives. This keeps their mills at 100% capacity even when their own mines face hiccups.

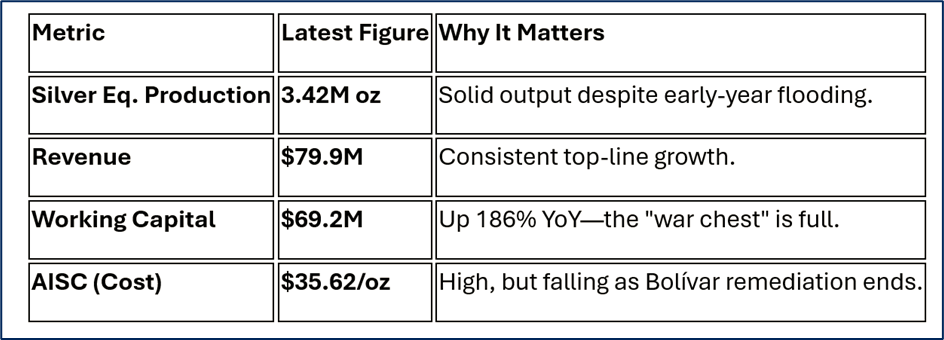

Financial & Operational Snapshot (Q3 2025 Data)

Source: Company Data

SWOT Analysis (The Retail Reality Check)

Source: Kalkine Group

Strengths

- Debt-Free: The Glencore anchor has been cut.

- Polymetallic Hedge: Large exposure to Zinc and Lead provides a safety net if Silver dips.

- NASDAQ Ready: Ready for the big leagues and institutional "FOMO."

Weaknesses

- Cost Creep: All-In Sustaining Costs (AISC) are currently high due to 2025's mine repairs.

- Operational Risk: One flood or labor strike in Bolivia can stall the momentum.

Opportunities

- Soracaya Project: A massive new project moving toward production in 2026.

- Short Squeeze Potential: High short interest earlier in 2025 could lead to a rapid upward spiral as the NASDAQ listing nears.

Threats

- Jurisdictional Risk: Bolivia’s political climate remains "predictably unpredictable."

- Currency Drag: A strong Bolivian Boliviano (BOB) hurts their USD margins.

The "Red Flags" You Shouldn't Ignore

While the 4% gain is sexy, don't ignore the Management Cease Trade Orders (MCTO) that occurred earlier in May 2025. Although resolved, they show that SCZ’s back-office can be slow. Also, keep an eye on the consolidation ratio—while necessary for the NASDAQ, it often leads to short-term volatility as retail holders adjust their positions.

The Verdict: Bullish or Bait?

Santacruz Silver is entering 2026 as a de-risked, debt-free, mid-tier producer with a massive US listing on the horizon. If silver stays above $70, SCZ is a coiled spring. However, it remains a "high-conviction" play—meaning it's not for the faint of heart.

Please wait processing your request...

Please wait processing your request...