The silver market is witnessing a historic "slingshot" effect, and Endeavour Silver Corp. (TSX: EDR) is at the epicenter. On December 30, 2025, the stock climbed ~2.44%, closing at approximately CAD 13.43, outperforming a broader market that has been characterized by late-year volatility.

While many retail investors focus on the price of the metal, the real story for Endeavour lies in its massive operational transformation and a strategic bet on a 2026 supply "bottleneck."

Key Drivers: What Pushed EDR Up on Dec 30?

The ~2.4% gain on the penultimate trading day of 2025 was driven by a convergence of macro-bullishness and company-specific de-risking:

Source: Kalkine Group

- The "Silver Squeeze" 2026 Narrative: Citigroup and other major analysts recently revised silver price targets toward the $100–$110/oz mark for 2026, citing acute physical shortages. EDR, known for its high "silver beta," is the primary vehicle for investors looking to capture this upside.

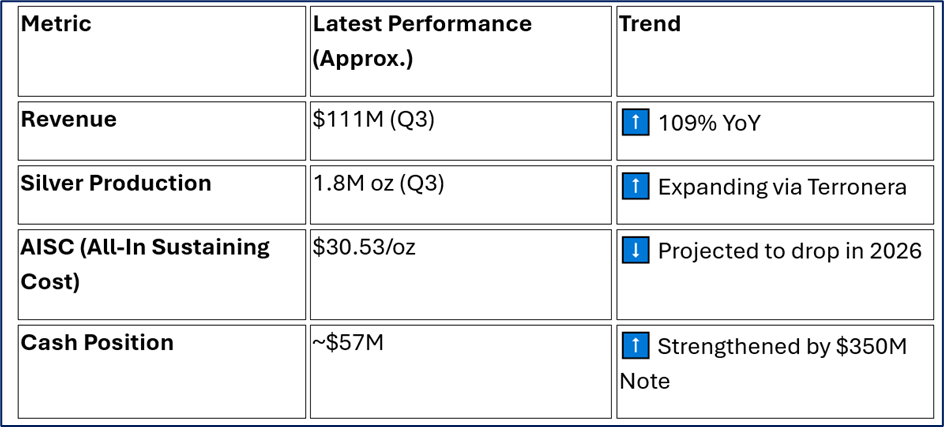

- Terronera Commercialization: The market is finally pricing in the successful ramp-up of the Terronera mine. Having reached commercial production in late 2024, the mine is now operating at 90% capacity, fundamentally shifting Endeavour from a high-cost producer to a high-margin mid-tier.

- Convertible Note Stability: Following the completion of a $350 million convertible debt offering in early December, the "funding risk" has been largely removed. Investors are now focused on growth rather than liquidity concerns.

Latest Business Model: The "30 by 30" Vision

Endeavour Silver has pivoted from a pure-play Mexican miner to a diversified North-South American producer. Its current business model rests on three pillars:

- Organic Production Growth: The goal is to reach 30 million silver-equivalent (AgEq) ounces annual production by 2030.

- Strategic M&A: The May 2025 acquisition of the Minera Kolpa mine in Peru added a third producing asset, diversifying geographical and jurisdictional risk.

- The "Pure Play" Premium: Unlike diversified giants, Endeavour remains one of the few miners where silver accounts for the vast majority of revenue, offering investors direct leverage to the metal’s spot price.

Financial & Operational Updates (Q4 2025 Context)

Source: Company Data

Operational Milestone: The Terronera Project is processing ~2,000 tonnes per day. Management expects this to be the primary engine for free cash flow generation starting in Q1 2026.

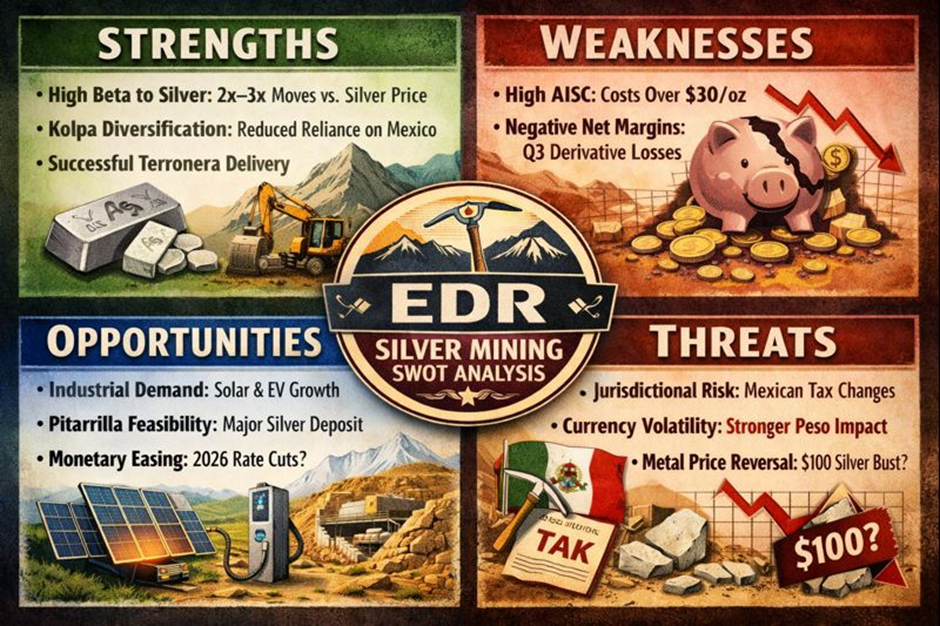

SWOT Analysis (2025/2026 Outlook)

Source: Kalkine Group

Strengths

- High Beta to Silver: EDR typically moves 2x–3x more than the spot price of silver.

- Operational Diversification: The addition of Kolpa (Peru) reduces reliance on Mexican mining laws.

- Management Track Record: Successful delivery of Terronera on schedule.

Weaknesses

- Historically High AISC: Current costs are high, requiring silver to stay above $30/oz to maintain healthy margins.

- Negative Net Margins: Q3 showed a loss due to non-cash derivative valuations, which can spook retail investors.

Opportunities

- Industrial Demand: Massive silver requirements for solar energy and EV infrastructure.

- Pitarrilla Feasibility: Advancing one of the world’s largest undeveloped silver deposits.

- Monetary Easing: Potential 2026 interest rate cuts could propel precious metals to new ATHs.

Threats

- Jurisdictional Risk: Increased mining taxes and regulatory changes in Mexico.

- Currency Volatility: A strengthening Mexican Peso (MXN) increases local operating costs.

- Metal Price Reversal: If the $100/oz silver thesis fails, high-cost producers are hit hardest.

Critical Risks to Watch

- Derivative Exposure: Endeavour often uses hedging and derivative contracts. While these protect against downside, they can cause "paper losses" that impact EPS during rapid price spikes.

- Liquidity: Despite the recent $350M raise, the company’s capital-intensive growth strategy requires constant monitoring of the cash runway.

Conclusion

Endeavour Silver is no longer just a "speculative junior." With Terronera firing on all cylinders and the Kolpa integration complete, the company has successfully transitioned into a mid-tier producer. The stock's performance on December 30 reflects a market that is looking past historical losses and toward a 2026 characterized by supply deficits and potential triple-digit silver prices.

Please wait processing your request...

Please wait processing your request...