The silver market is screaming, and Vizsla Silver Corp. (TSX: VZLA) is riding the lightning. While the broader markets catch their breath, Vizsla shares climbed ~2.2% on December 30, 2025, capping off a historic year for the "white metal."

As global silver inventories plummet to decade lows and China tightens its grip on exports, retail investors are pivoting to high-grade developers. Here is the deep dive into why Vizsla Silver is the name on every analyst's lips as we head into 2026.

The Catalyst: Why Dec 30 Was Bullish

The 2.2% move wasn't a fluke; it was a reaction to a "Perfect Storm" of macro and micro drivers:

Source: Kalkine Group

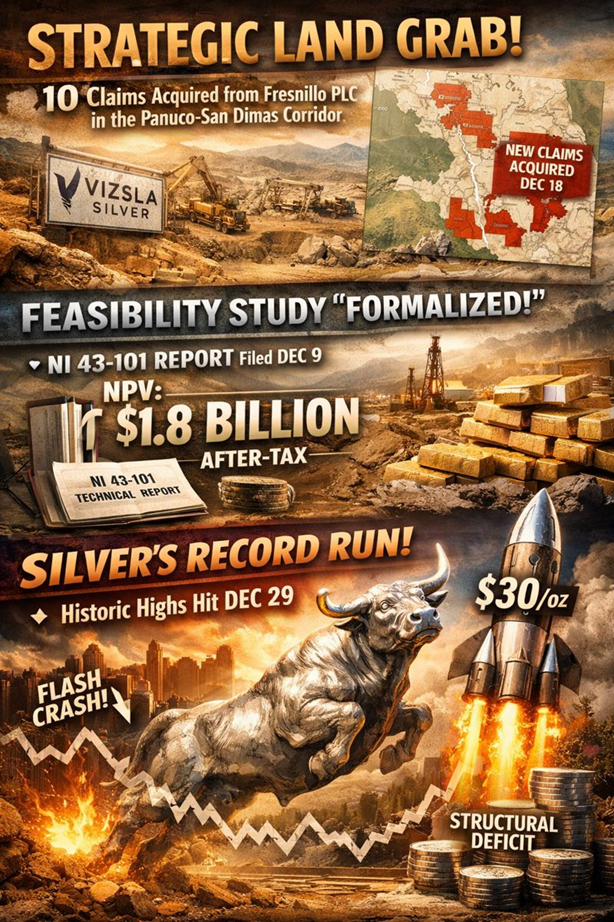

- Strategic Land Grab: Just days ago (Dec 18), Vizsla announced a massive acquisition of 10 strategic claims from mining giant Fresnillo PLC, expanding its footprint in the legendary Panuco-San Dimas corridor.

- Feasibility Study "Formalized": The filing of the official NI 43-101 Technical Report on Dec 9 confirmed what the market suspected: Panuco is an absolute beast with an after-tax NPV of US$1.8 Billion.

- Silver’s Record Run: Silver prices touched historic highs on Dec 29. Despite a brief "flash crash" due to margin hikes, the structural deficit remains, and Vizsla—as a primary silver play—is a high-beta beneficiary.

Latest Business Model: From Explorer to Tier-1 Producer

Vizsla has shed its "junior explorer" skin. Its 2025 business model is now a Dual-Track Strategy:

- Track 1: Rapid Development: Fast-tracking the Copala and Napoleon deposits toward a construction decision.

- Track 2: Aggressive Expansion: Using its US$300M convertible note war chest to find "Project 2" while drilling 25,000+ meters annually to grow the existing 222 Moz AgEq resource.

Unlike many peers who rely on "hope," Vizsla is now a fully funded developer with a clear path to first silver in H2 2027.

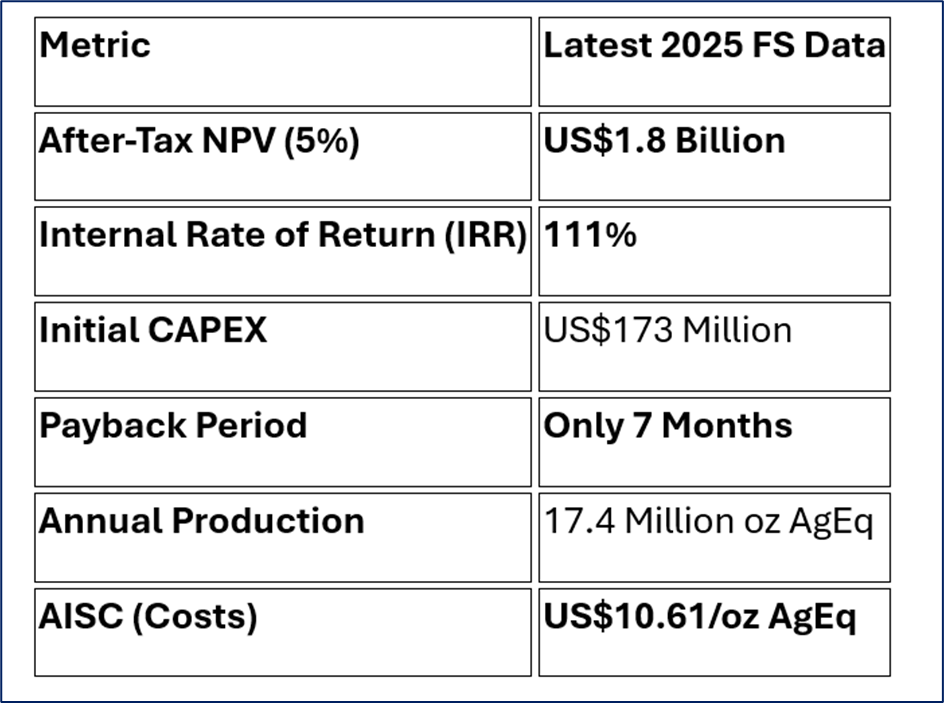

2025 Financial & Operational Power-Up

The numbers coming out of the November Feasibility Study (FS) are, quite frankly, industry-leading:

Source: Company Data

Financial Health: The company closed a US$300 Million convertible note offering in late 2025. While this introduced debt to a previously debt-free balance sheet, it provides the "strike capital" needed to build the mine without constant equity dilution.

SWOT Analysis: The Hard Truth

Source: Kalkine Group

Strengths

- Grade is King: Average reserve grades of 337 g/t AgEq at Copala.

- Tier-1 Location: Located in Sinaloa, Mexico, surrounded by giants like Fresnillo and First Majestic.

- Exceptional Economics: A 111% IRR is virtually unheard of in the current mining landscape.

Weaknesses

- Pre-Revenue Status: Still roughly 18-24 months away from steady cash flow.

- Debt Load: The new US$300M in convertible notes increases financial leverage.

Opportunities

- The "Silver Squeeze": If silver hits the projected US$75–$80/oz in 2026, Vizsla’s NPV could double.

- M&A Target: Its high-grade, single-asset profile makes it a "tasty snack" for a mid-tier or major producer.

Threats

- Jurisdictional Risk: Mexico’s shifting mining laws and permitting environment.

- Commodity Volatility: A sudden drop in silver prices could delay the construction decision.

The Risks: What Could Go Wrong?

Investors shouldn't ignore the "overbought" signals. As of late December, the RSI (Relative Strength Index) was hovering near 76, suggesting the stock may need a healthy consolidation. Furthermore, as a developer, any delay in permitting or an increase in construction costs (inflation) could dampen the current enthusiasm.

Conclusion: The New Silver Standard?

Vizsla Silver is no longer a "drill-and-hope" story. By securing US$300M in funding, filing a stellar Feasibility Study, and swallowing up strategic land from Fresnillo, the company has positioned itself as the premier silver development vehicle of 2026. If the silver deficit continues as predicted, VZLA isn't just a stock—it’s a high-octane bet on the future of the energy transition.

Please wait processing your request...

Please wait processing your request...