The Snapshot: December 22, 2025

Vizsla Silver Corp. (TSX: VZLA) is no longer flying under the radar. On December 22, 2025, the stock surged approximately 7.7%, hitting a new 52-week high of CAD 7.70. This wasn't a random fluctuation; it was a calculated market reaction to a convergence of macro tailwinds and aggressive company-specific execution.

Investors are witnessing a "de-risking" event for Vizsla, transitioning it from a speculative explorer to a prime development candidate in a silver bull market that just shattered historical records.

Key Drivers: Why the Stock Jumped

The ~7.7% move was fueled by three massive catalysts colliding on the same day:

Source: Kalkine Group

1. The Macro Super-Cycle: Silver Breaks $69/oz

The biggest driver was the commodity itself. On Dec 22, global spot silver prices broke the psychological $69/oz barrier (hitting record highs in multiple currencies).

- The Cause: Cooling US inflation data released earlier in the week solidified expectations for further Federal Reserve rate cuts.

- The Effect: Industrial demand (Solar/PV and AI hardware) is colliding with a 5-year structural supply deficit. As a high-beta play on silver, VZLA acts as a leveraged instrument—when silver moves 1%, high-quality developers often move 3-5%.

2. The Strategic "Coup": Fresnillo Land Acquisition

Investors are still pricing in the massive news from late last week (Dec 18) which is now being fully digested by institutional capital. Vizsla acquired 10 strategic mining claims (2,378 hectares) from Fresnillo plc—the world’s largest primary silver producer.

- Why it Matters: These claims surround Vizsla’s flagship Panuco project. This isn't just "more land"; it’s a defensive moat and an offensive resource expansion. It consolidates the entire district, effectively blocking competitors and securing potential vein extensions that Fresnillo held for decades.

3. Wall Street Validation: Analyst Initiation

On December 22, Cantor Fitzgerald initiated coverage on Vizsla Silver with a "Buy" rating.

- The Signal: When a major firm initiates coverage after a stock has already run up, it signals they believe the rally has legs. This follows recent target upgrades from CIBC and National Bankshares, creating a "consensus upgrades" cycle that attracts algorithmic buying.

Strategic Analysis: Business Model & Updates

Current Business Model: Vizsla is pivoting from "Drill & Discover" to "De-risk & Build." The model is focused entirely on the Panuco-Copala Silver-Gold District in Sinaloa, Mexico. Unlike prospect generators, Vizsla owns the asset 100% and is fast-tracking it toward production.

Latest Operational & Financial Updates (Q4 2025):

- Feasibility Study (Nov 2025): The company dropped a bombshell study showing an After-Tax NPV (5%) of US$1.8 Billion and an IRR of 111%.

- Payback Period: astonishingly low at 7 months. Most mines take 2-4 years to pay back capital; 7 months is world-class.

- Cash Position: Vizsla sits on a fortress balance sheet with ~$203 million in cash (following recent financings). They are fully funded for early development, removing the immediate fear of dilutive equity raises that plagues the junior mining sector.

- Production Timeline: First silver pour is targeted for 2027, positioning them to sell into what analysts forecast will be a peak supply-deficit market.

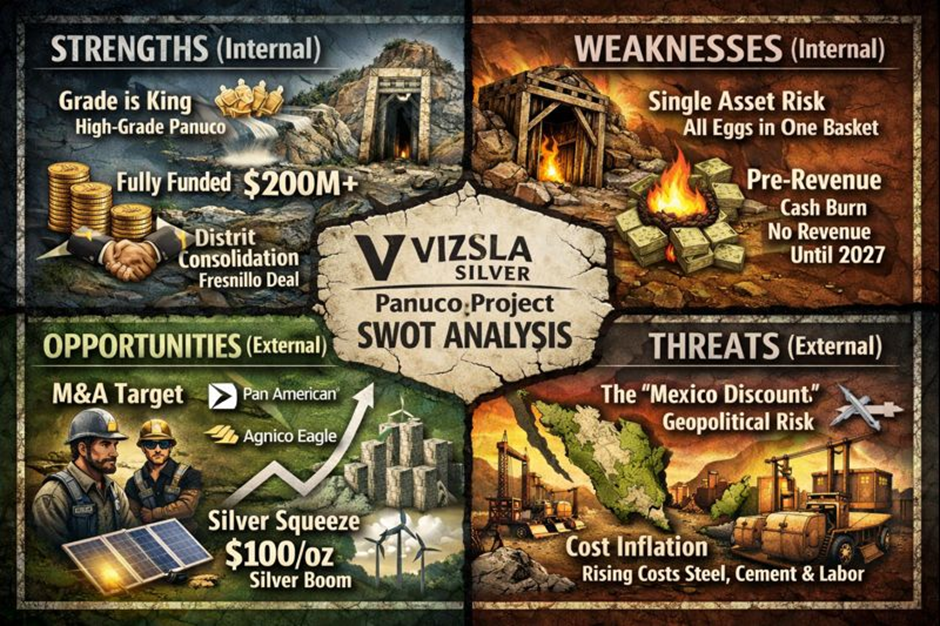

SWOT Analysis

Source: Kalkine Group

Strengths (Internal)

- Grade is King: Panuco is one of the highest-grade undeveloped silver primary assets globally. High grades provide margin protection if silver prices dip.

- Fully Funded: With >$200M in the bank, they don't need to beg the market for cash.

- District Consolidation: The Fresnillo deal cements their dominance in the region.

Weaknesses (Internal)

- Single Asset Risk: The company’s valuation is tied almost entirely to Panuco. Any technical failure there is catastrophic.

- Pre-Revenue: Despite high cash reserves, they are burning cash (OPEX) monthly with no commercial revenue until 2027.

Opportunities (External)

- M&A Target: With major miners (like Pan American or Agnico Eagle) running out of reserves, VZLA is a prime takeover target.

- Silver Squeeze: If industrial demand from the Green Energy transition continues to outpace mining supply, silver could target $100/oz, exponentially increasing VZLA's NPV.

Threats (External)

- The "Mexico Discount": Geopolitical risk in Mexico remains the biggest overhang. Concerns regarding mining law reforms, security in Sinaloa, or permitting delays could crush the stock multiple regardless of geology.

- Cost Inflation: Building a mine in 2026-2027 means battling inflated costs for steel, cement, and labor.

Risks to Watch

While the chart looks parabolic, caution is warranted:

- Permitting Delays: The timeline to 2027 assumes smooth sailing with Mexican environmental agencies (SEMARNAT). Delays here are common.

- Silver Volatility: If silver retraces back to $50, VZLA will correct sharply.

- Security: Sinaloa has a history of cartels activity. While Panuco has been safe, perception effects institutional investment.

Conclusion: The "Unicorn" of Silver?

Vizsla Silver's ~7.7% jump on December 22, 2025, is a rational repricing of an asset that is rapidly becoming a "unicorn" in the mining space: a high-grade, fully-funded, large-scale silver project in a bull market. The market is waking up to the fact that Vizsla isn't just finding silver; they are arguably building the next major primary silver mine in the Americas.

For investors, the thesis is clear: You are paying for execution and leverage to the silver price. The Fresnillo deal was the checkmate move for district control. Now, the clock is ticking toward 2027 production.

Source: Trading View, 22 December 2025

Please wait processing your request...

Please wait processing your request...