Utilities can’t pause maintenance. Stella-Jones powers North America’s grid with steady cash flow and dividends. Is TSX: SJ a buy in 2026?

As the S&P/TSX Composite Index grapples with volatility and a shifting Canada economy, investors are scouring the Toronto Stock Exchange for recession-proof stocks and high-yield dividend aristocrats. With the global energy transition demanding massive grid upgrades, the demand for utility poles and railway infrastructure is skyrocketing.

In this deep-dive analysis for January 2026, we break down why this infrastructure giant is trending on Twitter, LinkedIn, and Investing.com, and whether its current valuation makes it a "buy the dip" opportunity or a "hold" for the long haul.

Key Takeaways: January 2026 Market Snapshot

- Infrastructure Surge: Stella-Jones is capitalizing on the North American grid modernization, with utility pole sales hitting $480 million in the latest quarter (Source: Stella-Jones Q3 Report).

- Dividend Reliability: The board declared a $0.31 quarterly dividend in late 2025, supported by a robust 18.36% Return on Equity (ROE).

- Stock Momentum: Shares hit a 52-week high of $91.59 earlier this month, currently trading near $88.10 with a "Moderate Buy" consensus.

- Macro Resilience: Amidst a cooling Canada GDP (0.1% growth), Stella-Jones remains a defensive powerhouse due to its essential service nature.

Why is the Canada Economy and TSX Composite Facing a "Structural Reset" in January 2026?

Are you watching the TSX Composite Index closely this month? As of January 29, 2026, the index fell to 32,757 points, losing 1.26% in a single session as technology stocks tumbled (Source: Trading Economics). The Bank of Canada recently held interest rates steady, but Governor Tiff Macklem has warned of "unusual potential for new economic shocks" stemming from global trade dynamics and tariff uncertainties. While the CAD (Canadian Dollar) is showing resilience at 73.89 cents US, the manufacturing PMI has dipped to 48.8, signaling a contraction.

However, in this "high-interest, low-growth" environment, why are infrastructure stocks like Stella-Jones outperforming? The answer lies in the global energy nexus. As AI data centers and EV charging networks demand more power, the physical grid—the poles and ties—must be replaced. Stella-Jones isn't just a lumber company; it is the backbone of the North American energy transition.

Is Stella-Jones (SJ.TO) a Bullish or Bearish Play for Short and Long-Term Investors?

Short-Term Analysis (3-6 Months): Neutral to Bullish

Is the momentum sustainable? Currently, Stella-Jones displays a classic "Buy on the dip" profile. While technical signals like the 3-month MACD show some short-term exhaustion after hitting recent highs, the stock remains above its 200-day moving average of $82.03 (Source: MarketBeat). Retail sentiment is catchy: "Let the trend be your friend." With a share buyback program (NCIB) active until November 2026, the company is effectively putting a floor under the share price.

Long-Term Analysis (1-3 Years): Highly Bullish

Why does the long-term outlook look so golden? It’s about replacement cycles. Millions of utility poles across the U.S. and Canada are reaching their 50-year expiration date. Stella-Jones dominates this monopoly-like niche. Their recent acquisition of Brooks (crossarm manufacturer) further solidifies their vertical integration. Analysts note that even if a recession hits, utilities cannot stop maintaining the grid without risking catastrophic failure. This makes SJ.TO a "forever hold" for many retail portfolios.

What Are the Latest Financial and Operational Drivers Behind the Surge?

- Sales Growth: Reported $958 million in quarterly sales, a 5% increase year-over-year, driven by organic volume growth in utility poles (Source: Stella-Jones Press Release).

- Profitability: Net income reached $88 million ($1.59 EPS), beating analyst expectations and showcasing strong margin management despite rising input costs.

- Strategic M&A: The company is aggressively pursuing acquisitions to expand its footprint in the Logs & Lumber and Pressure-treated wood segments.

- Dividend Update: A dividend of $0.31 per share was paid in December 2025, with expectations for an increase in the mid-2026 cycle (Source: Company filings).

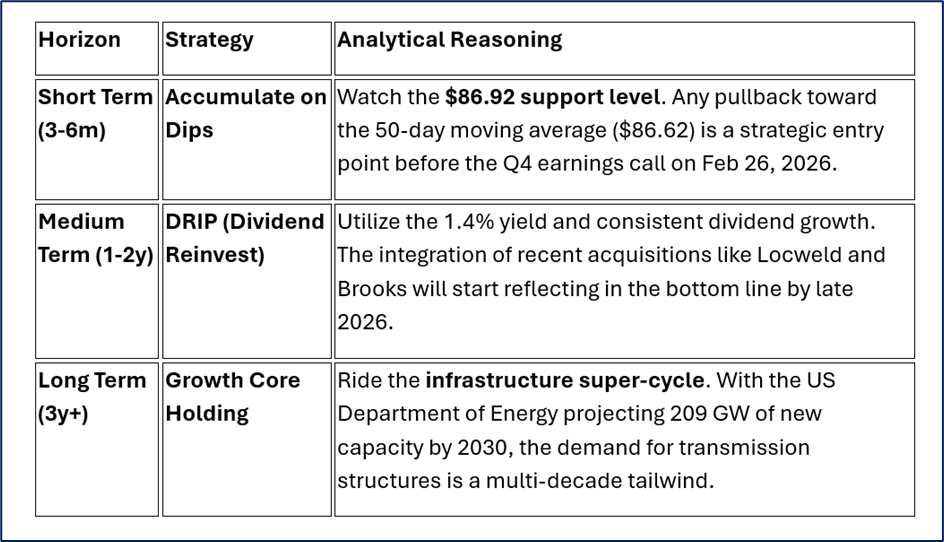

What Action Should Investors Take Now? Forward-Looking Strategies

Source: Market Data

What Do the Top Analysts Predict for Stella-Jones in 2026?

The "Smart Money" is leaning toward a moderate buy. Here are the latest ratings and CAD price targets:

- Desjardins: $102.00 – Buy (Source: Dec 2025 Report)

- Raymond James: $100.00 – Outperform (Source: Nov 2025 Report)

- TD Securities: $97.00 – Buy (Source: Nov 2025 Report)

- CIBC: $89.00 – Hold (Source: Nov 2025 Report)

- RBC Capital: $87.00 – Sector Perform (Source: Oct 2025 Report)

Consensus Price Target: $95.71 (Representing a ~8-9% upside from current levels).

Latest FAQ for Investors

Q: Is Stella-Jones a good hedge against inflation?

A: Yes. Because they operate under long-term contracts with utilities and railroads, they can often pass through cost increases, maintaining their 19.6% gross profit margin.

Q: When is the next earnings report?

A: Mark your calendars for February 26, 2026, for the Q4 2025 results.

Q: What is the biggest risk to the stock?

A: A shift toward steel or composite poles could threaten long-term wood demand, though wood remains the most cost-effective and environmentally friendly option currently.

Investment Conclusion: Buy, Sell, or Hold?

Analytical Verdict: BUY / ACCUMULATE.

For investors seeking a "Sleep Well at Night" (SWAN) stock in the TSX Materials sector, Stella-Jones is a top contender. It offers the rare trifecta of value (P/E ~14.4x), growth (Infrastructure tailwinds), and income (Reliable dividends). While the TSX remains choppy, SJ.TO’s mission-critical business model makes it a viral favorite for 2026.

Please wait processing your request...

Please wait processing your request...