The 2026 Strait of Hormuz crisis, triggered by the ongoing Iran war, has rapidly evolved into the largest energy supply disruption in modern history, with profound implications for global markets, geopolitics, and economic stability. What began as a regional military escalation has now cascaded into a full-scale systemic shock affecting energy flows, trade, inflation, and global growth.

This comprehensive analysis breaks down the latest developments (as of April 2, 2026), the supply-demand dynamics, country-level impacts, and short-, medium-, and long-term outlooks for energy, commodities, and financial markets.

Source: Kalkine Group

Latest Iran War & Hormuz Crisis Updates (April 2026)

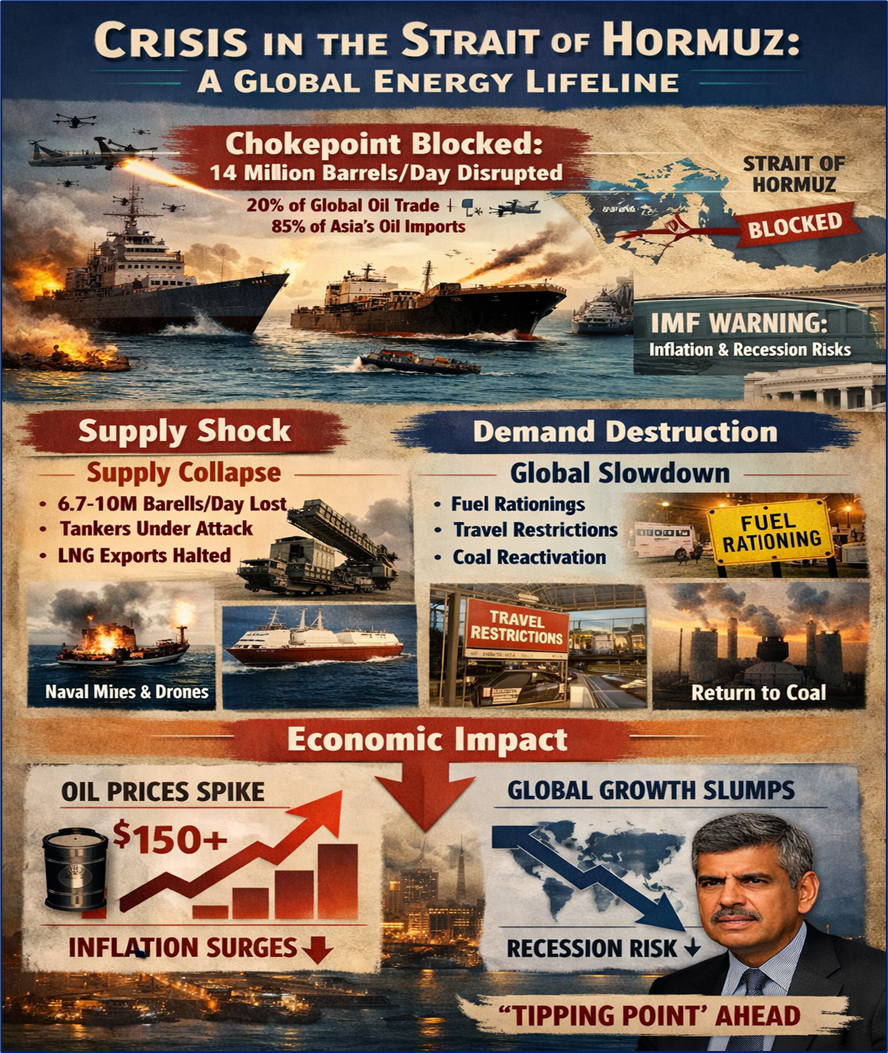

- The Strait of Hormuz remains effectively blocked, halting tanker traffic and disrupting ~20–30% of global oil flows

- Oil supply disruption is estimated at ~14 million barrels/day, exceeding COVID-era shocks

- The IMF warns of worsening global economic outlook, with inflation and recession risks rising

- Global trade growth is expected to collapse from ~4.7% to as low as 1.5–2.5%

- US military operations to reopen the strait are ongoing, while Iran continues asymmetric attacks on shipping

- Economist Mohamed El-Erian warns of an imminent “tipping point” in supply disruption and inflation

The situation remains highly volatile, with ceasefire claims disputed and geopolitical escalation risks still elevated.

Why the Strait of Hormuz Matters: A Global Energy Lifeline

The Strait of Hormuz is the most critical energy chokepoint in the world:

- Handles ~20–25% of global oil trade

- Carries significant LNG flows (20% globally)

- Supplies Asia with ~85%+ of its imported oil via this route

This concentration risk explains why its disruption has triggered a global macro shock rather than a regional crisis.

Supply Shock vs Demand Destruction: The Core Economic Dynamic

- Supply Collapse (Primary Driver)

- Oil production losses: 6.7–10 million barrels/day+

- LNG exports halted from Qatar and others

- Shipping halted due to:

- Missile/drone threats

- Naval mines

- Insurance cost spikes

This is widely considered the largest oil supply shock ever recorded

- Demand Destruction (Secondary Response)

Governments globally are responding with:

- Fuel rationing

- Reduced working hours

- Travel restrictions

- Coal reactivation

This creates a classic stagflation scenario:

- Supply shock → higher prices

- Demand suppression → slower growth

Oil & Energy Price Outlook

Current Situation

- Oil surged past $100–$126 per barrel

- Analysts warn of $150–$200 scenarios if disruption persists

Forward Price Scenarios

Source: Kalkine Group Analysis

Global Economic Impact

Source: Kalkine Group

Inflation Surge

- Energy-driven inflation spreading globally

- Food prices rising due to fertilizer shortages

- Freight and insurance costs surging

Growth Slowdown

- IMF: global outlook deteriorating sharply

- UN: trade slowdown to near stagnation

- Oxford Economics: risk of global recession scenario

Financial Markets

- Equities under pressure

- Bond yields volatile

- Capital flight from emerging markets

Impact by Region

United States

- Relatively insulated due to domestic oil production

- However:

- Inflation rising

- Equity markets falling (~20% downside risk)

- Policy stance: pro-fossil fuel expansion

Europe

- Facing a second energy crisis after Ukraine war

- LNG shortages (especially from Qatar)

- Policy dilemma:

- Renewables vs coal fallback

Middle East (Gulf States)

- Most directly impacted:

- GDP decline >8% in 2026

- Export revenues disrupted

- Food and water supply crisis emerging

Asia (Biggest Loser)

- Heavily dependent on Hormuz flows

- Severe:

- Fuel shortages

- Industrial disruptions

- Countries like India, Japan, South Korea under pressure

BRICS Nations

- China: Supply risk via Iranian oil dependency

- India: Managing via reserves but exposed

- Russia: Beneficiary via higher oil prices

- Brazil: Less impacted due to domestic production

- South Africa: Vulnerable to import costs

Commodity Market Impact

Energy

- Oil, gas → sharp spike

- LNG → extreme volatility

Metals

- Aluminum prices rising due to Gulf production disruption

Agriculture

- Fertilizer shortages (urea, ammonia)

- Food inflation rising globally

Other Strategic Commodities

- Helium, chemicals, shipping fuels disrupted

- Supply chain ripple effects expanding

Supply Chain Shock Beyond Oil

The crisis is not just about oil:

- Shipping routes disrupted

- Air travel halted in Gulf

- Insurance premiums skyrocketing

- Global logistics bottlenecks emerging

This mirrors:

- COVID supply shocks

- Ukraine war commodity disruption

But is more concentrated and immediate

What Economists & Strategists Are Saying

Mohamed El-Erian

- Warning of “tipping point”

- Risk of:

- Supply shortages (not just price spikes)

- Global recession probability rising

IMF

- War is “dimming global economic outlook”

- Key risks:

- Inflation

- Debt stress

- Food insecurity

UN Trade Agency

- Crisis spreading from energy → trade → financial systems

- Warning of systemic global slowdown

Energy Analysts

- Calling it:

- “Largest oil disruption ever”

- “1970s crisis-level shock”

Short, Medium, and Long-Term Energy Outlook

Short-Term (0–3 Months)

- Extreme volatility

- Oil prices spike

- Emergency policy responses:

- Strategic reserves release

- Fuel subsidies

- Demand reduction

Medium-Term (3–12 Months)

- Supply re-routing attempts

- Partial normalization if conflict de-escalates

- Persistent:

- High energy prices

- Inflation

- Renewables gain strategic importance

Long-Term (1–5 Years)

- Structural shifts:

- Energy Security > Cost Efficiency

- Countries diversify supply chains

- Accelerated Energy Transition

- Renewables seen as security hedge

- New Trade Routes & Alliances

- Reduced dependence on chokepoints

The “Energy Paradox”

One of the most important emerging themes:

- Fossil fuels → cause crisis vulnerability

- But → still required to stabilize markets

This creates a paradox:

- Short-term: more fossil investment

- Long-term: faster renewable adoption

Geopolitical Power Shifts

United States

- Leveraging crisis to:

- Expand oil exports

- Strengthen geopolitical influence

Iran

- Demonstrating:

- Asymmetric warfare capability

- Ability to disrupt global systems

China & Asia

- Forced into:

- Energy diversification

- Strategic reserves expansion

Europe

- Accelerating:

- Energy independence

- Renewable transition

Key Risks Ahead

- Prolonged Blockade

- Oil > $150–200

- Global recession

- Regional Escalation

- Wider Middle East conflict

- Supply collapse

- Financial Crisis Spillover

- Emerging market defaults

- Currency crises

- Food Crisis

- Fertilizer shortages → crop yield decline

- Rising hunger in developing economies

Investment & Market Outlook

Winners

- Oil producers (US, Russia)

- Energy infrastructure companies

- Defense sector

Losers

- Energy importers (Asia, Europe)

- Airlines, logistics

- Emerging markets

Key Themes

- Inflation hedge assets outperform

- Commodities remain volatile

- Energy equities structurally supported

Final Conclusion: A Structural Turning Point for the Global Economy

The 2026 Strait of Hormuz crisis is not a temporary geopolitical disturbance — it is a structural inflection point for the global economic and energy system.

At its core, this crisis has exposed a critical fragility: the world remains deeply dependent on a narrow set of geographic chokepoints for its energy lifelines. The disruption of the Strait of Hormuz has demonstrated how quickly localized conflict can escalate into a global economic shock with cascading second-order effects — from inflation and trade collapse to financial instability and food insecurity.

Three defining conclusions emerge:

- Energy security is now the top geopolitical priority

Nations are shifting from cost-optimization to resilience, accelerating diversification of supply sources and transport routes. - The era of cheap and stable energy is over

Volatility will remain elevated as geopolitical risk becomes a permanent feature of commodity markets. - The global energy transition will accelerate — but unevenly

While renewables gain urgency, fossil fuels will paradoxically remain central in the short term, reinforcing the “energy paradox.”

The biggest unknown remains the trajectory of the Iran War 2026:

- A rapid de-escalation could stabilize markets and avoid a deep global recession

- A prolonged or escalating conflict could trigger a multi-year stagflationary cycle, reshaping global trade, capital flows, and geopolitical alliances

Ultimately, this crisis may be remembered as the moment the world fully transitioned into a new era of geopolitically driven economics, where energy, security, and financial stability are inseparably linked.

Frequently Asked Questions (FAQs)

Please wait processing your request...

Please wait processing your request...