Key Takeaways – January 2026

- Historic CA$10 Special Dividend: Strathcona returned CA$10.00 per share to investors in December 2025 following major asset divestments—one of the largest capital returns in recent TSX energy history.

- Pure-Play Heavy Oil Transformation: The exit from Montney assets completes Strathcona’s pivot to a focused heavy oil producer with long-life thermal assets in Cold Lake and Lloydminster.

- Aggressive Growth Vision: Management targets 200,000 barrels/day by 2031 (10% CAGR), with an aspirational upside case of 300,000 barrels/day longer term.

- Balance Sheet Reset: US$500M in senior notes redeemed and a CA$3.49B credit facility secured—lowering the weighted average interest rate for 2026 and beyond.

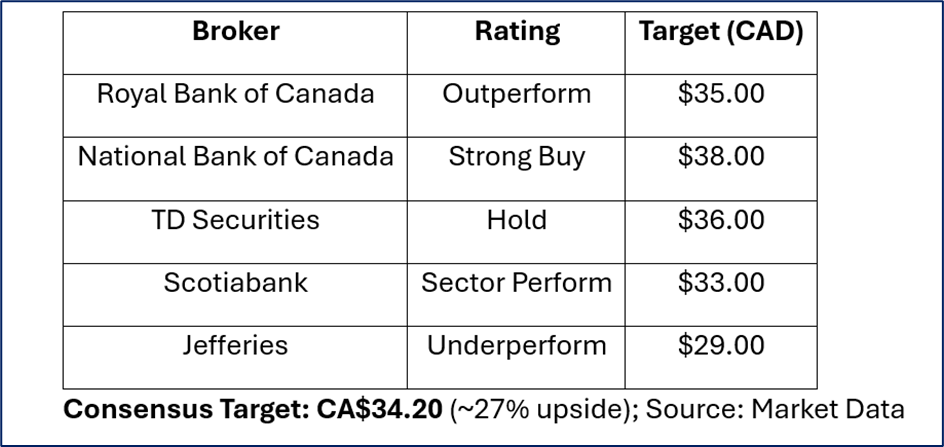

- Split Analyst Outlook: Royal Bank of Canada and National Bank of Canada remain bullish, while others temper expectations amid softer WTI forecasts.

Is Strathcona Resources (TSX: SCR) a Top Energy Stock to Buy in 2026?

As January 2026 unfolds, the Canadian energy sector is undergoing a structural reset—and Strathcona Resources sits right at the center of it. With investors rotating back into cash-generative TSX energy stocks, SCR’s transformation into a low-cost, pure-play heavy oil producer has become impossible to ignore.

The headline CA$10.00 special dividend grabbed attention—but the deeper story is strategy. With WTI crude oil forecasts hovering in the mid-US$50s, Strathcona’s ultra-low breakeven costs and massive 2P reserves offer downside protection few peers can match.

Against a volatile CAD backdrop and a cautious TSX Composite, SCR increasingly looks like a value investor’s energy compounder, not a one-off dividend trade.

Macro Forces Shaping SCR Stock in 2026

Global Energy Crosscurrents

The oil market in 2026 is defined by a tug-of-war between disciplined OPEC+ supply and renewed heavy crude competition.

- Venezuela Re-Entry Risk: U.S. policy shifts aimed at reviving Venezuelan output directly pressure Western Canada Select (WCS) differentials.

- Canadian Policy Headwinds: Carbon pricing under the TIER system rises toward CA$130/tonne, but federal-provincial MOUs may accelerate pipeline approvals.

- Currency Tailwind: A weaker CAD (≈0.72–0.74 USD) boosts margins for exporters like Strathcona, which sells oil in USD while paying costs in CAD.

Meanwhile, energy has lagged U.S. tech flows, and SCR’s ~17% underperformance year-over-year largely reflects its post-dividend price reset—not deteriorating fundamentals.

How Does Strathcona Compare With Canadian Energy Peers?

Strathcona’s model differs sharply from diversified majors like Cenovus Energy and Canadian Natural Resources.

Peer Snapshot (2026E)

- Strathcona (SCR): ~125,000 bbls/day | ~5.3x P/E | 100% heavy oil

- Peers (Whitecap/Baytex): More light oil exposure, but structurally higher costs

Why SCR Stands Out

- ~6× the sub-US$50 WTI breakeven inventory of its median peer

- Targeting growth, while many seniors focus on buybacks and maintenance

- Ownership of the Hamlin Rail Terminal bypasses pipeline bottlenecks and improves netbacks

This combination gives SCR a rare blend of growth, resilience, and logistics control.

SCR Stock Outlook: Short, Medium & Long Term

Short Term (0–6 Months): Neutral / Range-Bound

Markets are still digesting the special dividend. Expect consolidation ahead of Q4 2025 earnings (March 2026), with attention on the Vawn Thermal Project ramp-up.

Medium Term (1–3 Years): Bullish

- Production growth accelerates toward the 2031 target

- LNG-driven gas demand supports pricing while hedges protect margins

- Carbon capture initiatives and west-coast pipeline momentum re-rate heavy oil assets

Long Term (5+ Years): Strongly Bullish

With a 24-year Reserve Life Index, SCR is effectively a long-duration asset on “hard-to-replace” heavy crude demand—particularly asphalt and industrial distillates.

Bull, Bear & Neutral Cases for Strathcona Resources

Bull Case – “The Heavy Oil King”

Low costs, long reserve life, and shareholder-first capital allocation make SCR a standout if global heavy crude demand remains intact.

Bear Case – “Growth vs. Leverage”

A sustained US$45 WTI environment could pressure cash flow and test the expanded credit facility amid aggressive growth spend.

Neutral Case – “Wait for Confirmation”

Some investors are waiting for April 2026 AGM clarity on capital discipline under shifting U.S. energy policy.

Latest Analyst Ratings & Price Targets (January 2026)

Final Verdict: Buy, Sell, or Hold SCR Stock in 2026?

Verdict: STRONG BUY (Long-Term Growth + Income)

Strathcona Resources has evolved from a special-situations trade into a disciplined, scalable heavy oil compounder. At roughly 5× earnings, with a covered dividend and double-digit production growth runway, the valuation simply doesn’t reflect the strategic reset.

For investors seeking exposure to the next phase of Canadian energy—leaner, tougher, and cash-rich—SCR earns a place as a core TSX holding in 2026.

Please wait processing your request...

Please wait processing your request...