The TSX may have been winding down for the holidays, but Strathcona Resources (TSX: SCR) was busy rewriting its balance sheet. On December 24, 2025, while most of the sector drifted, SCR shares edged up +0.52% to close at CAD 29.15. While that number looks modest, it hides a massive technical story: the stock had just "gapped down" the day prior due to a massive $10.00 per share special distribution.

Stripping away the accounting noise, Strathcona is emerging as North America's leanest, "pure-play" heavy oil powerhouse. Here is the analytical breakdown of why the retail crowd is buzzing and why the "Smart Money" is watching SCR.

The Christmas Catalyst: Why SCR is Decoupling

The primary driver for the Christmas Eve resilience was the successful execution of the company’s Plan of Arrangement. On December 22, Strathcona confirmed the payment of a staggering $10.00 per share special distribution (totaling ~$2.14 billion).

Investors who held the stock through the record date essentially received a massive cash windfall, and the 0.52% gain on the 24th indicates that buyers are already stepping back in to "buy the dip" of the newly adjusted, leaner share price.

Key Drivers on Dec 24, 2025:

Source: Kalkine Group

- De-Leveraging Victory: Pro forma for the distribution and the redemption of US$500M in Senior Notes, Strathcona expects to end 2025 with just $2.1 billion in debt.

- Liquidity Surge: The company closed an upsized $3.49 billion credit facility, providing $1.4 billion in immediate liquidity.

- Portfolio Purge: Management confirmed it dumped its entire marketable security portfolio for $1.39 billion in cash, locking in a $101M gain since September.

Latest Business Model: The "Pure-Play" Pivot

Strathcona has officially exited the "diversified" game. By selling its Montney segment for billions earlier in the year, the company has transitioned into a concentrated heavy oil specialist.

The Strategy: Focus on long-life, low-decline thermal assets (SAGD) that require minimal maintenance capital compared to traditional shale.

- No Refineries, No Mines: Unlike Suncor or CNRL, SCR avoids the high-cost overhead of mining and refining, focusing strictly on upstream extraction and midstream logistics (via the recently acquired Hardisty Rail Terminal).

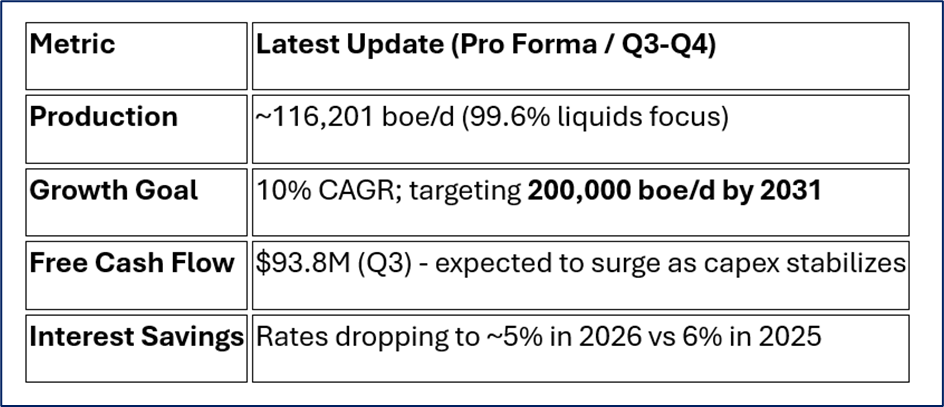

Financial & Operational Pulse (Q3/Q4 2025)

Strathcona isn't just paying dividends; it’s pumping record volumes from its core remaining assets.

Source: Company Data

Operational Milestone: The Orion project hit an all-time high of 25,000 bbls/d in October, thanks to innovative "Lower Drainage Wells" (LDWs) that recover oil from legacy sites with almost no extra steam.

SWOT Analysis: The SCR Breakdown

Source: Kalkine Group

Strengths

- Incredible Capital Efficiency: New projects (like Vawn) are being developed at less than $30,000/bbl/d.

- Massive Reserves: Proved reserve life (1P) is over 50 years in some segments.

- Institutional Backing: Waterous Energy Fund (WEF) provides aggressive, private-equity-style discipline.

Weaknesses

- Narrow Focus: 99%+ liquids concentration leaves the company highly sensitive to WCS (Western Canadian Select) price spreads.

- Governance Perception: Being majority-owned by a private equity fund (WEF) can lead to "financial sponsor" risk.

Opportunities

- M&A Hunger: Even after the failed MEG Energy bid, SCR is hunting for "distressed" thermal assets.

- Carbon Capture: Partnering with the Canada Growth Fund for a major CCUS project could re-rate the stock for ESG-conscious funds.

Threats

- Regulatory Squeeze: Increasing carbon taxes in Canada could inflate operating costs for thermal projects.

- WCS Volatility: If pipeline bottlenecks return, heavy oil differentials could eat into profit margins.

Critical Risks to Watch

- Concentration Risk: By divesting the Montney (gas/condensate), SCR has "put all its eggs in the heavy oil basket."

- Market Float: While the public float increased in 2025, the stock can still be volatile due to high insider ownership.

- Commodity Prices: A global slowdown in 2026 could see WTI slip, making thermal oil’s higher-cost extraction less attractive.

The Verdict: A New Era for SCR

Strathcona is no longer the "new kid" on the TSX; it is a battle-hardened heavy oil machine. By returning $2.1 billion to shareholders in a single move, management has signaled that they are focused on Total Shareholder Return (TSR) over mindless growth.

With a debt-to-EBITDA ratio trending toward 1.0x and a clear path to 200k barrels per day, SCR is positioned as a high-yield, high-efficiency play for those who believe in the long-term necessity of Canadian heavy oil.

Please wait processing your request...

Please wait processing your request...