Suncor Energy (TSX: SU) caught the market's attention on December 30, 2025, closing up approximately 1.7%. While the broader energy sector saw modest gains, Suncor’s outperformance is a direct result of a "perfect storm" of operational excellence, aggressive shareholder returns, and a newly released, lean 2026 outlook.

Under the leadership of CEO Rich Kruger, Suncor has transformed from a "problem child" of the oil sands into a high-efficiency cash machine. Here is the analytical breakdown of what’s driving the stock today and where the company stands heading into 2026.

The "Why" Behind the 1.7% Jump: Key Drivers

The recent uptick isn't just noise; it’s a reaction to Suncor's end-of-year momentum and its December 11 strategic update.

Source: Kalkine Group

- 2026 Efficiency Guidance: Investors are cheering Suncor's forecast for higher production in 2026 (targeting 845k–855k bpd) despite a trimmed capital budget. This "do more with less" mantra is music to the ears of institutional investors.

- WTI Stability & Margin Capture: With WTI crude hovering in a sweet spot, Suncor’s integrated model (mining to refining to gas station) is capturing massive spreads. Even with lower year-over-year oil prices, Suncor’s free funds flow has remained resilient.

- The $250M Buyback Engine: Suncor has been buying back roughly $250 million in shares every single month regardless of price volatility. This constant buying pressure provides a "floor" for the stock price and increases EPS for remaining holders.

Latest Business Model: The "Unfair Advantage"

Suncor’s 2025/2026 business model differentiates it from peers like CNRL or Imperial Oil through its Vertical Integration 2.0.

- Upstream (The Source): Massive long-life oil sands assets (Fort Hills, Syncrude) with near-zero decline rates.

- Midstream (The Link): Strategic pipeline ownership that bypasses third-party bottlenecks.

- Downstream (The Cash Cow): Refining 100%+ of its own production at times.

- Retail (The Brand): The Petro-Canada network provides a "natural hedge"—when oil prices drop, refining and retail margins usually expand, cushioning the blow.

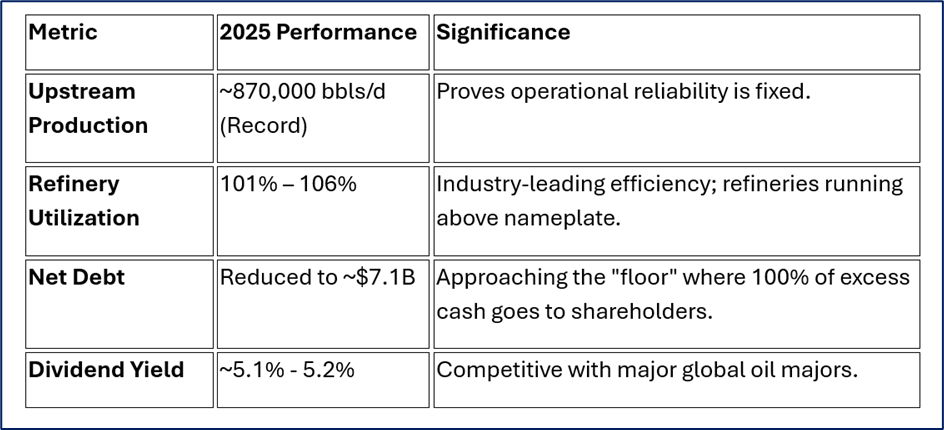

Operational & Financial Health Check (Q3/Q4 2025)

Suncor’s recent data points highlight a company firing on all cylinders:

Source: Company Data

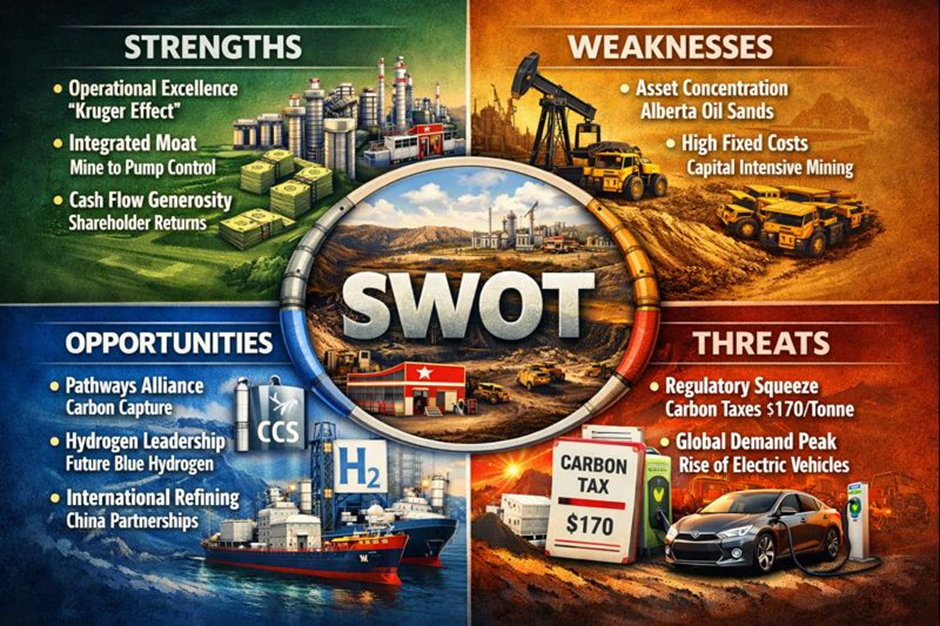

SWOT Analysis

Source: Kalkine Group

Strengths

- Operational Excellence: The "Kruger Effect" has slashed unplanned maintenance and improved safety.

- Integrated Moat: Complete control of the value chain from the mine to the gas pump.

- Cash Flow Generosity: Commitment to returning nearly all excess funds to shareholders.

Weaknesses

- Asset Concentration: Highly dependent on the Alberta Oil Sands, which are carbon-intensive.

- High Fixed Costs: Mining operations require massive constant capital compared to shale drilling.

Opportunities

- Pathways Alliance: The massive Carbon Capture (CCS) network could de-risk the company's "dirty oil" reputation.

- Hydrogen Leadership: The ATCO partnership in Alberta positions Suncor as a future blue hydrogen giant.

- International Refining: Recent partnerships with Chinese refiners open new export arbitrage.

Threats

- Regulatory Squeeze: Increasing Canadian carbon taxes ($170/tonne by 2030) pose a multi-billion dollar risk.

- Global Demand Peak: Long-term transition to EVs could eventually erode Petro-Canada’s retail dominance.

The Risk Factors: What Could Go Wrong?

While the stock is currently in a "buy/hold" favor, two primary risks loom:

- Execution Risk on Decarbonization: If the Pathways Alliance (CCS) project faces delays or cost overruns, Suncor could face institutional divestment.

- Commodity Sensitivity: Despite the integrated model, a sustained drop in WTI below $60 would likely force a pause in the aggressive buyback program.

Conclusion

Suncor Energy has successfully pivoted from a period of operational instability to one of industrial engineering precision. The 1.7% gain on December 30 reflects a market that is finally trusting management’s ability to deliver "boring" but highly profitable results. With 2026 guidance pointing toward higher output and lower costs, Suncor remains a foundational play for those seeking exposure to the Canadian energy transition.

Please wait processing your request...

Please wait processing your request...