1. The Dec 29 Rally: What Just Happened?

On December 29, 2025, TerraVest Industries (TSX: TVK) surged approximately 3.35%, closing near CAD 169. While the broader TSX Composite drifted lower (-0.32%), TerraVest stood out as a top performer.

Why the sudden pop?

There was no single new press release on December 29. Instead, this move appears to be a continuation of high-conviction accumulation following their blowout Q4/Year-End earnings released earlier this month (Dec 11).

- The "Window Dressing" Effect: As we approach year-end 2025, fund managers are likely adding "winners" to their portfolios to show they own the year's best performing stocks. TVK is up massively year-to-date, making it a prime target for this institutional behavior.

- Delayed Earnings Reaction: The market is still digesting the sheer scale of the growth reported on Dec 11 (82% revenue spike), realizing that the "expensive" valuation might actually be justified by the aggressive acquisition strategy.

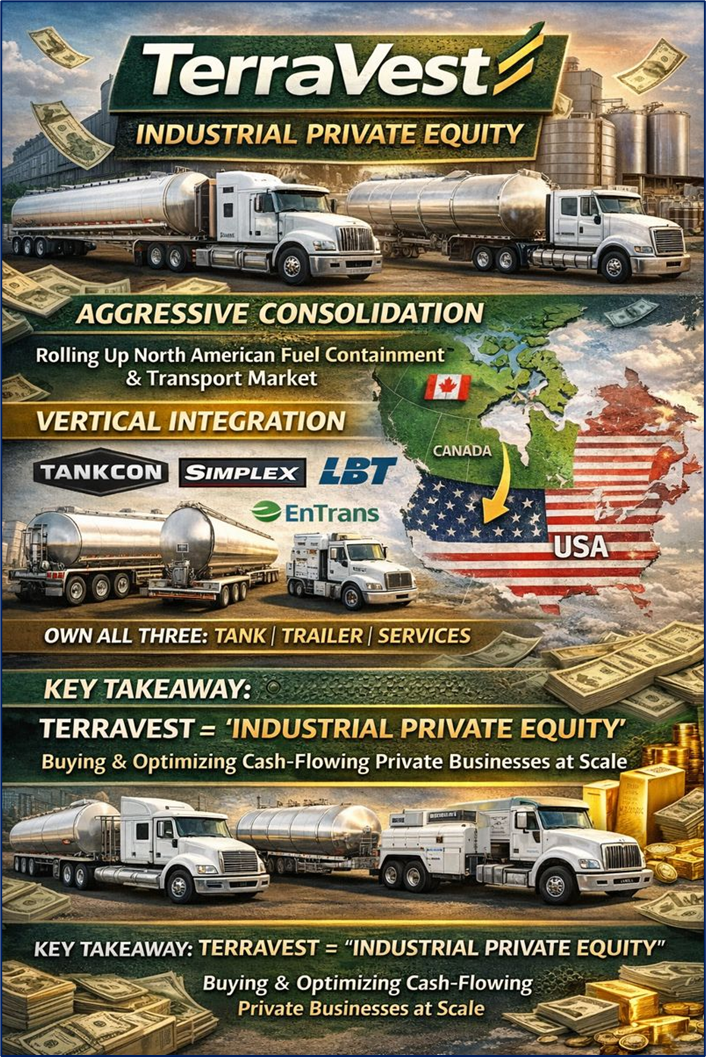

2. The Engine: Business Model "Refreshed"

TerraVest is no longer just a boring manufacturer of propane tanks. It has evolved into a diversified industrial compounder.

Source: Kalkine Group

The New 2025 Strategy:

- Aggressive Consolidation: They are rolling up the fragmented North American market for fuel containment (tanks) and transport (trailers).

- Vertical Integration: By acquiring Tankcon, Simplex, LBT, and EnTrans in 2025 alone, they now control the manufacturing of the tank, the trailer it sits on, and the logistics services (water/heating) that support the energy sector.

- Geography: They have aggressively expanded south into the USA (via EnTrans and LBT), reducing their reliance on the Canadian energy cycle.

Key Takeaway: TerraVest is effectively an "Industrial Private Equity" firm that trades publicly. They buy unloved, cash-flowing private businesses, optimize them, and use the cash flow to buy more.

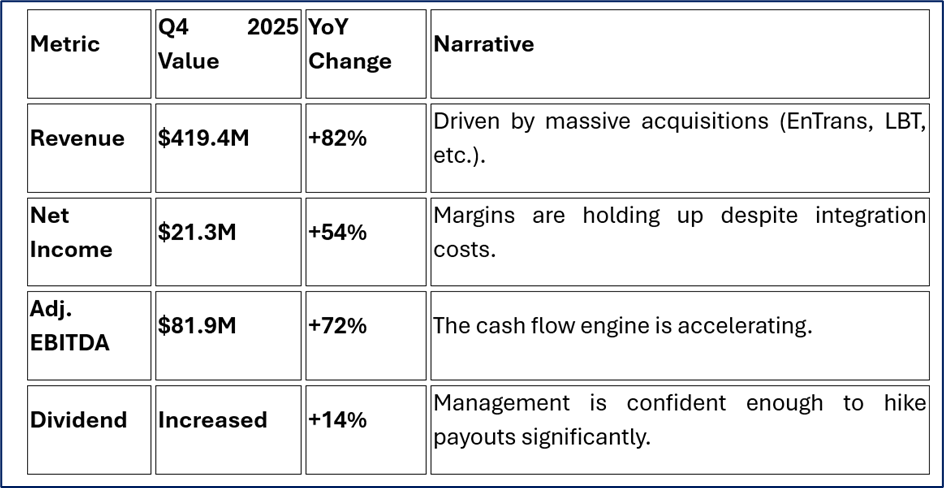

3. Financial Firepower: Q4 2025 Snapshot

The numbers released in mid-December explain the high investor confidence. The growth rates are startling for an industrial company.

Source: Company Data

4. SWOT Analysis

Source: Kalkine Group

Strengths (The Moat)

TerraVest creates a "local monopoly" effect. In many niche markets (e.g., residential propane tanks in Western Canada or specialized fracking water heating), they are the dominant player. Their ability to integrate acquisitions without destroying culture is rare. The 14% dividend hike signals extreme confidence in cash flow sustainability.

Weaknesses (The Cracks)

Liquidity is low. With an average volume often under 60k shares, it is hard for large institutions to enter or exit without moving the price. The company also operates with a complex structure of subsidiaries, making "sum of the parts" valuation difficult for retail investors to calculate accurately.

Opportunities (The Upside)

The US market is the golden goose. The 2025 acquisitions of EnTrans (Tennessee) and LBT (Nebraska) open the door to a market 10x the size of Canada. If they can replicate their Canadian dominance in the US mid-west, the stock could double again.

Threats (The Risks)

Tariffs. With a new US administration potentially focusing on protectionism, cross-border manufacturing (parts moving between Canada/USA) could face friction. However, their recent US acquisitions act as a natural hedge against this. Rising interest rates are also a threat, as their M&A strategy relies on debt leverage.

5. Why Caution is Needed

Despite the bullish price action, you must look at the valuation.

- P/E Expansion: The stock is trading at a P/E of ~40x. This is "Tech Stock" territory for a company that bends metal.

- priced for Perfection: At this multiple, the market expects 20%+ growth to continue indefinitely. If they miss earnings in Q1 2026 or if an acquisition integration stumbles, the multiple compression could be severe (stock drops to match lower expectations).

- Cyclicality: Ultimately, they serve the energy and heating sectors. A warm winter or an oil price crash still impacts their base business.

6. Conclusion

TerraVest Industries' 3.4% rise on December 29 is the market's vote of confidence in a "Compounder" strategy that is firing on all cylinders. The company has successfully transitioned from a Canadian tank maker to a North American logistics giant.

Verdict: The momentum is undeniable, but the valuation demands respect. This is a stock for those who believe management can continue to find and integrate cheap acquisitions in 2026.

Please wait processing your request...

Please wait processing your request...