In early 2026, the Canadian telecommunications landscape is witnessing a historic anomaly as TELUS Corporation (TSX: T) offers a dividend yield exceeding 9%, a level typically reserved for distressed assets rather than blue-chip incumbents. This sky-high yield is the byproduct of a significant stock price drawdown—nearly 46% from its all-time highs—colliding with a management team that has chosen to "pause" dividend growth to prioritize aggressive deleveraging.

While the yield captures the headlines, the underlying narrative is one of a telecom giant in the midst of a massive structural pivot: transitioning from a traditional connectivity provider into a diversified digital powerhouse fueled by AI infrastructure and high-margin health services.

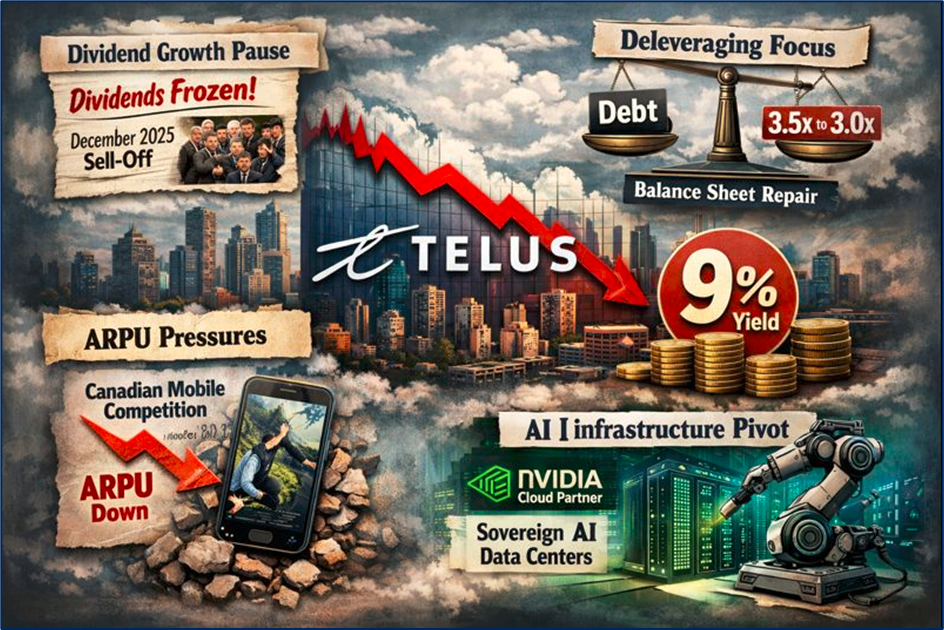

Latest Drivers and Reasons for Yield Surge

Source: Kalkine Group

The primary driver of the current 9% yield is a prolonged decline in the share price, which has been pressured by a high-interest-rate environment that increased the cost of servicing Telus’s debt.

- Dividend Growth Pause: In December 2025, Telus announced a temporary halt to its legendary semi-annual dividend increases. This move was intended to signal fiscal discipline but initially led to a sell-off among income-seeking investors (TELUS Investor Relations, Dec 2025).

- Deleveraging Focus: The market is pricing in the company’s pivot from "growth at all costs" to "balance sheet restoration," as the company aims to lower its net debt-to-EBITDA ratio from 3.5x to 3.0x by 2027.

- ARPU Pressures: While customer additions remain strong, the "backbook" repricing and competitive intensity in the Canadian mobile market have weighed on Average Revenue Per User (ARPU).

- AI Infrastructure Pivot: Telus has transformed into an NVIDIA Cloud Partner, shifting capital expenditures toward "Sovereign AI" data centers, a move that requires heavy upfront investment but promises higher long-term margins (TELUS Media Release, Nov 2025).

Current Business Model

Telus has moved beyond being a "Simple Telco" to a "Puretone" model—unbundling its business into distinct, high-growth segments that leverage its core network.

- TTech (Core Connectivity): The backbone of the company, providing 5G and PureFibre internet. This segment now emphasizes "profitable customer growth" over pure volume.

- TELUS Health: A global provider of digital health solutions, currently covering over 160 million lives. It is being positioned for potential partial monetization or strategic partnerships in 2026.

- TELUS Digital: Recently privatized, this segment focuses on AI-powered customer experience (CX) and is integrated to provide $150–$200 million in annual synergies.

- Sovereign AI Factory: A newer pillar focused on providing secure, Canadian-hosted AI compute for government and enterprise clients.

Latest Financial and Operational Updates (Company Sourced)

- Free Cash Flow (FCF) Guidance: Telus is targeting $2.4 billion in FCF for 2026, representing a minimum 10% compounded annual growth rate through 2028 (TELUS Corp, Dec 2025).

- Debt Management: In January 2026, the company successfully redeemed $600 million of 3.75% Series CV Notes, funded by a $2.9 billion "Hybrid Note" offering to improve financial flexibility (TELUS PR Newswire, Jan 2026).

- Customer Growth: Q3 2025 saw 288,000 total net additions, including 82,000 mobile phone and 40,000 internet subscribers, reaching a total of 21 million connections (TELUS Q3 Report, Nov 2025).

- Share Buybacks: Management initiated a Normal Course Issuer Bid (NCIB) in late 2025, purchasing 2.3 million shares for cancellation at an average price of $17.39, signaling internal confidence in the stock's value (TELUS News, Jan 2026).

Latest Analyst Coverage

- Morningstar: Noted that Telus’s fiber network ownership allows it to outperform peers in fixed-line sales, though interest coverage remains a metric to watch at 1.80x (Morningstar, Jan 20, 2026).

- Simply Wall St: Highlights the 9.1% yield as being in the top 25% of the Canadian market, though they flag a payout ratio that currently exceeds earnings (211%) but is supported by growing cash flows (Simply Wall St, Jan 2026).

Outlook and Risks

- The 2026 Outlook: Management expects to exit 2026 with a leverage ratio of 3.3x. The focus remains on "monetization of non-core assets," including real estate and copper infrastructure, to accelerate debt reduction.

- AI Growth: AI-enabled sales are projected to rise from $800 million in 2025 to approximately $2 billion by 2028.

- Key Risks: Continued high interest rates could prolong the debt-reduction timeline. Additionally, aggressive competition from Rogers and Bell in the wireless space could continue to squeeze margins, while any delay in the $150 million synergy realization from Telus Digital could impact FCF targets.

Conclusion

Telus has entered 2026 as a high-yield outlier on the TSX. By pausing dividend growth and aggressively repurchasing its own shares at a discount, the leadership team is betting that the company's evolution into an AI and Health-focused entity will eventually trigger a valuation re-rating. For now, the 9% yield stands as a stark reminder of the market's caution regarding its debt levels, balanced against the company’s robust 10% annual free cash flow growth targets.

Please wait processing your request...

Please wait processing your request...