The global financial narrative around Artificial Intelligence (AI) is no longer just about groundbreaking technology; it's about a self-reinforcing, multi-billion-dollar financial structure known as Circular Financing or Vendor Financing. This strategy, unprecedented in its current scale, involves major hardware and cloud suppliers investing massive capital into AI developers, who then immediately commit to spending that money on the investor's own products.

This detailed analysis provides the latest data, case studies, and critical risks of this financial dynamic dominating the US and Canadian tech sectors as of late 2025.

Content: The Mechanics of the AI Circular Loop

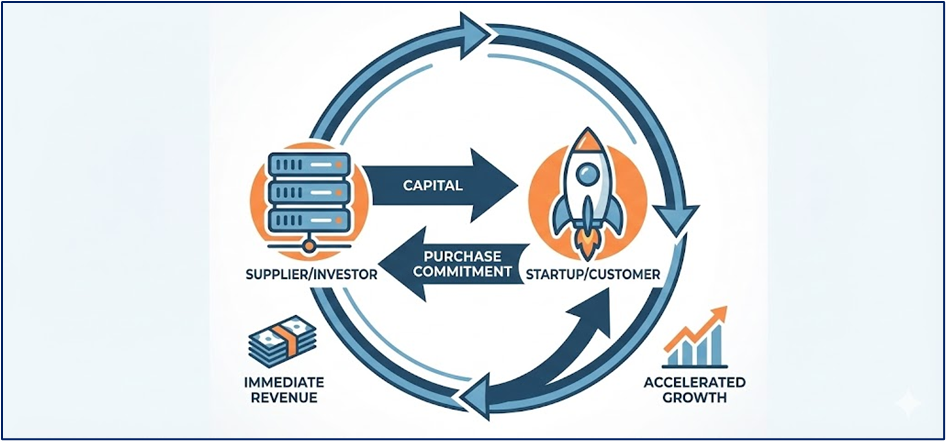

1. The Core Mechanism

Circular financing in AI is the practice where a handful of powerful players simultaneously function as investor, supplier, and customer. The money essentially flows out of a major giant (e.g., Nvidia) as an investment and cycles back to its balance sheet as revenue from the startup (e.g., OpenAI) purchasing its hardware or cloud services.

Source: Kalkine Group

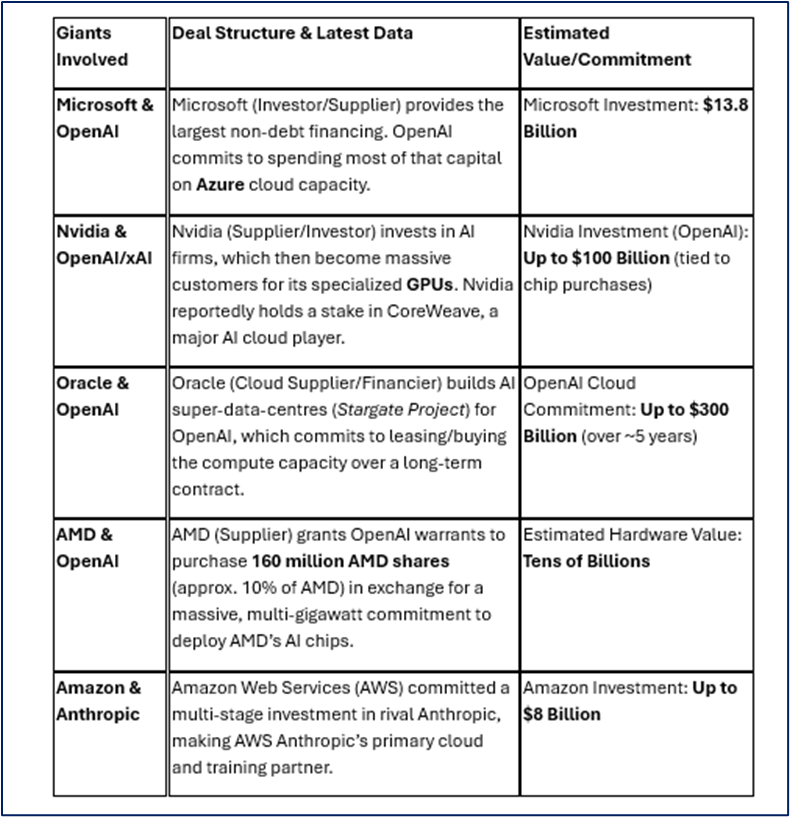

2. Major Case Studies: US & Canadian Giants (Updated 2025)

The most prominent cases of circular financing are creating a tightly bound ecosystem, binding the fortunes of the largest technology companies and the leading AI labs.

3. The Canadian Nexus: Compute Infrastructure

While the core AI labs are primarily US-based (OpenAI, Anthropic), the sheer demand for data centres and specialized compute is driving the growth of hyperscalers and GPU suppliers who heavily utilize and expand Canadian data centre capacity. This loop ensures Canadian infrastructure providers are direct beneficiaries of the circular capital.

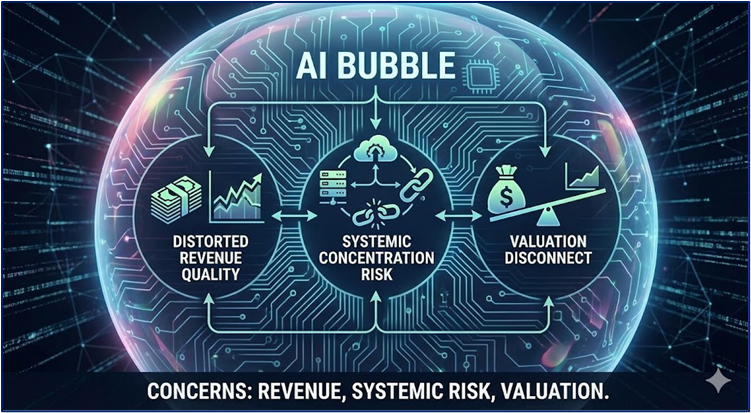

Analytical Take: Bubble or Boom?

The "AI Bubble" Concerns

- Distorted Revenue Quality: The primary criticism is that the sales generated by the supplier (e.g., Nvidia's GPU sales) are funded by the supplier's own investment capital, potentially inflating reported revenues and making it difficult to gauge genuine, external customer demand.

- Systemic Concentration Risk: The entire ecosystem is hyper-interconnected. If a flagship AI lab were to underperform or if a major cloud provider's monetization strategy faltered, the chain reaction could lead to cascading losses across partner balance sheets, mirroring aspects of the late-90s telecom crash.

- Valuation Disconnect: While current Price-to-Earnings (P/E) ratios for Big Tech are generally lower than the dot-com peak, the high valuations of AI startups and the sheer volume of capital expenditure ($50 billion+ annual Capex for some hyperscalers) rely on an uninterrupted, exponential growth narrative.

Source: Kalkine Group

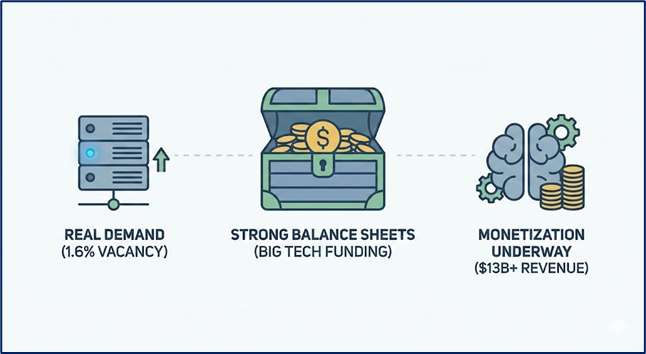

The "Sustainable Boom" Argument

- Real, Tangible Demand: Unlike the dot-com era where vast fiber-optic capacity went unused, current data suggests a genuine shortage of AI compute power. North American data centre vacancy rates are at a record low of 1.6% (H1 2025 data), and utilization is reportedly near 80%, indicating the infrastructure being financed is immediately put to use.

- Stronger Balance Sheets: Today's primary financiers (Microsoft, Amazon, Alphabet) are funding this build-out largely from their massive, proven free cash flows and retained earnings, not risky debt, making the system more resilient than the heavily debt-leveraged telecom sector of the 1990s.

- Monetization Underway: Companies like OpenAI are already generating substantial revenue (estimated $13 billion run-rate in 2025), a stark contrast to many dot-com entities that achieved high valuations with no clear monetization path.

Source: Kalkine Group

Conclusion: The Financial Scaffolding of the Next Economy

Circular financing has become the default financing mechanism for AI infrastructure because the cost and scarcity of compute power have outpaced traditional venture capital and public market funding capabilities. It is not an inherently fraudulent scheme, but an urgent solution to bootstrap the physical backbone of the AI economy.

The market consensus is watchful: the loop is currently sustainable due to genuine, explosive demand for AI compute and the deep pockets of the Big Tech financiers. However, investors must be keenly aware that the risks are concentrated within this small, hyper-leveraged network. Any regulatory action or a major failure to meet expected monetization targets could trigger a disproportionately large market correction.

This process is accelerating innovation and competition but is simultaneously constructing an intertwined financial architecture whose stability hinges on the one certainty in the AI world: compute demand will continue to grow exponentially.

Please wait processing your request...

Please wait processing your request...