TerraVest Industries (TSX: TVK) stock experienced a massive surge yesterday, climbing nearly 29% on the Toronto Stock Exchange. This dramatic jump was fueled by an exceptional earnings report that showcased significant financial growth and a renewed vote of confidence from a major analyst.

Key Takeaways

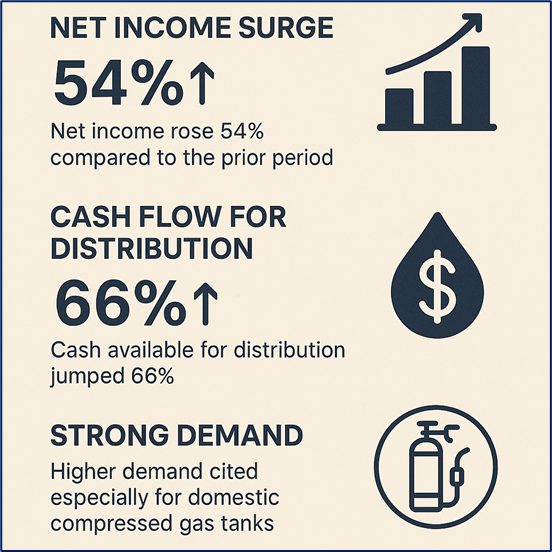

- Exceptional Financial Beat: Q4 2025 results significantly surpassed market expectations, with Net Income climbing 54% and the crucial Cash Available for Distribution (CAD) soaring by 66% year-over-year.

- Primary Driver: The massive stock surge was primarily driven by these stellar earnings, confirming the strength of its industrial compounding model.

- Dividend Boost: The company signaled high confidence in future cash flow by declaring a 14% increase in the quarterly dividend to $0.20 per share, attracting income investors.

- Analyst Endorsement: BMO Capital upgraded the stock to "Outperform" and significantly raised its price target to C$200.00 (from C$150.00), validating the strong results.

- Resilient Organic Growth: The base portfolio of businesses achieved a robust 7% organic growth, demonstrating operational health beyond just expansion via acquisitions.

The Explosive Performance: Reasons Behind the 29% Surge

The key driver behind TerraVest's powerful stock move was the release of its fiscal fourth-quarter and full-year 2025 results, which far exceeded analyst expectations and demonstrated impressive operational leverage across its segments.

1.Spectacular Q4 2025 Financial Beat

The headline figures from the earnings report were undeniable and indicated a strong operational performance:

- Net Income Surge: Net income for the quarter jumped 54% compared to the prior comparable period, reflecting strong profitability, particularly in the domestic market segments.

- Cash Flow for Distribution: Crucially for a company focused on returns, Cash Available for Distribution (CAD) skyrocketed by 66% in the fourth quarter. This metric is a strong indicator of the cash generated that can be used for dividends, share buybacks, or future acquisitions, which directly impacts shareholder value.

- Strong Demand: The company cited higher demand in the Service and HVAC and Containment Equipment segments, particularly for domestic compressed gas tanks, as core to the revenue growth.

Source: Kalkine Group

2. A Significant 14% Dividend Increase

In a clear signal of confidence in its sustained cash flow generation and future profitability, the Board of Directors declared a 14% increase in the quarterly dividend to $0.20 per common share. A substantial dividend hike often attracts a new wave of investors, putting significant upward pressure on the stock price and underscoring management's positive outlook.

3. Major Analyst Upgrade and Price Target Lift

The positive momentum was further cemented by a significant endorsement from a key financial institution. BMO Capital Markets upgraded TerraVest Industries from "Market Perform" to "Outperform," while simultaneously increasing its price target from C$150.00 to a new high of C$200.00.

BMO noted that the company is managing tariff challenges comfortably and believes that TerraVest's highly successful acquisition activity is poised to accelerate again in fiscal 2026. This third-party validation helps reset market expectations for the stock's future valuation.

TerraVest Industries: Business Model and Latest Updates

TerraVest operates as an industrial compounder, focused on acquiring and operating market-leading businesses within niche infrastructure markets. Its core objective is to grow free cash flow per share through a disciplined combination of organic growth and strategic, accretive acquisitions.

The company operates through four main segments that provide essential industrial products and services:

- HVAC and Containment Equipment: Manufactures and distributes home heating products, including residential refined fuel tanks, furnaces, and air conditioning equipment.

- Compressed Gas Equipment: Manufactures products for the storage, distribution, and dispensing of compressed gases (like propane, natural gas liquids, and anhydrous ammonia), including bulk storage vessels and transport trailers.

- Processing Equipment: Provides wellhead processing equipment, desanding units, and custom process equipment primarily for the oil and gas industry.

- Service: Offers water management, environmental, heating, and well services.

Latest Business Updates

The 2025 results highlight the successful integration of recent acquisitions, including Entrans, LBT, Tankcon, Simplex, Aureus, Advance, and Highland, which positively contributed to net income and revenue growth.

Crucially, the base portfolio achieved approximately 7% organic growth, demonstrating that the existing businesses are thriving alongside the expansion from acquisitions. This blend of strong operational performance in core segments and strategic M&A is a hallmark of the company's compounding success.

Key Risks and Investment Outlook

Risks to Monitor

While the outlook is strong, investors must be aware of inherent risks, especially for an acquisitive industrial company:

- Integration Risk: The company's growth relies heavily on its ability to successfully integrate new acquisitions and achieve anticipated synergies.

- Interest Rate/Leverage Risk: The acquisition-driven model often requires taking on debt. Higher financing costs due to rising interest rates can pressure net income and overall returns.

- Economic/Tariff Uncertainty: As a manufacturer, the company is exposed to broader economic slowdowns and regulatory changes, such as recent tariff announcements, which have previously resulted in "softer demand" in some business lines.

Outlook and Conclusion

TerraVest Industries has emphatically proven its capacity to grow both organically and through acquisition, delivering exceptional financial results that justify the recent, massive stock price appreciation.

The strong Q4 results, the 14% dividend hike, and the subsequent analyst upgrade point to a premium valuation being warranted for this well-executed industrial compounder. The market is now pricing in sustained outperformance and high-quality returns. For investors, the narrative remains one of durable industrial exposure combined with energy-linked growth, led by a highly effective, disciplined M&A strategy.

The company's focus on essential niche infrastructure products and its proven track record of strong cash flow generation position it well for continued success, provided it can manage integration and leverage risks effectively. The path forward looks bright, with the market signaling renewed confidence in its ability to generate high returns.

Source: Trading View, 11 December 2025

Please wait processing your request...

Please wait processing your request...