Today, Friday, December 19, 2025, the Bank of Japan is concluding its final policy meeting of the year, and markets are bracing for what increasingly looks like a near-certain 25-basis-point rate hike, taking the short-term policy rate toward 0.75%.

This would not be just another incremental move. A hike of this magnitude would push Japanese interest rates to their highest level since 1995, marking a definitive break from nearly three decades of ultra-easy monetary policy.

For years, Japan’s zero-rate regime acted as the fuel line for global risk, powering the Yen carry trade that financed everything from U.S. tech stocks to emerging-market debt and crypto. Now, with the verdict imminent and policy normalization accelerating, that bridge is actively being dismantled, not repaired.

The signal is clear: capital is preparing to come home, and the global liquidity map is on the verge of a major redraw.

The Hard Numbers: What’s at Stake?

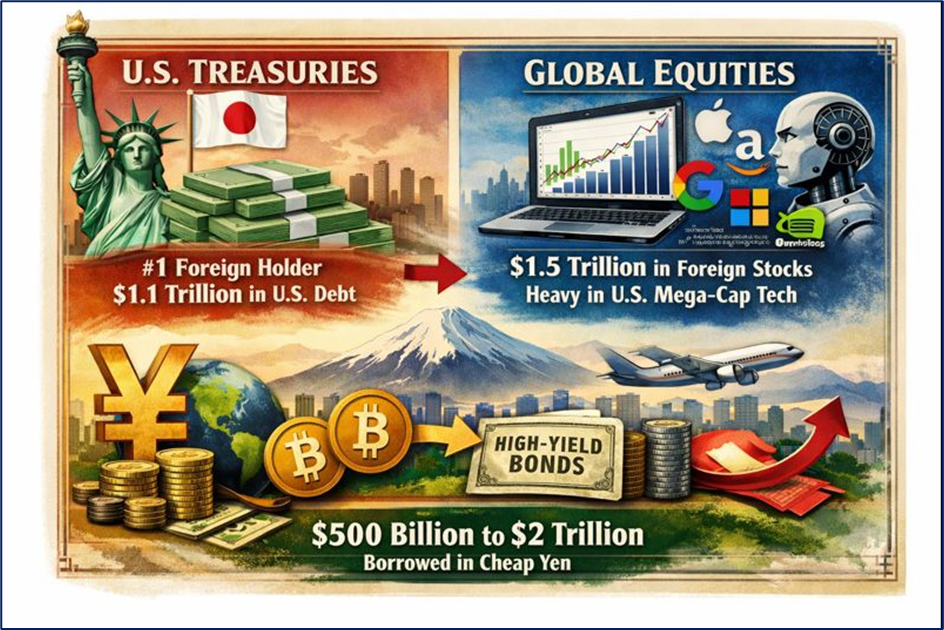

Japan sits on the world’s largest net international investment position, totalling $3.66 trillion (as of Q3 2025). The total footprint of Japanese capital globally is a staggering $4.9 trillion.

Source: Kalkine Group

The Exposure Breakdown:

- U.S. Treasuries: Japan is the #1 foreign holder, with $1.1 trillion in US debt.

- Global Equities: Roughly $1.5 trillion is parked in foreign stocks, heavily weighted toward U.S. Mega-Cap Tech (AI and the "Magnificent Seven").

- The Carry Trade: Estimated at $500 billion to $2 trillion, this represents money borrowed in cheap Yen to fund everything from high-yield emerging market bonds to Bitcoin.

Fund Manager Strategy: The "Repatriation" Playbook

Institutional "whales" like Japan’s GPIF (the world’s largest pension fund) and global hedge funds are shifting gears. The strategy going forward focuses on Repatriation and De-leveraging.

Source: Kalkine Group

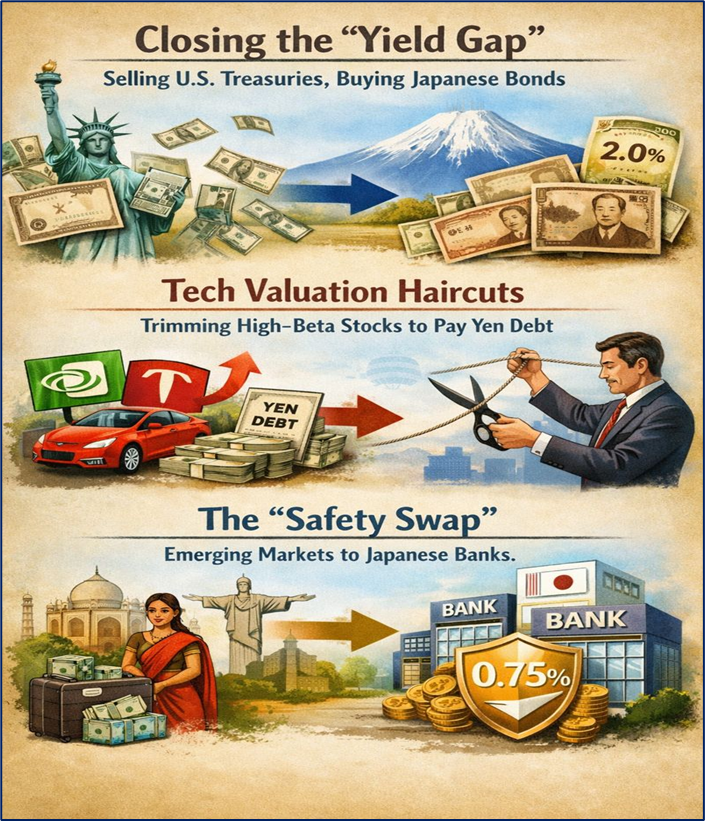

- Closing the "Yield Gap": With 10-year Japanese Government Bond (JGB) yields surging toward 2.0%, Japanese insurers no longer need to chase U.S. yields that come with high currency-hedging costs.

- The Move: Selling U.S. Treasuries and bringing cash home to buy domestic JGBs.

- Tech Valuation Haircuts: Fund managers are reducing exposure to "high-beta" assets. The Yen was the funding currency for risk; as Yen borrowing costs rise, managers are trimming "winner" positions (Nvidia, Tesla) to pay back Yen-denominated debt.

- The "Safety Swap": Rotating out of emerging markets (India, Brazil) and into Japanese Banks, which directly profit from expanded lending margins at 0.75%.

Retail Investor Landscape: Navigating the Unwind

For retail investors, the BOJ hike marks the end of "easy mode" for global liquidity. The primary risk is a volatility spike rather than a fundamental collapse.

Source: Kalkine Group

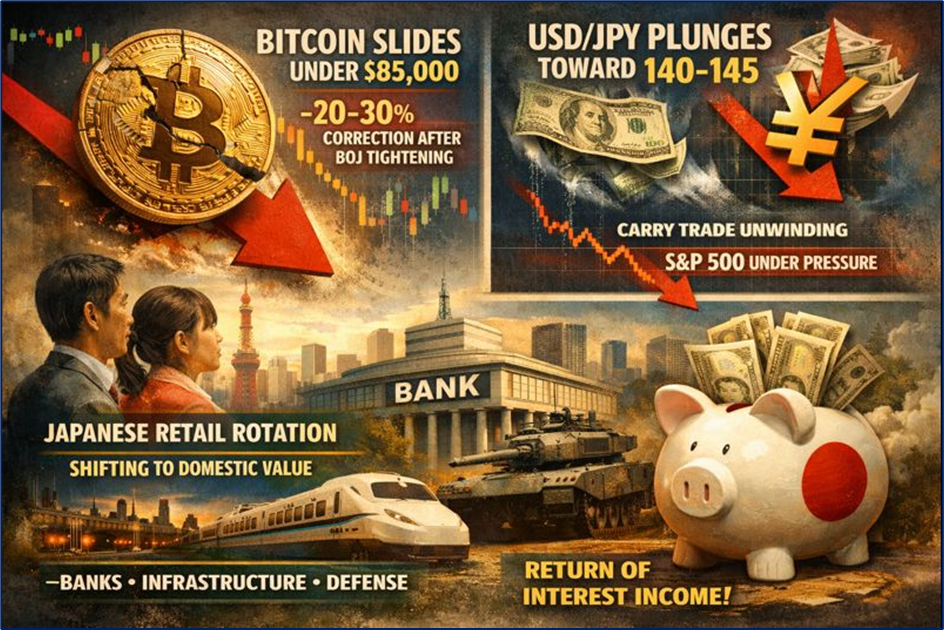

- Crypto Sensitivity: Historically, every major BOJ tightening event in 2024 and 2025 has been followed by a 20-30% correction in Bitcoin. As of today, BTC is under pressure, trading near the $85,000 mark as traders brace for a liquidity drain.

- Currency Shifts: The USD/JPY is the most critical ticker on the board. A move toward 140–145 would signify a massive unwinding of carry trades, putting downward pressure on the S&P 500.

- Domestic Japan Rotation: Retail sentiment in Japan is shifting toward domestic value. Banks and "Sanaenomics-aligned" sectors (infrastructure and defense) are seeing increased inflows as the middle class anticipates a return of interest income on their savings.

Market Reaction Summary

Source: Kalkine Group

Conclusion: A Return to "Normal"

The verdict is in: Japan is finally re-joining the global monetary norm. While the 0.75% rate is still low by Western standards, the velocity of the change is what matters. The global financial system has been "doped" on cheap yen for 30 years; today, the withdrawal symptoms have officially begun.

Key Watch Item: Governor Kazuo Ueda’s press conference (06:30 GMT). If he hints at a 1.0% terminal rate by mid-2026, expect the Yen rally and the Tech sell-off to accelerate into the weekend.

Please wait processing your request...

Please wait processing your request...