Dollarama Inc. (TSX: DOL) remains one of the most closely watched defensive growth stocks in North America. With the retail landscape shifting due to persistent consumer pressure and international expansion, the stock's "Buy" or "Hold" status is a central debate among institutional desks and retail analysts.

Business Model & Current Drivers

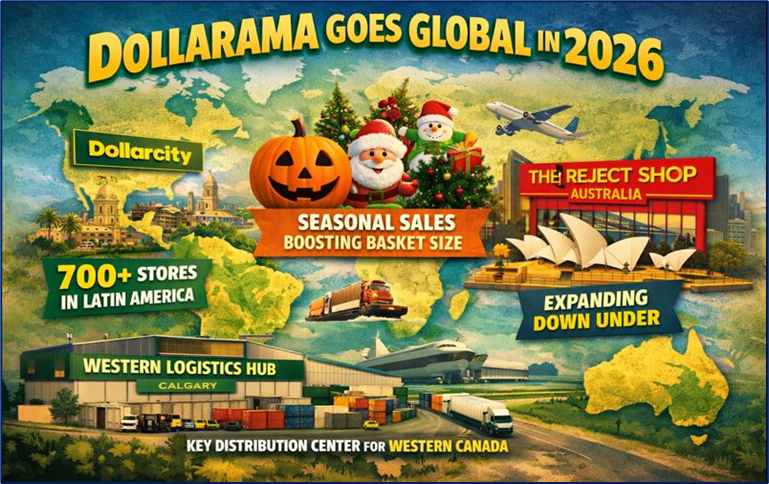

Dollarama continues to operate as the undisputed leader in Canadian discount retail, but 2026 marks a pivotal transition into a global multi-banner conglomerate. The core Canadian business model remains "fixed-price-point" retail, focusing on convenience and consumables. However, the current drivers are increasingly international. The majority-owned Dollarcity has surpassed 700 stores in Latin America, and the recent acquisition of The Reject Shop in Australia is now the primary laboratory for Dollarama's operational "playbook" transformation.

- The company is shifting from a purely Canadian story to a three-continent growth engine.

- Consumables remain the primary traffic driver, but high-margin seasonal items (like Halloween and Christmas) are providing the "basket size" growth.

- The "Western Logistics Hub" near Calgary is a key operational driver for 2026, aimed at reducing transport costs for the western provinces.

Source: Kalkine Group

Technical Analysis (As of January 20, 2026)

Source: Trading View

The technical profile for TSX: DOL shows a stock in a persistent long-term uptrend, currently trading near its 52-week highs around the $200 – $206 range. Historically, the stock has utilized its 200-day moving average (currently sitting near $191.38) as a reliable support floor. In the last 14 days, the stock has successfully cleared psychological resistance at $200, confirming bullish momentum. Relative Strength Index (RSI) levels are hovering around 45, suggesting the stock is approaching "overbought" territory slowly but still has room for a momentum run before a cooling period. Support is firmly established at $195, while the immediate upside target for technical traders is the consensus analyst high of $235.

Analyst Upgrades, Downgrades & Valuation

The "Smart Money" sentiment remains "Moderate Buy" despite a high valuation. Following the December earnings beat, a wave of price target increases occurred.

- TD Securities: Increased target to $235 (Buy).

- Royal Bank of Canada (RBC): Boosted target to $225 (Outperform).

- Scotiabank: Raised target to $220 (Outperform).

- Wells Fargo: Maintained Equal Weight but raised target to $195.

- Valuation: Currently, Dollarama trades at a Trailing P/E of approximately 42.4x, significantly higher than its 10-year historical average of 28x. This premium reflects the market's willingness to pay for "recession-proof" earnings and the high growth rate of international segments.

Financials & Dividend Analysis

Dollarama’s latest Q3 Fiscal 2026 results (ended late 2025) showed a massive 22.2% increase in sales, reaching $1.91 billion. This was heavily influenced by the consolidation of Australian operations. Canadian same-store sales grew by a robust 6.0%, beating the 3-4% guidance.

- Dividends: The current quarterly dividend stands at $0.1058 CAD, yielding approximately 0.21%. While the yield is low, the dividend growth rate is high, averaging nearly 20% annually over the last three years.

- Payout Ratio: The payout ratio remains exceptionally low (under 10%), as management prioritizes share buybacks (repurchasing over 2.6 million shares in Q3 alone) and international CAPEX.

- Liquidity: A quick ratio of 0.08 remains a point of concern for some bears, but the company’s massive cash-flow generation and low debt-to-equity (by retail standards) mitigate immediate liquidity risks.

Outlook, Guidance & Risks

Management has raised its full-year Fiscal 2026 same-store sales (SSS) guidance to 4.2% – 4.7% and increased gross margin targets to 45.0% – 45.5%. The outlook for 2027 (starting February 2026) anticipates revenue growth of 12% and EPS growth of 13%+.

- The Australia Transformation: The Reject Shop will undergo a 4-year renovation plan to mirror the Dollarama layout, which analysts believe will unlock significant margin expansion.

- Mexico Expansion: The 2025 entry into Mexico is the "wild card" for 2026, with the market watching to see if the Dollarcity model can scale against established Mexican discounters.

- Risks: The primary risks include valuation compression (if growth slows, the 42x P/E is vulnerable), geopolitical supply chain shocks for Asian-sourced goods, and labour cost inflation in the Canadian market.

Conclusion

Dollarama remains a "gold standard" for defensive growth on the TSX. While the valuation is historically "expensive," the stock's ability to beat expectations and provide shelter during economic uncertainty continues to attract institutional capital. For investors seeking value, the current price offers little "margin of safety," but for those seeking a high-quality compounding machine with international tailwinds, it remains a core holding.

Please wait processing your request...

Please wait processing your request...