In 2026, the S&P/TSX Composite has evolved into a global powerhouse for wealth compounding, outperforming major U.S. indices as the "AI-driven commodity supercycle" takes hold. While the Nasdaq faces valuation friction, the TSX Metals & Mining sector has become a primary hedge for smart money.

According to major investment banks like Goldman Sachs and Bernstein, the focus has shifted from mere extraction to "critical mineral security" and "precious metal revaluation" as central banks continue to diversify away from the dollar.

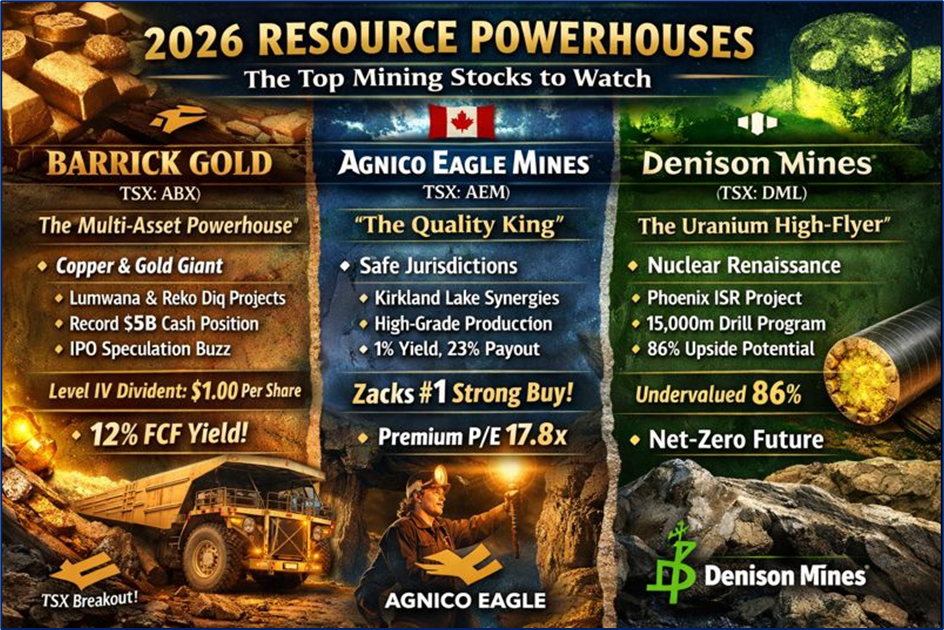

Below is an analytical deep dive into the top three TSX mining stocks positioned for multibagger potential in 2026.

Source: Kalkine Group

The Multi-Asset Powerhouse of the 2026 Gold Bull Run

Key Reasons and Drivers

Barrick Gold has transitioned from a pure-play gold miner into a diversified "Tier One" producer. The primary driver is the unprecedented rise in spot gold prices, which reached $4,650 per ounce in early 2026.

- Copper Synergies: Barrick’s massive investment in the Lumwana Super Pit and Reko Diq projects has transformed it into a significant copper producer, tapping into the AI-driven grid electrification demand.

- North American IPO Speculation: Global fund managers are closely watching Barrick’s potential IPO of its North American assets, a move expected to unlock massive latent value for TSX shareholders.

Latest Business Model and Financials

The company operates on a "high-margin, low-AISC" (All-In Sustaining Cost) model, focusing strictly on Tier One assets that produce over 500,000 ounces of gold annually at low costs.

- Operational Update: Barrick reported a record cash position of $5 billion in Q4 2025, with production ramping up at the Goldrush mine in Nevada.

- Latest Dividend: Barrick maintains a performance-based dividend structure. With net cash exceeding $1 billion, the company is currently at "Level IV" payouts, yielding roughly $1.00 per share annually (approx. 1.1% - 1.6% yield depending on entry).

- Latest Valuation: Trading at a forward P/E of 12.99x, Barrick remains at a discount compared to its 5-year median and its peer group average of 13.25x.

Technical Analysis and Analyst Sentiment

Technically, Barrick has broken out of a multi-year consolidation pattern. Analysts at BNP Paribas Exane and Jefferies recently upgraded the stock to "Outperform," citing a projected free cash flow yield of 12% for 2026—the highest in its peer group. The stock is currently testing resistance levels not seen since 2011, supported by heavy institutional "smart money" inflows.

The "Quality King" of Low-Risk Jurisdictions

Key Reasons and Drivers

Agnico Eagle is the preferred choice for conservative hedge funds due to its nearly exclusive focus on low-risk regions like Canada, Australia, and Finland.

- Jurisdictional Safety: As resource nationalism rises in emerging markets, Agnico’s Canadian-heavy portfolio commands a "safety premium."

- Synergy Realization: The 2022 Kirkland Lake merger is now yielding full operational synergies, particularly at the Detour Lake and Macassa mines, driving costs down as throughput hits record highs.

Latest Business Model and Financials

Agnico focuses on high-grade underground mining and regional consolidation. Its "hub-and-spoke" model in the Abitibi region allows it to process ore from multiple sites through central mills, drastically reducing capital expenditure.

- Operational Update: Preliminary 2025 revenue hit record highs. The company is currently exploring organic growth targets that could push production beyond 2030 levels.

- Latest Dividend: Agnico offers a 1% yield with a sustainable payout ratio of 23%, recently reporting a 5-year annualized dividend growth rate of 3.1%.

- Latest Valuation: Trading at a premium (forward P/E of ~17.8x) compared to Barrick, reflecting its superior Return on Equity (ROE) and lower leverage (debt-to-capitalization of only 1.2%).

Technical Analysis and Analyst Sentiment

Agnico is currently categorized as a "Zacks Rank #1 (Strong Buy)." Technical charts show a "golden cross" occurring in late 2025, with the stock outperforming the Zacks Mining-Gold industry index by nearly 20% over the last six months. Analysts at BMO Private Wealth note that Agnico is the "ultimate compounding vehicle" for investors seeking gold exposure without the geopolitical volatility of South American or African operations.

The High-Alpha Uranium Play for the Net-Zero Era

Key Reasons and Drivers

Unlike the gold giants, Denison Mines is a "multibagger" candidate driven by the 2026 nuclear renaissance. With the global shift toward AI data centers requiring 24/7 carbon-free power, uranium has entered a structural deficit.

- Phoenix Project Innovation: Denison’s use of In-Situ Recovery (ISR) mining at its flagship Phoenix deposit allows for some of the lowest operating costs globally.

- Strategic Inventory: The company holds significant physical uranium piles, which act as a direct lever to skyrocketing spot prices.

Latest Business Model and Financials

Denison is transitioning from a developer to a producer. Its business model relies on high-margin, low-CAPEX extraction in the world-class Athabasca Basin.

- Operational Update: Denison recently completed a 15,000-meter drilling program, eyeing deeper sulphide zones to expand its mineral resource.

- Latest Dividend: As a growth-stage mining company, Denison does not currently pay a dividend, reinvesting all cash flow into project development.

- Latest Valuation: Simply Wall St’s DCF (Discounted Cash Flow) analysis suggests Denison is significantly undervalued by as much as 86% based on projected 2030 cash flows, with an intrinsic value estimate near $39.00 vs. its current $5.00 range.

Technical Analysis and Analyst Sentiment

Denison has seen a staggering 89% return over the past year. While some analysts warn of "peak-on-peak" valuations, the consensus remains a "Buy" among uranium specialists. The stock is currently in a "momentum" phase, with high insider ownership signaling confidence in the upcoming 2026 production milestones.

Sector Outlook and Risks

Outlook: The 2026 outlook for TSX miners is "Neutral to Bullish." While commodity prices are elevated, the shift toward production expansion—rather than just deleveraging—is the new theme. Risks:

- Cost Inflation: Rising labor and energy costs could compress margins if metal prices stagnate.

- Geopolitics: Trade tensions (CUSMA review) and potential tariffs remain wildcards for Canadian exporters.

- Policy Shifts: The sector is becoming highly politicized; "Green Mining" mandates require heavy ESG investment.

Please wait processing your request...

Please wait processing your request...